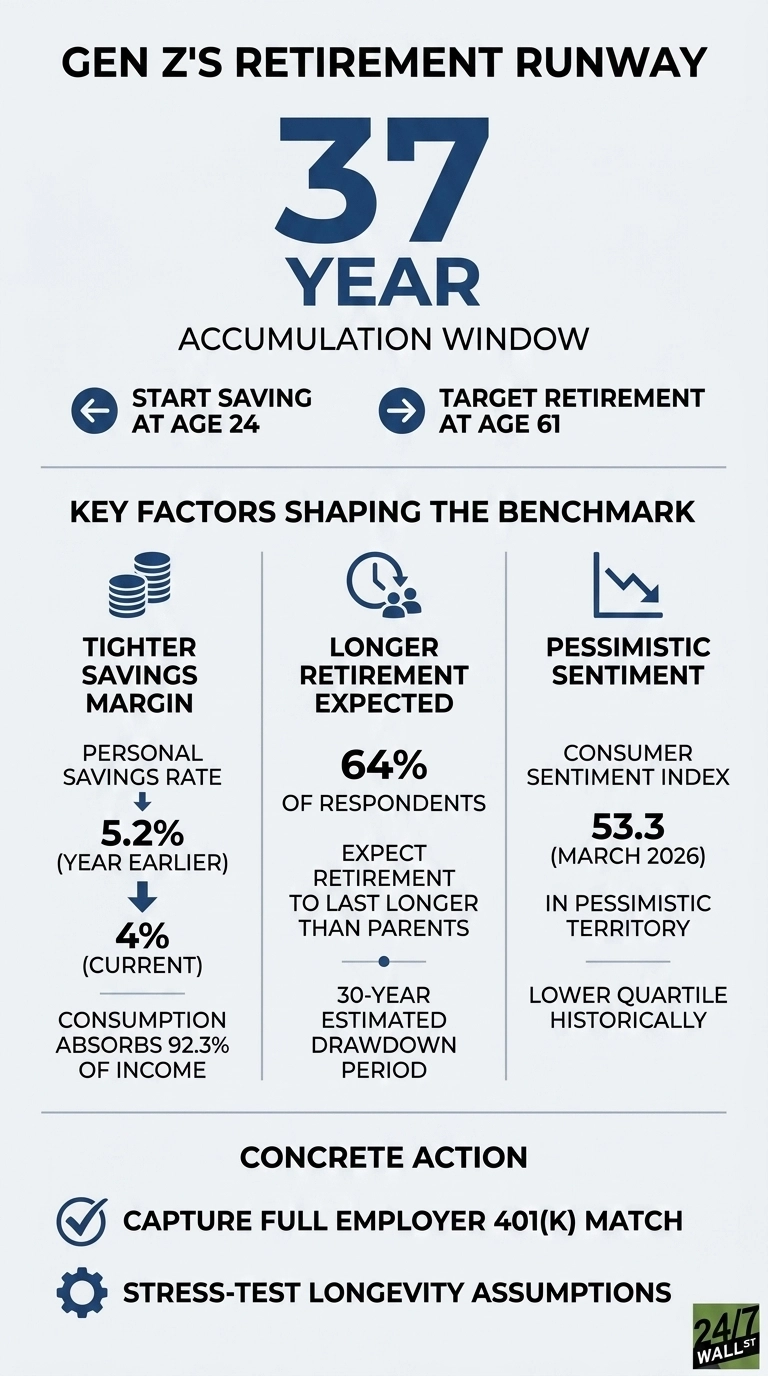

Gen Z is approaching retirement with a very different rhythm than the generations before them. Northwestern Mutual’s 2025 Planning & Progress Study shows they typically begin saving at 24 and picture themselves stepping out of the workforce around 61. That gives them nearly four decades to build a nest egg, a span that looks generous next to Boomers, who report starting at 37 and planning to retire at 72. On paper, it’s a 13‑year advantage, but in practice, the economy will decide how much that head start is actually worth.

The runway looks generous on paper

Compounding pays out most generously to those who give it time, which is why a 37‑year savings window carries real weight. Someone who starts at 24 gets more than a decade of growth before the average Boomer even begins. Northwestern Mutual’s data shows a generation that absorbed the lesson early: begin sooner, stay consistent, and try to reach the finish line ahead of schedule. The same study reports that Americans now estimate they will need $1.26 million to retire comfortably, down from last year’s $1.46 million as inflation pressures eased.

Gen Z also imagines retirement differently, with 79% saying their vision diverges from their parents’, and nearly two‑thirds expect their retirement years to last longer. A longer retirement, supported by a smaller target number, is the tension at the center of the early‑exit plan.

The economic backdrop is constraining household savings

The early‑retirement ambition is running straight into a tight household‑finance environment. The personal savings rate stood at 4% in the first quarter of 2026, down from 5.2% a year earlier, and personal consumption now accounts for 92.3% of disposable income. That leaves very little room for the long‑horizon contributions an early exit requires. Per‑capita disposable income is $68,617, and average private‑sector hourly earnings reached $37.41 in April 2026, yet the extra income is being pulled into day‑to‑day spending rather than long‑term saving.

The sentiment data tell the same story: The University of Michigan Consumer Sentiment Index registered 48.2 in May, a reading in the lower quartile of its historical range and firmly in what the index classifies as pessimistic territory. Headline CPI stands at 332.4, near the top of its twelve‑month range, and Core PCE has climbed from 125.79 to 129.28 over the past year. The 10‑year Treasury yield sits at 4.42%, a level that raises borrowing costs but finally offers a more functional baseline for long‑duration fixed‑income returns than the prior decade provided.

The longevity risk

An earlier retirement stretches the number of years that savings have to cover. Survey data show that 39% of U.S. adults consider it likely or very likely that they will outlive their savings, a concern that aligns with the longer life expectancy built into the Gen Z timeline. A retiree stepping away at 61 and planning for life into their nineties is looking at roughly three decades of withdrawals, a span that demands a larger starting balance than the traditional 65‑to‑85 frame Boomers planned around. That tension sits at the center of retirement longevity risk.

Debt is one of the few variables moving in a helpful direction, with U.S. adults carrying debt held an average of $22,354 in non‑mortgage balances as of February 2025, a figure that has fallen 25% over three years. Lower short‑term debt frees up the cash flow that a 37‑year saving plan depends on, and it gives younger workers more room to build toward long‑horizon goals.

What the math actually requires

To translate the goal into contributions, a worker targeting $1.26 million over 37 years at a 7% real return faces a monthly contribution requirement that scales with income growth and investment mix. The early start is what makes that figure manageable. A 37-year-old Boomer starting from zero with the same target would need to set aside several times that amount per month to reach the same destination by 72.

Three practical implications follow from the data. Contribution rates carry more weight than market timing over a 37-year horizon, so capturing the full employer 401(k) match is one of the higher-return contribution choices available to most Gen Z workers. Sequence-of-returns risk grows when retirement begins at 61, making a glide path that protects the final five working years before exit more important than for someone retiring at 67. And longevity assumptions should be stress-tested against the 64% of respondents who expect longer retirements than their parents had.

The 13-year head start is real, and so is the labor market backdrop supporting it, with unemployment at 4.3% and GDP growth at 2.0% in the first quarter of 2026. Whether the runway translates into a 61st-birthday retirement depends on what happens in the 37 years between the intention and the date.

Contact [email protected] for any questions or corrections.