Taiwan Semiconductor Manufacturing (NYSE:TSM | TSM Price Prediction) is set to report third-quarter earnings on October 16, a moment that could shape the trajectory for one of the semiconductor industry’s cornerstones. As the world’s leading contract chip manufacturer, TSM produces advanced chips for major players like Nvidia (NASDAQ:NVDA), Apple (NASDAQ:AAPL), and Advanced Micro Devices (NASDAQ:AMD).

With shares trading around $302 in midday trading today — up almost 8% and 53% higher year-to-date — the stock has ridden the AI wave to record highs. But with the report just days away, investors face a key decision: scoop up shares now for potential upside, or hold off amid volatility risks?

The AI Engine Driving TSM’s Surge

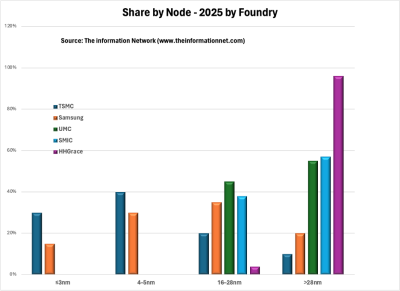

TSM’s growth story in 2025 hinges on artificial intelligence (AI) demand, which has transformed the company from a steady foundry into an indispensable AI enabler. Second-quarter revenue hit $30.1 billion, a 44% year-over-year jump that exceeded analyst forecasts. This beat stemmed from robust orders for advanced nodes like 3-nanometer (nm) and 5nm, which power Nvidia’s GPUs and Apple’s latest processors. Advanced technologies, defined as 7nm and more advanced technologies, accounted for 74% of total wafer revenue.

The numbers underscore TSM’s dominance: it holds a 70% share of the global foundry market, far ahead of rivals like Samsung. September alone brought NT$331 billion in sales, up 31.4% from last year, signaling sustained momentum into the third quarter. Management’s $38 billion to $42 billion capital expenditure plan for 2025 — up from $32 billion in 2024 — targets expansions in Arizona and Japan, ensuring capacity for AI’s insatiable appetite. Without TSM’s precision manufacturing, the AI boom simply stalls, making it a linchpin for tech’s future.

Navigating Headwinds in a Tense Landscape

Yet, TSM isn’t immune to challenges that could jolt the stock post-earnings. Geopolitical strains top the list: U.S.-China trade tensions and Taiwan Strait risks have prompted diversification, but 90% of production remains in Taiwan. Recent U.S. scrutiny on chip exports adds uncertainty, potentially capping growth if restrictions tighten.

Currency fluctuations pose another drag. A stronger New Taiwan Dollar eroded some Q2 gains, pressuring margins below first-quarter rates. Overseas fabs, while strategic, carry higher costs — up to 50% more than Taiwan facilities — squeezing profitability as utilization ramps up. Non-AI segments, like consumer electronics, recovered from Q1, with smartphone chip demand rising due to AI adoption. A miss on forward guidance, though, especially if Q3 revenue dips below expectations, could trigger a pullback in shares already at lofty valuations. These factors demand caution, as earnings surprises cut both ways in a high-stakes sector.

What the Street Expects — and Why It Matters

Analysts enter the October 16 report with a bit of exuberance. Where management is looking for $32.4 billion in revenue at the midpoint of its guidance range, consensus estimates call for $2.54 per share in earnings — a 13% rise from last year — on a 10% increase in revenue to $33.1 billion, the high end of TSM’s range. Profit is projected to climb as a result of AI’s advance, but tempered by forex headwinds. Wall Street’s average price target sits at $307 per share, implying modest upside from current levels, though recent upgrades from Susquehanna to $400 reflect AI tailwinds.

A beat could spark a 5% to 10% rally, especially if guidance lifts 2025 revenue growth to 32% to 34% as Morgan Stanley anticipates.

Investors should focus on 2nm progress and wafer pricing hikes — 5% to 10% increase are expected in 2026 — which could offset costs and affirm TSM’s edge. The call will reveal if AI’s fire keeps burning or if broader pressures dim the glow.

Buy, Sell, or Hold?

TSM’s fundamentals underscore the opportunity: AI demand propels 40% compounded annual growth through 2030, and its forward P/E of 25 trails the sector’s 29.4. At $302, shares offer a 1% yield and growth potential that justifies entry for long-term holders.

Buy if you’re bullish on semiconductors, which seem unstoppable at the moment, indicating an earnings beat is in the cards. But for risk-averse traders, wait — volatility could dip shares on any guidance whiff. Hold, though, if you already have a sizable position, as any pullback from its current price provides a better entry point.

Ultimately, Taiwan Semiconductor Manufacturing’s competitive moat in advanced nodes makes it a core holding, but time your move wisely around October 16.

Contact [email protected] for any questions or corrections.