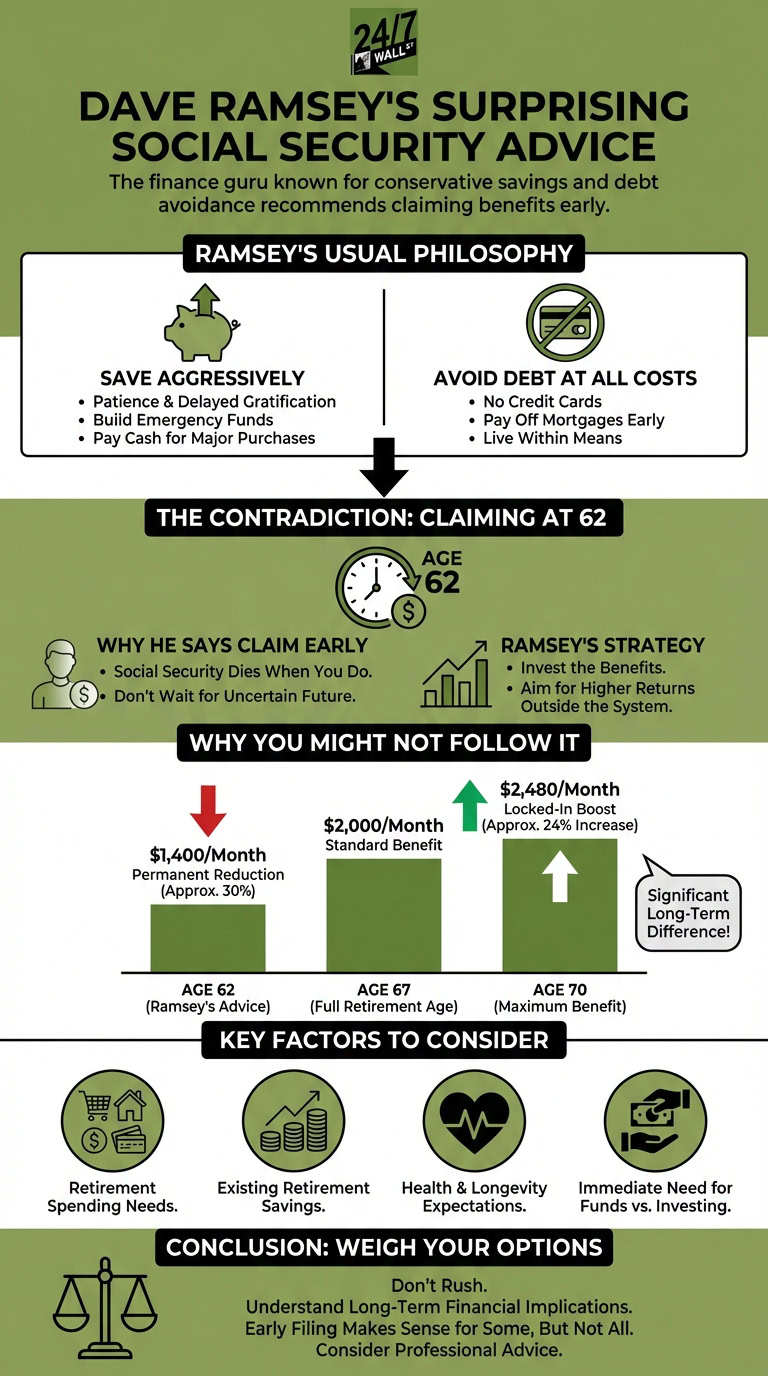

Dave Ramsey has built his reputation in personal finance on one core principle: protect yourself with savings and stay out of debt. He has pushed that philosophy into nearly every corner of daily spending, from car purchases to vacations to housing. He has even gone so far as to suggest that Americans buy a home with cash rather than carry a mortgage.

That makes his position on Social Security all the more striking. Ramsey breaks sharply from his own playbook when it comes to claiming benefits, and the reasoning behind that break is worth understanding.

