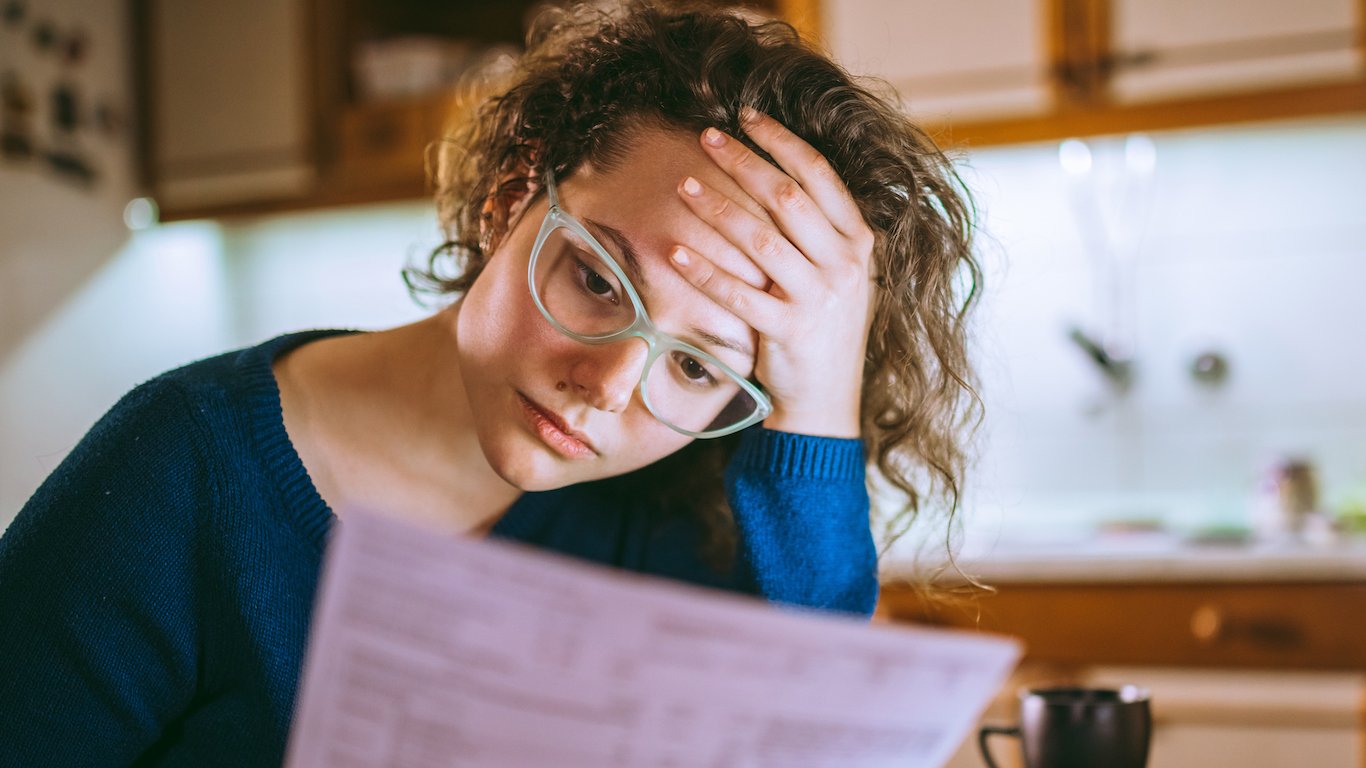

The COVID-19 pandemic and associated lockdowns in 2020 led to over 9 million U.S. workers losing their jobs. Of those who didn’t, some took pay cuts or had their employment hours reduced. This put a strain on the ability of many Americans to keep up with their mortgage payments. (Here are the states with the most mortgage debt.)

Struggling homeowners have received some temporary relief. The federal Coronavirus Aid, Relief and Economic Security Act, signed into law in March 2020, included provisions for mortgage forbearance — meaning that homeowners with federally backed mortgages could suspend their monthly payments. The forbearance relief was extended for as long as 12 months in September of 2021.

When forbearance ends, however, homeowners need to contact their lenders or loan servicers to arrange a plan for catching up with the payments that were deferred. As of February 2021, according to the Government Accountability Office, homeowners in forbearance had accumulated an average of eight mortgage payments that will have to be repaid. This will leave some homeowners in debt for tens of thousands of dollars. (Here are the states where people are struggling the most with debt.)

