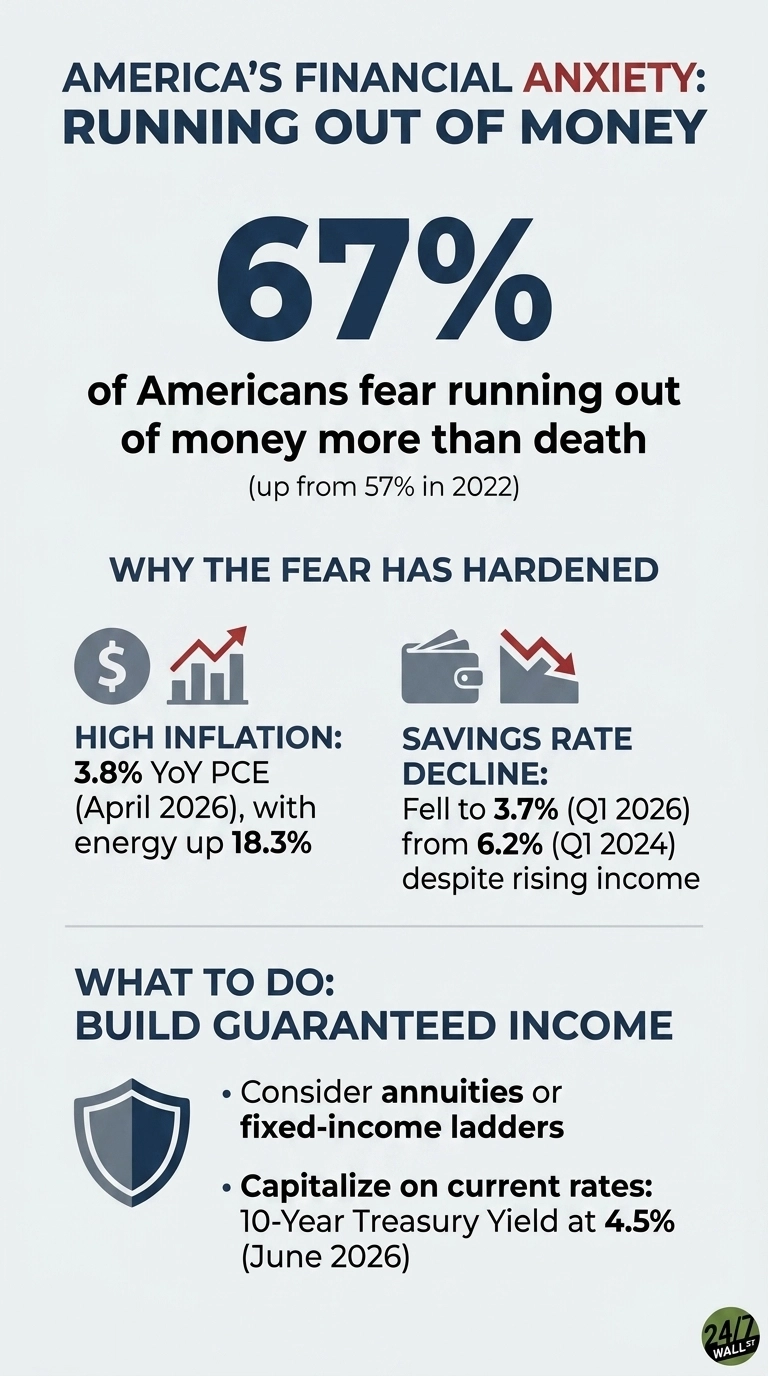

A new finding from the Allianz Center for the Future of Retirement’s 2026 Annual Retirement Study puts a number on something many people sense but don’t articulate: 67% of Americans say they worry more about running out of money than about dying. That share has climbed steadily, from 57% in 2022 to 67% in 2026. The problem is that the anxiety is not isolated to one cohort, as Gen X reports the highest level at 73%, and the concern appears across all adult age groups in the survey.

The economic backdrop helps explain why the fear has hardened. Headline PCE inflation ran at 3.8% year over year in April 2026, with energy alone up 18.3% and goods inflation accelerating to 4.4%. The Consumer Price Index sits at 332.4, a 90th-percentile reading over the past 12 months, all while the University of Michigan Consumer Sentiment Index has fallen to 49.8 in April 2026, down from 61.7 in July 2025, a level the index categorizes as recessionary.

The Fear Has a Mathematical Basis

The concern has a mathematical basis: 82% recognize that during a 30-year retirement, the cost of goods and services will at least double. That awareness aligns with the historical math of compounding inflation and reframes the question of savings. A nest egg that looks adequate at 65 has to maintain its purchasing power into the late 80s and 90s, against a price level moving in one direction.

The personal savings rate has been moving in the other direction. It fell from 6.2% in Q1 2024 to 3.7% in Q1 2026, the lowest reading in the recent series, even as wages and salaries rose from $12.15 trillion to $13.24 trillion over the same period. Average hourly earnings for private workers reached about $37 in April 2026, up from about $35 two years earlier. Nominal income kept rising, but the cushion is getting thinner.

What Americans Are Actually Worried About

The Allianz study breaks anxiety into specific buckets: 77% worry that everyday expenses will become unaffordable, and the same survey reports widespread concern about market drops, health care costs, and outliving savings. With this report, 60% of respondents worry that Social Security will not be available through their full retirement, and 61% say they do not know what their health care costs will be or how they will pay for them.

The Social Security concern has policy substance behind it, with research from the Stanford Institute for Economic Policy Research noting that closing the program’s funding gap entirely through benefit cuts would double the elderly poverty rate, which is why most proposals combine revenue and benefit changes, including raising the payroll tax rate from 12.4% to 15.9% of wages by 2035. Long-term care sits in a similar category of unmodeled risk. A nursing home stay can run $10,000 to $15,000 a month, an amount almost always paid out of retirement accounts when insurance is absent.

The Planning Gap

Nearly half of Americans (48%) do not have a written financial plan. Among those with retirement accounts, 58% believe simply having a 401(k), 403(b), or IRA is enough, while 56% admit they do not know what else they should be doing. The disconnect between participation and preparation is where most of the anxiety lives.

One data point from the same survey suggests that what people say would help: 77% report that a guaranteed income stream would decrease their anxiety about spending money in retirement. That preference is consistent with the current rate environment: the 10-year Treasury yield sits at 4.5%, and the Fed funds upper bound at 3.75%, making annuity pricing and fixed-income ladders more workable than they were in the zero-rate decade.

Building for Durability

The Allianz data centers on income durability rather than overall savings levels. The numbers point to income durability as the structural problem. A portfolio sized to a single retirement-date balance treats longevity, inflation, health shocks, and Social Security uncertainty as someone else’s variables. The 67% figure suggests Americans already feel the weight of those variables. The architecture that addresses them, layering guaranteed income with growth assets, planning for a price level that doubles, and writing the plan down, is what closes the gap between having an account and having a plan.

Contact [email protected] for any questions or corrections.