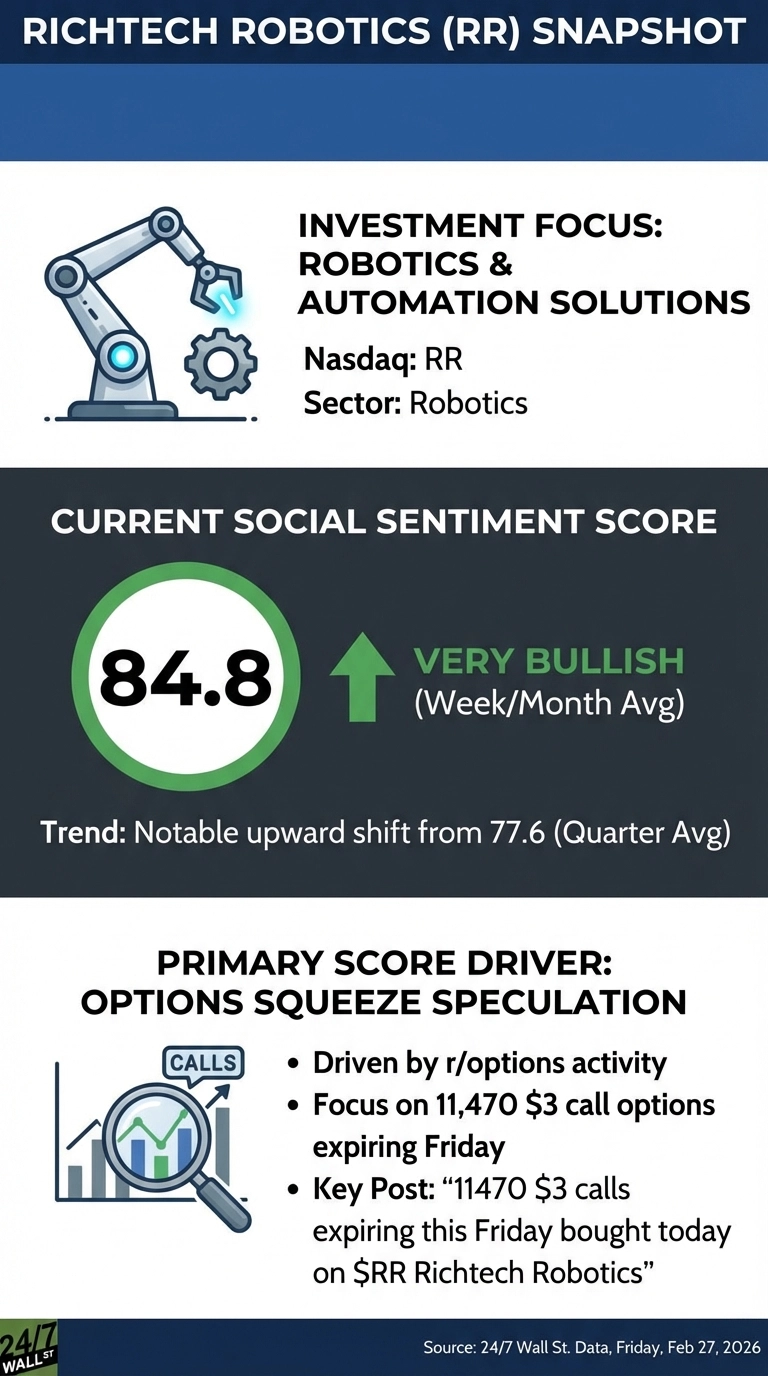

Richtech Robotics (NASDAQ:RR), a company that specializes in developing, manufacturing, and deploying robotic solutions for automation, is currently trading at $2.74, down 28% over the past month after a January scandal exposed what multiple law firms allege was a misrepresentation of the company’s relationship with Microsoft. Retail sentiment on Reddit has climbed from a quarterly average of 77.6 to 84.8 in the past week, a split that captures the central tension: does the post-crash price reflect a genuine reassessment of fundamentals, or does the stock reflect a business that was always more narrative than substance?

On January 29, 2026, Hunterbrook Media alleged Richtech mischaracterized what Microsoft called a “standard, non-commercial customer program” as a close commercial collaboration. Shares fell by more than 29% over two days on the news, and at least eight law firms have since filed class-action suits, with a lead plaintiff deadline of April 3, 2026.

Retail Traders Are Betting on a Squeeze, Not the Business

Discussion is concentrated in r/options, driven by a thread about a trader who purchased 11,470 $3 call options expiring Friday, which has accumulated 50 upvotes and 57 comments over 48 hours. The original post read: “11470 $3 calls expiring this Friday bought today on $RR Richtech Robotics.”

11470 $3 calls expiring this Friday bought today on $RR Richtech Robotics

by u/[OP] in r/options

One commenter framed the bull case: “Richtech currently has approximately $330M in cash, virtually no debt, and a market capitalization near $612M, with short interest exceeding 25%.” That is a short-squeeze setup, not a fundamental thesis.

- Revenue has fallen 42% from its FY2023 peak of $8.76M to $5.05M in FY2025, while SG&A tripled to $17.5M, producing an operating loss of $17.9M.

- The three-pillar model (hardware, RaaS, data services) generates only $0.3M in RaaS revenue per quarter, with no disclosed figures for data services.

- Short interest sits at 25.28% of float, roughly 4.6 times the peer group average of 5.43%.

Strong Balance Sheet, Unsustainable Burn

Looking at the numbers as the company moves deeper into 2026, Richtech closed Q1 FY2026 with $328.5M in liquid assets and just $730,000 in total debt. The problem is that the cash funds: Q1 FY2026 SG&A alone hit $11.8M against $1.1M in revenue. HC Wainwright maintains a Buy rating with a $6 price target, implying over 100% upside, but that call predates the Microsoft dispute. The April 3 lead plaintiff deadline is the next meaningful catalyst, as consolidated litigation could pressure the stock regardless of the business trajectory.