Click here to learn how many people in your state are behind on their mortgage payments

The GAO found that forbearance was more common among certain demographics at greater risk of mortgage default, including first-time homebuyers, low and moderate-income buyers with Federal Housing Authority and Rural Housing Service loans, and minorities. Black and Latino homeowners — who are more likely to have been negatively impacted by the pandemic — had used forbearance at twice the rate of white homeowners.

Although some borrowers are back on their feet and out of forbearance and currently working to get up to date on their payments, many are still behind and could face foreclosure. Others didn’t qualify for relief in the first place and are currently in default.

50. Oregon

> Mortgage delinquency rate (30+ days): 0.76%

> Share with a subprime credit score: 15.65% — 9th lowest

> Homeownership rate 2019: 62.9% — 9th lowest

> Median home value 2019: $354,600 — 6th highest

> Median household income 2019: $67,058– 18th highest

[in-text-ad]

49. Washington

> Mortgage delinquency rate (30+ days): 0.84%

> Share with a subprime credit score: 14.32% — 3rd lowest

> Homeownership rate 2019: 63.1% — 10th lowest

> Median home value 2019: $387,600 — 5th highest

> Median household income 2019: $78,687– 7th highest

[recirclink id=959952]

47. California

> Mortgage delinquency rate (30+ days): 0.95%

> Share with a subprime credit score: 18.28% — 18th lowest

> Homeownership rate 2019: 54.9% — 2nd lowest

> Median home value 2019: $568,500 — 2nd highest

> Median household income 2019: $80,440– 5th highest

47. Idaho

> Mortgage delinquency rate (30+ days): 0.95%

> Share with a subprime credit score: 17.52% — 15th lowest

> Homeownership rate 2019: 71.6% — 6th highest

> Median home value 2019: $255,200 — 19th highest

> Median household income 2019: $60,999– 20th lowest

[in-text-ad-2]

46. Colorado

> Mortgage delinquency rate (30+ days): 0.98%

> Share with a subprime credit score: 18.05% — 17th lowest

> Homeownership rate 2019: 65.9% — 19th lowest

> Median home value 2019: $394,600 — 4th highest

> Median household income 2019: $77,127– 9th highest

45. Vermont

> Mortgage delinquency rate (30+ days): 1%

> Share with a subprime credit score: 13.73% — 2nd lowest

> Homeownership rate 2019: 70.9% — 8th highest

> Median home value 2019: $233,200 — 24th highest

> Median household income 2019: $63,001– 25th lowest

[in-text-ad]

44. Montana

> Mortgage delinquency rate (30+ days): 1.06%

> Share with a subprime credit score: 17.34% — 14th lowest

> Homeownership rate 2019: 68.9% — 14th highest

> Median home value 2019: $253,600 — 20th highest

> Median household income 2019: $57,153– 11th lowest

[recirclink id=968097]

43. Utah

> Mortgage delinquency rate (30+ days): 1.09%

> Share with a subprime credit score: 17.20% — 12th lowest

> Homeownership rate 2019: 70.6% — 9th highest

> Median home value 2019: $330,300 — 10th highest

> Median household income 2019: $75,780– 11th highest

42. Wisconsin

> Mortgage delinquency rate (30+ days): 1.11%

> Share with a subprime credit score: 16.58% — 11th lowest

> Homeownership rate 2019: 67.2% — 20th highest

> Median home value 2019: $197,200 — 21st lowest

> Median household income 2019: $64,168– 21st highest

[in-text-ad-2]

41. Minnesota

> Mortgage delinquency rate (30+ days): 1.12%

> Share with a subprime credit score: 11.99% — the lowest

> Homeownership rate 2019: 71.9% — 3rd highest

> Median home value 2019: $246,700 — 21st highest

> Median household income 2019: $74,593– 13th highest

40. North Dakota

> Mortgage delinquency rate (30+ days): 1.13%

> Share with a subprime credit score: 15.15% — 7th lowest

> Homeownership rate 2019: 61.3% — 5th lowest

> Median home value 2019: $205,400 — 25th lowest

> Median household income 2019: $64,577– 20th highest

[in-text-ad]

38. Nevada

> Mortgage delinquency rate (30+ days): 1.14%

> Share with a subprime credit score: 27.49% — 11th highest

> Homeownership rate 2019: 56.6% — 3rd lowest

> Median home value 2019: $317,800 — 11th highest

> Median household income 2019: $63,276– 24th highest

[recirclink id=988934]

