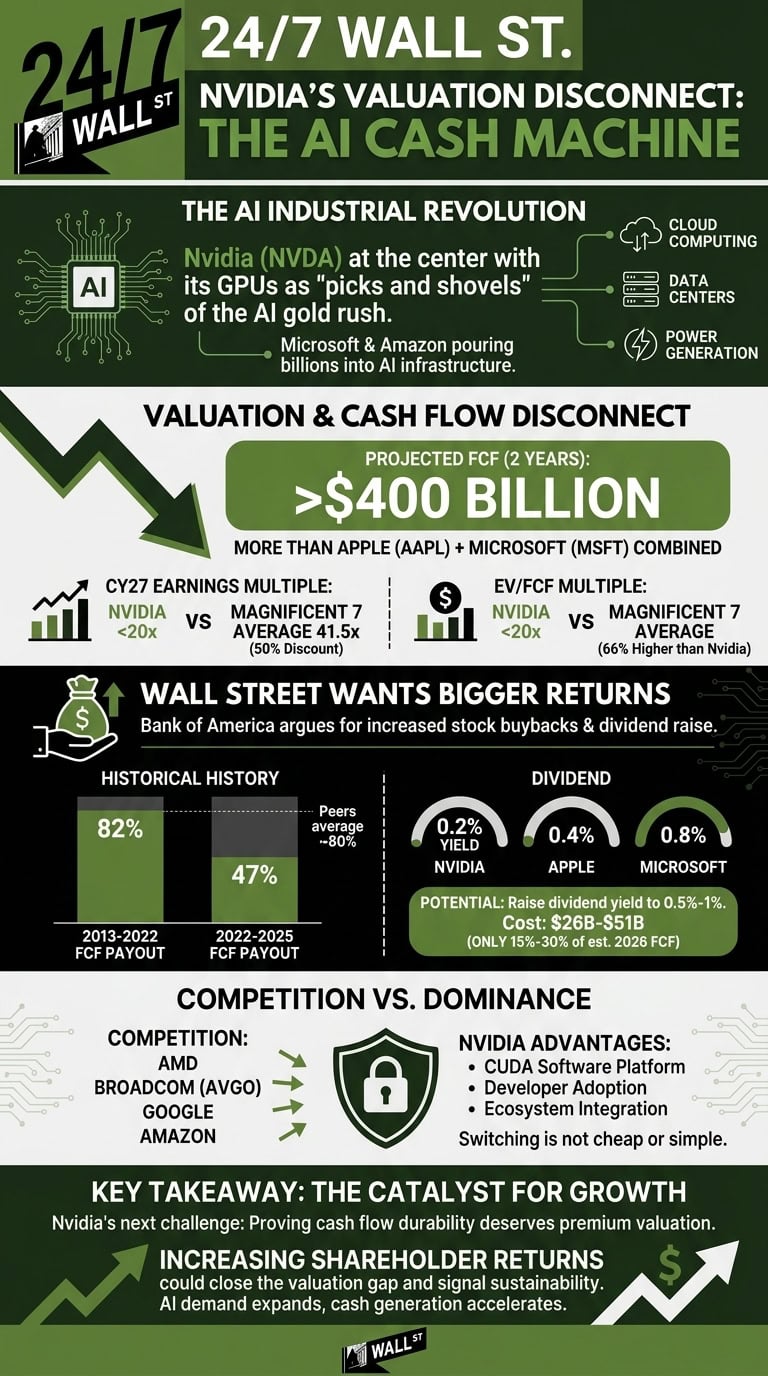

Artificial intelligence has become the market’s version of an industrial revolution. Every corner of the economy — cloud computing, utilities, networking hardware, data centers, and even power generation — is being reshaped by AI spending. At the center of that spending spree sits Nvidia (NASDAQ:NVDA | NVDA Price Prediction).

Its graphics processing units, or GPUs, have become the picks and shovels of the AI gold rush. Companies from Microsoft (NASDAQ:MSFT) to Amazon (NASDAQ:AMZN) are pouring tens of billions into AI infrastructure because Nvidia’s chips remain the fastest way to train and run large AI models.

Yet here’s the surprising part: Nvidia’s stock stopped rewarding investors for much of the past year. After its explosive run through 2023 and early 2024, shares largely moved sideways beginning last summer. Even with the stock recently breaking higher again, investors have started asking a fair question: How long can this dominance last?

