A new measure of how Americans understand money has surfaced the same finding researchers have documented for nearly a decade: women score about 10 points lower than men on financial literacy, and the gap barely moves. The number itself is unremarkable until set against the economic lives women actually lead. They earn less per hour, experience more career interruptions due to caregiving, and outlive their male peers by several years on average. A knowledge gap of that size, layered on top of those facts, has direct implications for retirement income.

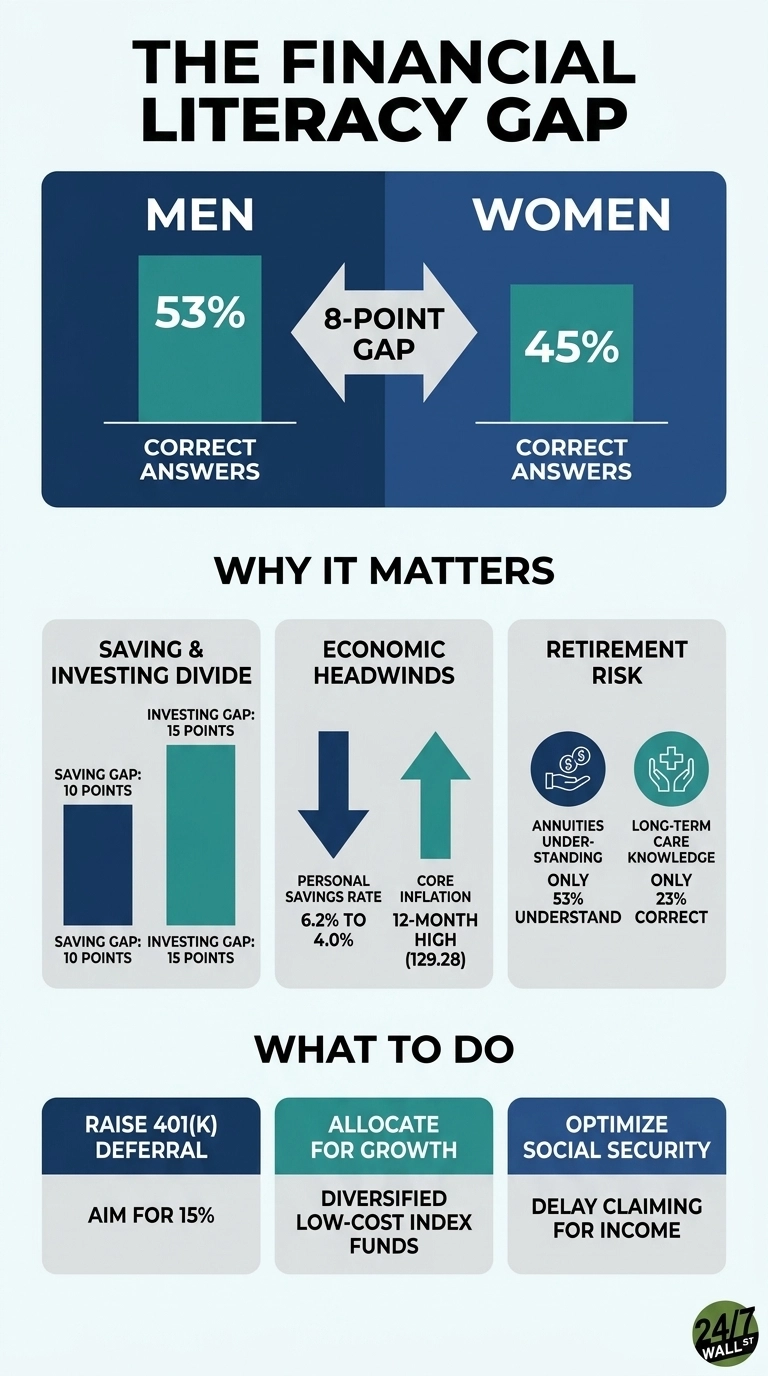

The TIAA Institute and GFLEC’s 2025 P-Fin Index found that men correctly answered 53% of the index’s questions while women answered 45%. The headline gap is closer to 8 points on that measure, but on the binary “very high literacy” threshold, the divide widens: 22% of men cleared it, compared with 11% of women. Regression analysis confirms the gap persists even after controlling for age, education, and income, indicating it is a knowledge gap that survives the usual explanations of schooling and earnings.

Where the gap actually opens up

Women do not lag across the board, but the gaps show up exactly where they matter most. The P‑Fin Index finds that women score essentially the same as men on day‑to‑day spending questions, yet fall sharply behind in the categories that shape long‑run wealth. The saving gap is ten points, and the investing gap is fifteen points, both documented in the report: “These gender differences are… as large as 10 and 15 percentage points in the realms of saving and investing”. Those are the levers that determine whether a 65‑year‑old ends up with a modest balance or a life‑changing one.

A 30‑year‑old woman who spends two decades under‑allocating to equities because she isn’t confident in what she owns will reach retirement with a fundamentally different balance sheet than a male peer earning the same income.

The current environment makes that gap more expensive to carry. Households are saving less: the personal savings rate has fallen from 6.2% in early 2024 to 4.0% in the first quarter of 2026. Inflation is still running hot, with core PCE at 129.28, the highest reading in the past year. And consumer sentiment has slipped to 48.2, a level deep in pessimistic territory.

In the P‑Fin data, low financial literacy already shows up as higher fragility: “Those with very low financial literacy are three times more likely to be financially fragile,” and today’s macro backdrop amplifies that vulnerability. A knowledge gap is far cheaper to carry when inflation is low and savings are high. Right now, the opposite is true, and the cost of falling behind compounds every year it goes unaddressed.

Why this is a longevity problem

The connection between retirement risk and financial literacy begins with a simple demographic fact. Women live longer, so their savings must stretch further. Yet the 2025 P Fin Index finds that most Americans lack even the basic knowledge to manage that longevity risk. Only 23 percent of adults answered the question about the likelihood of needing long-term care correctly, and just 53 percent understood that an annuity can guarantee lifetime income. Women scored below men on every retirement subtopic measured. That gap is especially troubling because women are more likely to need long-term care and more likely to pay for it alone.

The consequences appear not in theory but in financial fragility. Adults with very low financial literacy are three times more likely to be unable to come up with 2,000 dollars for an unexpected need. They are five times more likely to lack even one month of emergency savings. Women are overrepresented in that low literacy group. So when a financial shock arrives, a job loss, a medical bill, a divorce, it lands harder on them. The math of a longer life becomes, without basic financial fluency, a math of ruin.

What actually closes the gap

Contact [email protected] for any questions or corrections.