38. Arizona

> Mortgage delinquency rate (30+ days): 1.14%

> Share with a subprime credit score: 23.12% — 21st highest

> Homeownership rate 2019: 65.3% — 15th lowest

> Median home value 2019: $255,900 — 18th highest

> Median household income 2019: $62,055– 23rd lowest

37. Nebraska

> Mortgage delinquency rate (30+ days): 1.16%

> Share with a subprime credit score: 16.23% — 10th lowest

> Homeownership rate 2019: 66.3% — 24th lowest

> Median home value 2019: $172,700 — 14th lowest

> Median household income 2019: $63,229– 25th highest

[in-text-ad-2]

35. Hawaii

> Mortgage delinquency rate (30+ days): 1.20%

> Share with a subprime credit score: 15.58% — 8th lowest

> Homeownership rate 2019: 60.2% — 4th lowest

> Median home value 2019: $669,200 — the highest

> Median household income 2019: $83,102– 4th highest

35. Iowa

> Mortgage delinquency rate (30+ days): 1.20%

> Share with a subprime credit score: 17.21% — 13th lowest

> Homeownership rate 2019: 70.5% — 10th highest

> Median home value 2019: $158,900 — 9th lowest

> Median household income 2019: $61,691– 21st lowest

[in-text-ad]

34. Michigan

> Mortgage delinquency rate (30+ days): 1.23%

> Share with a subprime credit score: 21.56% — 25th highest

> Homeownership rate 2019: 71.6% — 5th highest

> Median home value 2019: $169,600 — 12th lowest

> Median household income 2019: $59,584– 19th lowest

[recirclink id=950776]

33. Massachusetts

> Mortgage delinquency rate (30+ days): 1.30%

> Share with a subprime credit score: 14.68% — 6th lowest

> Homeownership rate 2019: 62.2% — 8th lowest

> Median home value 2019: $418,600 — 3rd highest

> Median household income 2019: $85,843– 2nd highest

32. Wyoming

> Mortgage delinquency rate (30+ days): 1.35%

> Share with a subprime credit score: 20.80% — 24th lowest

> Homeownership rate 2019: 71.9% — 4th highest

> Median home value 2019: $235,200 — 23rd highest

> Median household income 2019: $65,003– 19th highest

[in-text-ad-2]

31. New Hampshire

> Mortgage delinquency rate (30+ days): 1.36%

> Share with a subprime credit score: 14.44% — 5th lowest

> Homeownership rate 2019: 71% — 7th highest

> Median home value 2019: $281,400 — 14th highest

> Median household income 2019: $77,933– 8th highest

30. South Dakota

> Mortgage delinquency rate (30+ days): 1.40%

> Share with a subprime credit score: 14.33% — 4th lowest

> Homeownership rate 2019: 67.8% — 18th highest

> Median home value 2019: $185,000 — 17th lowest

> Median household income 2019: $59,533– 18th lowest

[in-text-ad]

29. Virginia

> Mortgage delinquency rate (30+ days): 1.42%

> Share with a subprime credit score: 21.60% — 24th highest

> Homeownership rate 2019: 66.1% — 22nd lowest

> Median home value 2019: $288,800 — 12th highest

> Median household income 2019: $76,456– 10th highest

[recirclink id=988175]

28. Kansas

> Mortgage delinquency rate (30+ days): 1.49%

> Share with a subprime credit score: 21.77% — 23rd highest

> Homeownership rate 2019: 66.5% — 25th lowest

> Median home value 2019: $163,200 — 10th lowest

> Median household income 2019: $62,087– 24th lowest

27. Ohio

> Mortgage delinquency rate (30+ days): 1.60%

> Share with a subprime credit score: 24.23% — 18th highest

> Homeownership rate 2019: 66% — 21st lowest

> Median home value 2019: $157,200 — 8th lowest

> Median household income 2019: $58,642– 15th lowest

[in-text-ad-2]

26. Missouri

> Mortgage delinquency rate (30+ days): 1.62%

> Share with a subprime credit score: 24.66% — 16th highest

> Homeownership rate 2019: 67.1% — 21st highest

> Median home value 2019: $168,000 — 11th lowest

> Median household income 2019: $57,409– 13th lowest

25. Florida

> Mortgage delinquency rate (30+ days): 1.70%

> Share with a subprime credit score: 24.60% — 17th highest

> Homeownership rate 2019: 66.2% — 23rd lowest

> Median home value 2019: $245,100 — 22nd highest

> Median household income 2019: $59,227– 17th lowest

[in-text-ad]

