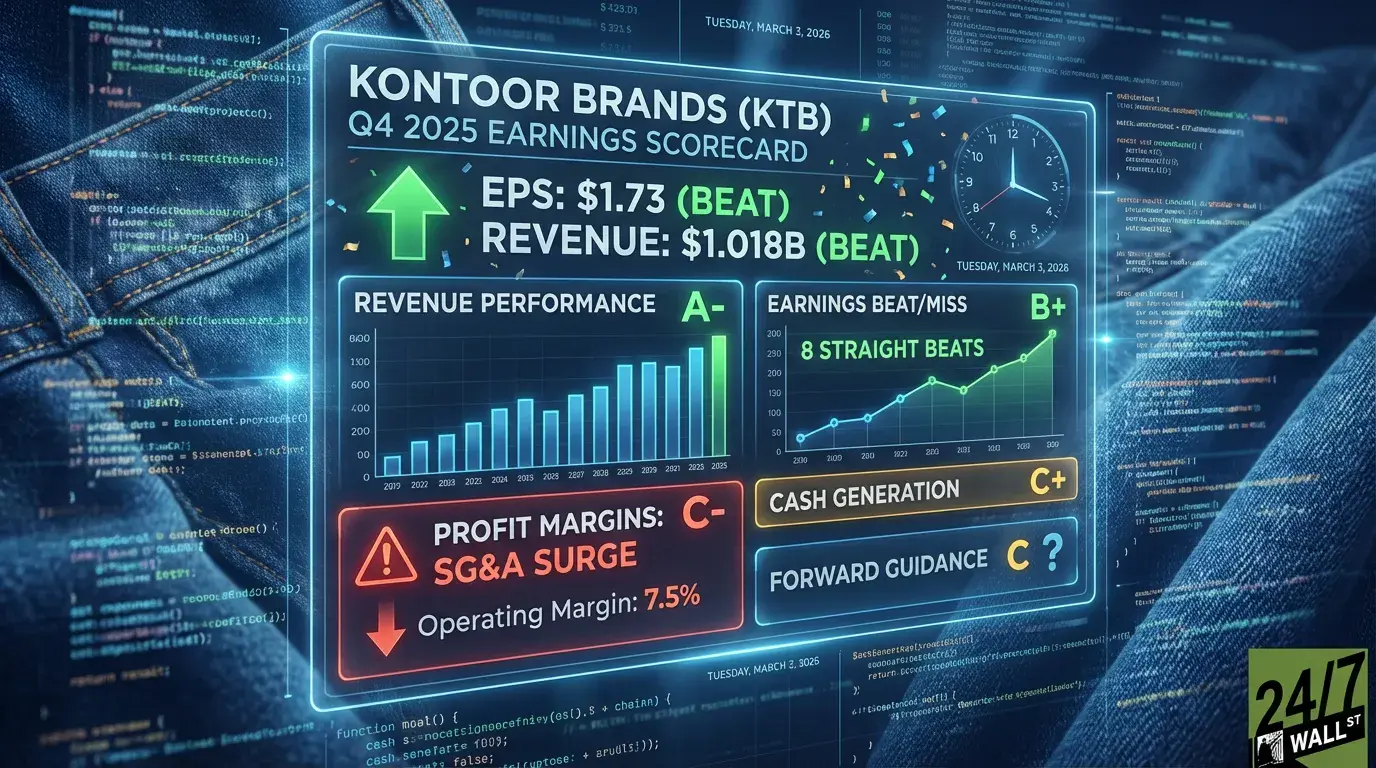

Kontoor Brands (NYSE:KNG) | KTB Price Prediction delivered a clean double beat to open fiscal 2026, reporting Q4 2025 adjusted EPS of $1.73 against a consensus estimate of $1.67, a +4.85% positive surprise. Revenue came in at $1.018 billion, clearing the $988.8 million estimate by nearly $29 million. Shares were trading at $64.82 heading into today’s session, up 6.11% year to date.

Q4 2025 Earnings Scorecard

| Category | Grade | Key Insight |

|---|---|---|

| Revenue Performance | A | Revenue of $1.018B increased 46% year over year from $699.3M in Q4 2024, reflecting the contribution from the Helly Hansen acquisition along with modest organic growth. |

| Earnings Beat/Miss | B+ | Adjusted EPS of $1.73 increased 26% year over year and beat the $1.6694 estimate. Reported EPS was $1.31 compared to $1.14 last year. |

| Forward Guidance | B | Management provided initial full-year 2026 guidance, projecting revenue of $3.40 to $3.45 billion and adjusted EPS of $6.40 to $6.50, representing expected growth of 9% and 15% to 16%, respectively. |

| Profit Margins | B- | Reported gross margin improved 250 basis points to 46.2%, while adjusted gross margin expanded 210 basis points to 46.8%. Reported operating income rose 44% to $121.1M, and adjusted operating income increased 48% to $150.3M, reflecting improved leverage despite incremental brand investments. |

| Cash Generation | B | Full-year operating cash flow totaled $455.8M. During the quarter, the company made a $200M voluntary term loan payment and repurchased $25M of shares, reflecting disciplined capital allocation alongside deleveraging efforts. |

| Management Tone | B+ | Management characterized 2025 as a transformational year driven by the Helly Hansen acquisition, strong Wrangler growth, and disciplined execution. The tone emphasized deleveraging progress and confidence entering 2026. |

Bottom Line

The headline numbers are strong. Revenue surpassed $1 billion for the quarter, increasing 46% year over year, supported by the Helly Hansen acquisition and steady brand performance. Adjusted operating income climbed 48% to $150.3M, and adjusted EPS rose 26%.

Importantly, margin performance improved rather than deteriorated. Adjusted gross margin expanded to 46.8%, and adjusted operating margin reached 14.8%, up 30 basis points year over year.

At $64.82, the stock trades at roughly 10x forward earnings based on 2026 guidance, a valuation that appears undemanding if projected earnings growth materializes. With initial 2026 guidance calling for high-single-digit revenue growth and mid-teens EPS expansion, the earnings call will focus on tariff impacts, Helly Hansen integration execution, and sustained margin expansion.

Contact [email protected] for any questions or corrections.