Why Ramsey’s Social Security advice defies his usual logic

Ramsey’s financial guidance is built on patience and delayed gratification. Save first, spend later. Avoid the temptation of debt-financed convenience in every category, whether automobiles, clothing, or travel. So it comes as a genuine surprise that Ramsey tells Americans to claim Social Security at the earliest possible age: 62.

For anyone born in 1960 or later, full retirement age (FRA) is 67. Waiting until FRA means collecting 100% of the benefit earned through a lifetime of payroll taxes. Delaying past FRA adds roughly 8% per year, so waiting until 70 pushes the monthly check to 124% of the FRA amount. Filing at 62, by contrast, locks in a permanent 30% reduction: a person with an FRA of 67 who claims at 62 walks away with just 70% of their full benefit, for life.

Yet Ramsey recommends filing at 62 anyway, and he has two distinct arguments for doing so. The first is straightforward: benefits stop when you die, so collecting earlier means more total payments if your lifespan is average or shorter. His second argument goes further. Ramsey does not suggest grabbing the check and spending it. Instead, his recommendation is to start payments at 62 and immediately channel the money into a diversified mutual fund, on the theory that investment returns can outpace the guaranteed 8% annual increase available by waiting.

You may not want to follow Ramsey’s advice

Part of Ramsey’s thinking reflects genuine concern about Social Security’s financial durability, and those concerns have only deepened. The 2026 Social Security and Medicare Trustees Reports, released in June 2026, show that the Old-Age and Survivors Insurance trust fund will be able to pay 100% of scheduled benefits only through the fourth quarter of 2032, one year earlier than last year’s projection. Unless Congress acts, current and future beneficiaries alike would see their benefits cut by 22% at that point. That is a legitimate risk worth factoring in. Even so, the core problem with filing at 62 remains unchanged: it locks in a smaller check for life, before any future cuts are even applied.

The numbers tell the story clearly. Imagine you are eligible for a $2,000 monthly benefit at your FRA of 67. Claiming at 62 pays $1,400 a month (70% of the full amount), waiting to FRA pays $2,000, and delaying to 70 pays $2,480 a month (124%). Those gaps compound over decades. The break-even point where cumulative lifetime benefits from claiming at FRA surpass those from claiming at 62 arrives at around age 78 and 8 months. Anyone who lives into their 80s comes out ahead by waiting.

There is also a practical obstacle in Ramsey’s invest-the-checks plan. In 2026, anyone under FRA who is still working and earns more than $24,480 will have Social Security withhold $1 in benefits for every $2 earned above that threshold. That earnings test creates a direct conflict for anyone who has not fully stopped working by 62. To execute the strategy as Ramsey describes it, a retiree generally needs to be completely out of the workforce and financially positioned to cover living expenses while routing every check into the market.

Your Social Security claiming decision ultimately comes down to several personal factors:

- What your retirement spending needs look like

- How much money you have saved for your senior years

- How healthy or unhealthy you are, and how you expect that to affect your longevity

If Social Security is your primary source of living expenses in retirement, investing the checks is simply not realistic. And Ramsey’s strategy of claiming early and investing the money depends on several factors that are far from guaranteed. Market performance is the most obvious: returns are volatile, especially over shorter timeframes, and a retiree who claims at 62 and immediately encounters a prolonged downturn may see this plan underperform a simple decision to delay.

The clearest takeaway is that Ramsey’s debt-avoidance and savings philosophy is worth following closely. On Social Security specifically, his advice may fit a narrow set of circumstances: a retiree who is fully debt-free, has substantial savings, and is genuinely committed to investing every check rather than spending it. For everyone else, running the break-even math against your own health history and income needs is the smarter first step before locking in a permanently reduced benefit.

Editor’s note: This article has been updated to reflect the June 2026 Social Security Trustees Report, which moved the projected OASI trust fund depletion date to 2032 (one year earlier than prior estimates) with a potential 22% benefit cut if Congress fails to act. The 2026 earnings test threshold of $24,480 for claimants under full retirement age has also been added, along with the AARP-calculated break-even age of approximately 78 years and 8 months for claiming at 62 versus full retirement age.

Contact [email protected] for any questions or corrections.