24. Delaware

> Mortgage delinquency rate (30+ days): 1.71%

> Share with a subprime credit score: 23.37% — 19th highest

> Homeownership rate 2019: 70.3% — 11th highest

> Median home value 2019: $261,700 — 17th highest

> Median household income 2019: $70,176– 16th highest

[recirclink id=959952]

23. Maine

> Mortgage delinquency rate (30+ days): 1.75%

> Share with a subprime credit score: 19.10% — 21st lowest

> Homeownership rate 2019: 72.2% — 2nd highest

> Median home value 2019: $200,500 — 23rd lowest

> Median household income 2019: $58,924– 16th lowest

22. Alaska

> Mortgage delinquency rate (30+ days): 1.78%

> Share with a subprime credit score: 23.18% — 20th highest

> Homeownership rate 2019: 64.7% — 13th lowest

> Median home value 2019: $281,200 — 15th highest

> Median household income 2019: $75,463– 12th highest

[in-text-ad-2]

19. North Carolina

> Mortgage delinquency rate (30+ days): 1.81%

> Share with a subprime credit score: 25.31% — 14th highest

> Homeownership rate 2019: 65.3% — 16th lowest

> Median home value 2019: $193,200 — 20th lowest

> Median household income 2019: $57,341– 12th lowest

19. Illinois

> Mortgage delinquency rate (30+ days): 1.81%

> Share with a subprime credit score: 21.21% — 25th lowest

> Homeownership rate 2019: 66% — 20th lowest

> Median home value 2019: $209,100 — 25th highest

> Median household income 2019: $69,187– 17th highest

[in-text-ad]

19. Maryland

> Mortgage delinquency rate (30+ days): 1.81%

> Share with a subprime credit score: 21.91% — 22nd highest

> Homeownership rate 2019: 66.8% — 23rd highest

> Median home value 2019: $332,500 — 9th highest

> Median household income 2019: $86,738– the highest

[recirclink id=968097]

16. New Jersey

> Mortgage delinquency rate (30+ days): 1.86%

> Share with a subprime credit score: 18.64% — 19th lowest

> Homeownership rate 2019: 63.3% — 11th lowest

> Median home value 2019: $348,800 — 7th highest

> Median household income 2019: $85,751– 3rd highest

16. Connecticut

> Mortgage delinquency rate (30+ days): 1.86%

> Share with a subprime credit score: 18.75% — 20th lowest

> Homeownership rate 2019: 65% — 14th lowest

> Median home value 2019: $280,700 — 16th highest

> Median household income 2019: $78,833– 6th highest

[in-text-ad-2]

16. Indiana

> Mortgage delinquency rate (30+ days): 1.86%

> Share with a subprime credit score: 24.73% — 15th highest

> Homeownership rate 2019: 69.3% — 13th highest

> Median home value 2019: $156,000 — 7th lowest

> Median household income 2019: $57,603– 14th lowest

15. New York

> Mortgage delinquency rate (30+ days): 1.87%

> Share with a subprime credit score: 17.92% — 16th lowest

> Homeownership rate 2019: 53.5% — the lowest

> Median home value 2019: $338,700 — 8th highest

> Median household income 2019: $72,108– 14th highest

[in-text-ad]

13. Texas

> Mortgage delinquency rate (30+ days): 1.91%

> Share with a subprime credit score: 29.84% — 7th highest

> Homeownership rate 2019: 61.9% — 7th lowest

> Median home value 2019: $200,400 — 22nd lowest

> Median household income 2019: $64,034– 22nd highest

[recirclink id=988934]

13. Tennessee

> Mortgage delinquency rate (30+ days): 1.91%

> Share with a subprime credit score: 27.65% — 10th highest

> Homeownership rate 2019: 66.5% — 24th highest

> Median home value 2019: $191,900 — 18th lowest

> Median household income 2019: $56,071– 9th lowest

12. Pennsylvania

> Mortgage delinquency rate (30+ days): 1.92%

> Share with a subprime credit score: 19.62% — 23rd lowest

> Homeownership rate 2019: 68.4% — 16th highest

> Median home value 2019: $192,600 — 19th lowest

> Median household income 2019: $63,463– 23rd highest

[in-text-ad-2]

