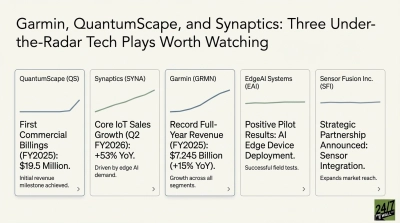

QuantumScape (NYSE:QS | QS Price Prediction), the pre-revenue solid-state battery developer, used its Q4 2025 report to pair a narrow earnings beat with a strategic pivot: chasing AI data centers, robotics, aviation and defense as new markets for a battery that has yet to power a single commercial electric vehicle. Q1 EPS of -$0.16 eased past the -$0.18 consensus. Shares are rising 5.8% heading into noon trading, but are down 25.8% year-to-date, even as the stock remains up 94.35% over one year. Investors want to know whether the AI pivot is vision or distraction.

Q 2025 Earnings Scorecard

| Category | Grade | Key Insight |

|---|---|---|

| Revenue Performance | F | Still zero product revenue; customer billings totaled $1 million, against a $4.7 billion market cap. |

| Earnings Beat/Miss | B | Q1 EPS of -$0.16 beat consensus by 11.11%. |

| Forward Guidance | C | 2026 adjusted EBITDA loss guided to $250M to $275M, roughly a 10% improvement, with capex rising to $40M to $60M. |

| Profit Margins | C+ | Q1 operating loss narrowed 11.64% YoY to -$109.18 million; R&D fell roughly 11.5% to $84.57 million. |

| Cash Generation | C | Q1 free cash flow of -$69.5 million worsened slightly from Q4, but total liquidity sits at $904.7 million, with cash down 37% YoY. |

| Management Tone | B | CEO Siva Sivaram called the Eagle Line “will help drive a virtuous cycle” of growth while reframing QSE-5 as a fit for data centers where “you absolutely cannot have a fire with million-dollar GPUs.” |

Bottom Line Assessment

Blended GPA lands near 2.3, roughly a C+. Verdict: Concerning to Hold. QuantumScape has not commercialized a battery in its primary EV market, yet is already positioning for AI, aviation and defense, a pattern that looks like chasing the next hot theme after EV demand cooled. The balance sheet buys time, and Wall Street agrees the risk-reward is balanced: zero Buy ratings, 7 Hold and 2 Sell, with a $7.41 consensus target implying -4.94% downside from current levels.

The single number to watch next quarter is customer billings; management expects an increase over 2025, and Eagle Line yield data will determine whether the AI pivot has technical substance or is purely narrative.

Contact [email protected] for any questions or corrections.