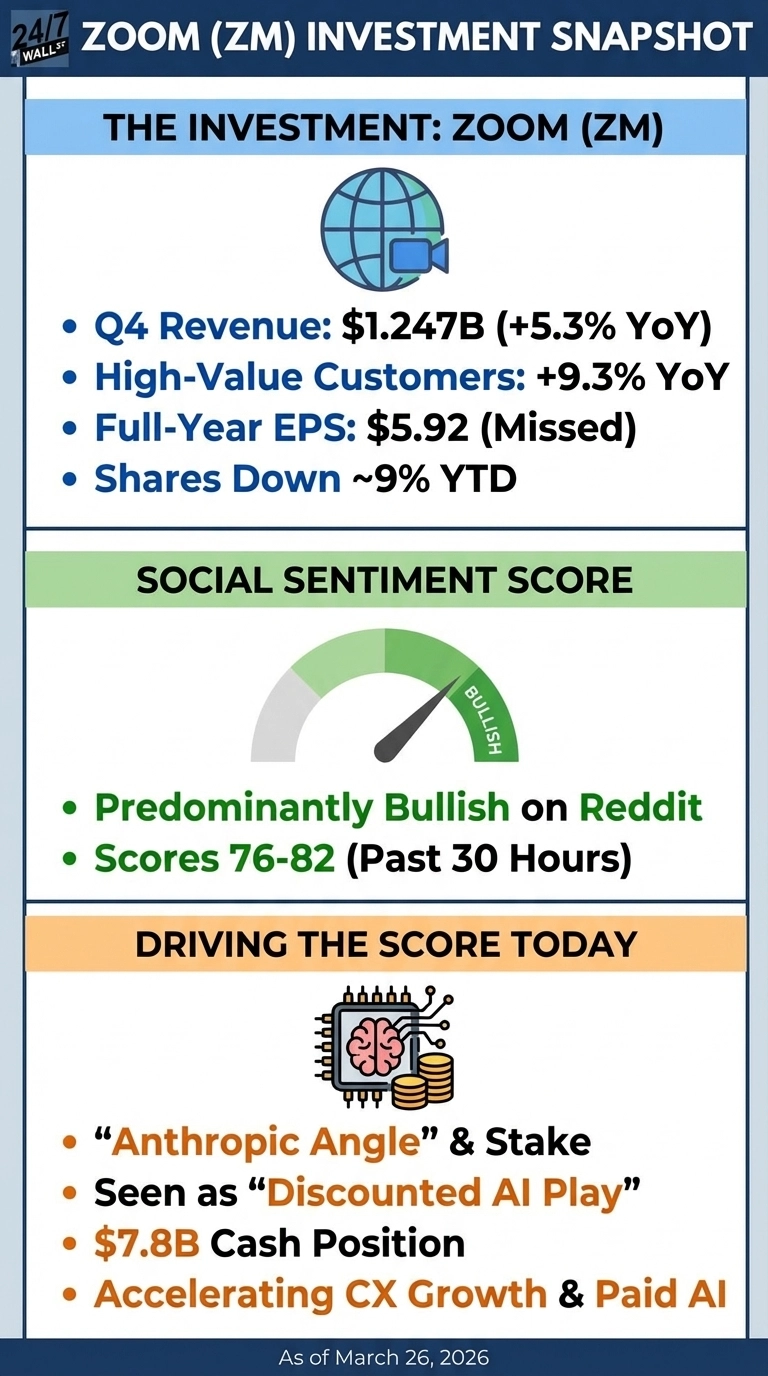

Still one of the most popular video calling tools, Zoom’s Q4 FY2026 earnings handed investors a headline that looked spectacular and a full-year figure that quietly disappointed. Zoom Video Communications (NASDAQ:ZM | ZM Price Prediction) posted $1.247 billion in Q4 revenue, up 5.3% year-over-year, beating estimates by 0.6%. High-value enterprise customers grew 9.3% year-over-year to 4,468 accounts. Yet the full-year non-GAAP EPS of $5.92 missed the $5.9724 estimate, marking Zoom’s first EPS miss in seven quarters. Shares dropped roughly 12% in the session after earnings and remain down about 7.5% year to date.

The Q4 non-GAAP EPS of $1.44, which beat the $0.85 estimate by 69%, was heavily distorted by $532 million in gains on strategic investments. Free cash flow fell nearly 19% year-over-year in Q4; the enterprise net dollar expansion rate was 98%, below the 100% threshold; and online monthly churn ticked up to 2.9% from 2.8%.

The Anthropic Angle Driving Reddit’s Bull Case

Sentiment on r/wallstreetbets has been predominantly bullish over the past 30 hours, with scores ranging from 76 to 82 across six of eight measured windows. The conversation centers on a thread titled “$ZM – Best Anthropic Play, Trades Below Nav.” from u/Stonkgang_, which has accumulated 109 upvotes and 55 comments.

$ZM – Best Anthropic Play, Trades Below Nav.

by u/Stonkgang_ in wallstreetbets

The post argues “$ZM, yes, Zoom Video owns a 1% stake in Anthropic due to its early investment in 2023… it generates 2bn in FCF a year, has a market cap of 22bn, with 7.8bn in cash… its entire core business trades at 5x FCF ($10bn)”, making Zoom the most efficient way to buy Anthropic exposure at a discount. Zoom carries $7.8 billion in cash against a $23 billion market cap, trades at roughly 12x trailing earnings, and guides for $5.065 to $5.075 billion in FY2027 revenue, the first time it would cross the $5 billion milestone. The bull case rests on three pillars:

- Zoom’s Anthropic stake and $7.8 billion cash position create a balance sheet that prices the core video and CX business at a deep discount to intrinsic value.

- Zoom Customer Experience saw accelerating high-double-digit growth in Q4, with paid AI included in each of the top 10 CX deals, pointing to real product expansion beyond legacy video.

- The analyst consensus of 14 buy ratings and a $97 average price target sits well above the current share price near $80, with at least one firm carrying a $115 price target.

Where the Bear Case Still Has Teeth

For investors focused on finances, Zoom’s free cash flow guidance for FY2027 is $1.70 to $1.74 billion, down from the $1.924 billion generated in FY2026. A net dollar expansion rate below 100% means existing enterprise customers are spending less than they did a year ago. Revenue growth is expected to decelerate, with consensus projecting 3.3% growth in the fiscal year after next. Microsoft Teams remains a formidable free alternative for enterprise buyers locked into Microsoft 365, and management explicitly flagged lengthened sales cycles.

At roughly 14x on guided EPS of $5.77 to $5.81 is reasonable for a profitable, cash-generative technology business. The Anthropic stake and agentic AI roadmap are the variables that will determine whether Zoom earns a higher valuation multiple from here.

Contact [email protected] for any questions or corrections.