11. Kentucky

> Mortgage delinquency rate (30+ days): 1.93%

> Share with a subprime credit score: 27.42% — 12th highest

> Homeownership rate 2019: 67% — 22nd highest

> Median home value 2019: $151,700 — 5th lowest

> Median household income 2019: $52,295– 7th lowest

10. Rhode Island

> Mortgage delinquency rate (30+ days): 1.95%

> Share with a subprime credit score: 19.37% — 22nd lowest

> Homeownership rate 2019: 61.7% — 6th lowest

> Median home value 2019: $283,000 — 13th highest

> Median household income 2019: $71,169– 15th highest

[in-text-ad]

9. Georgia

> Mortgage delinquency rate (30+ days): 2%

> Share with a subprime credit score: 29.41% — 9th highest

> Homeownership rate 2019: 64.1% — 12th lowest

> Median home value 2019: $202,500 — 24th lowest

> Median household income 2019: $61,980– 22nd lowest

[recirclink id=950776]

8. Arkansas

> Mortgage delinquency rate (30+ days): 2%

> Share with a subprime credit score: 30.50% — 4th highest

> Homeownership rate 2019: 65.5% — 17th lowest

> Median home value 2019: $136,200 — 3rd lowest

> Median household income 2019: $48,952– 3rd lowest

7. Oklahoma

> Mortgage delinquency rate (30+ days): 2.06%

> Share with a subprime credit score: 29.95% — 6th highest

> Homeownership rate 2019: 65.5% — 18th lowest

> Median home value 2019: $147,000 — 4th lowest

> Median household income 2019: $54,449– 8th lowest

[in-text-ad-2]

6. New Mexico

> Mortgage delinquency rate (30+ days): 2.15%

> Share with a subprime credit score: 26.30% — 13th highest

> Homeownership rate 2019: 68.1% — 17th highest

> Median home value 2019: $180,900 — 16th lowest

> Median household income 2019: $51,945– 6th lowest

5. South Carolina

> Mortgage delinquency rate (30+ days): 2.16%

> Share with a subprime credit score: 29.97% — 5th highest

> Homeownership rate 2019: 70.3% — 12th highest

> Median home value 2019: $179,800 — 15th lowest

> Median household income 2019: $56,227– 10th lowest

[in-text-ad]

4. Alabama

> Mortgage delinquency rate (30+ days): 2.40%

> Share with a subprime credit score: 30.78% — 3rd highest

> Homeownership rate 2019: 68.8% — 15th highest

> Median home value 2019: $154,000 — 6th lowest

> Median household income 2019: $51,734– 5th lowest

[recirclink id=988175]

3. Louisiana

> Mortgage delinquency rate (30+ days): 2.44%

> Share with a subprime credit score: 32.20% — 2nd highest

> Homeownership rate 2019: 66.5% — 25th highest

> Median home value 2019: $172,100 — 13th lowest

> Median household income 2019: $51,073– 4th lowest

2. West Virginia

> Mortgage delinquency rate (30+ days): 2.63%

> Share with a subprime credit score: 29.43% — 8th highest

> Homeownership rate 2019: 73.4% — the highest

> Median home value 2019: $124,600 — the lowest

> Median household income 2019: $48,850– 2nd lowest

[in-text-ad-2]

1. Mississippi

> Mortgage delinquency rate (30+ days): 3.54%

> Share with a subprime credit score: 32.57% — the highest

> Homeownership rate 2019: 67.3% — 19th highest

> Median home value 2019: $128,200 — 2nd lowest

> Median household income 2019: $45,792– the lowest

Methodology

To identify how many people in each state are behind on mortgage payments, 24/7 Wall St. reviewed data from the nonprofit Urban Institute’s Credit Health During the COVID-19 Pandemic report. We ranked states by their mortgage delinquency rate — the share of mortgage holders who are behind on their mortgage payments by 30 days or more — as of October 2020, the latest available data.

Additional data from the Urban Institute, also from October 2020, includes the share of people with a credit bureau record of a subprime credit score (equal to or less than 600). The Urban Institute dataset contains information derived from de-identified, consumer-level records from a major nationwide credit bureau.

24/7 Wall St. added annual estimates of median household income, Homeownership rate, and median home value from the Census Bureau’s 2019 American Community Survey.

Contact [email protected] for any questions or corrections.