Nvidia’s Valuation Disconnect

That skepticism is exactly what Vivek Arya of Bank of America tackled in a recent research note.

Arya estimates Nvidia could generate more than $400 billion in free cash flow over the next two years — a massive sum that is more than Apple (NASDAQ:AAPL) and Microsoft combined over the same period. That is an astonishing figure considering Apple and Microsoft are already viewed as two of the market’s premier cash-producing machines.

Free cash flow matters because it represents money left after operating expenses and capital investments. It is the cash a company can actually use to reward shareholders, buy businesses, or strengthen its balance sheet.

Despite that projected cash generation, Nvidia still trades at a discount to many of its peers.

Here’s what the numbers tell us:

| Company | CY27 Earnings Multiple | EV/FCF Multiple | Dividend Yield |

| Nvidia | Under 20x | Under 20x | 0.2% |

| Magnificent 7 Average | 41.5x | Higher than Nvidia by 66% | Varies |

| Apple | Higher than Nvidia | 33x | 0.4% |

| Microsoft | Higher than Nvidia | 42x | 0.8% |

According to Bank of America, Nvidia trades at roughly a 50% discount to Magnificent 7 peers on forward earnings and at a 66% discount on enterprise value-to-free-cash-flow metrics. Regardless of how you look at it, that is an unusual setup for a company still defining the AI infrastructure market.

More cash flow than Apple and Microsoft combined—yet trading at a 50% discount. Discover the massive valuation disconnect at the heart of the AI gold rush.

More cash flow than Apple and Microsoft combined—yet trading at a 50% discount. Discover the massive valuation disconnect at the heart of the AI gold rush.

Wall Street Wants Bigger Shareholder Returns

To convince investors its growth is sustainable, Arya says Nvidia needs to return more cash to them.

He argues Nvidia should increase stock buybacks and raise its dividend to better align with its massive free cash flow generation. The logic is straightforward: if a company is generating unprecedented levels of cash, shareholders want clearer evidence that cash will eventually flow back to them. Historically, Nvidia has done exactly that.

Between 2013 and 2022, Nvidia returned 82% of free cash flow to shareholders through buybacks and dividends. But from 2022 through 2025, that figure dropped to just 47%, according to Bank of America research. Its peers average closer to 80%.

The dividend gap stands out even more. Nvidia currently yields just 0.2%, compared with:

- Apple: 0.4%

- Microsoft: 0.8%

Arya estimates Nvidia could raise its dividend yield to between 0.5% and 1% at a cost of $26 billion to $51 billion. That would represent just 15% to 30% of estimated 2026 free cash flow and 11% to 21% of projected 2027 free cash flow.

In other words, Nvidia could still fund aggressive buybacks, expand its AI ecosystem, and maintain a fortress balance sheet even after boosting shareholder payouts.

As Arya wrote, “Increased cash returns could signal sustainability, widen the shareholder base, and help narrow the valuation gap.”

Competition Is Growing — But Nvidia Still Leads

Granted, Nvidia is not operating without risks. Arya noted Nvidia now accounts for roughly 8% of the entire S&P 500 by itself. That sheer size may limit how much additional institutional money can flow into the stock because many funds already own enormous positions.

Competition is also increasing. Advanced Micro Devices (NASDAQ:AMD) continues pushing aggressively into AI accelerators, while custom ASIC chipmakers like Broadcom (NASDAQ:AVGO) Google, and Amazon are building alternatives designed for specific workloads.

That said, Nvidia still holds major advantages in software, developer adoption, and ecosystem integration. CUDA — Nvidia’s programming platform — remains deeply embedded across AI development. Switching away from it is neither cheap nor simple for customers.

Surprisingly, that software advantage may matter more than the hardware itself over the long term.

Key Takeaway

In short, Nvidia’s biggest challenge may no longer be proving it can dominate AI chips. The market already understands that story. The next challenge is proving its cash flow durability deserves a premium valuation.

Bank of America’s argument is persuasive: if Nvidia can generate more than $400 billion in free cash flow over two years while still trading below many slower-growing peers, increasing shareholder returns could become the catalyst that finally closes the valuation gap.

Arya still calls Nvidia his top semiconductor stock pick — and the numbers explain why. AI demand continues expanding, Nvidia’s cash generation keeps accelerating, and even after its recent rebound, the stock still trades like investors are unsure the growth can last.

For long-term investors, that disconnect may be the opportunity.

Contact [email protected] for any questions or corrections.