At roughly $220, Boeing (NYSE:BA | BA Price Prediction) is a Buy. The stock has pulled back into a window that aligns with operational turnaround, a record backlog, and a reopened door to China. That combination rarely appears in a duopoly business.

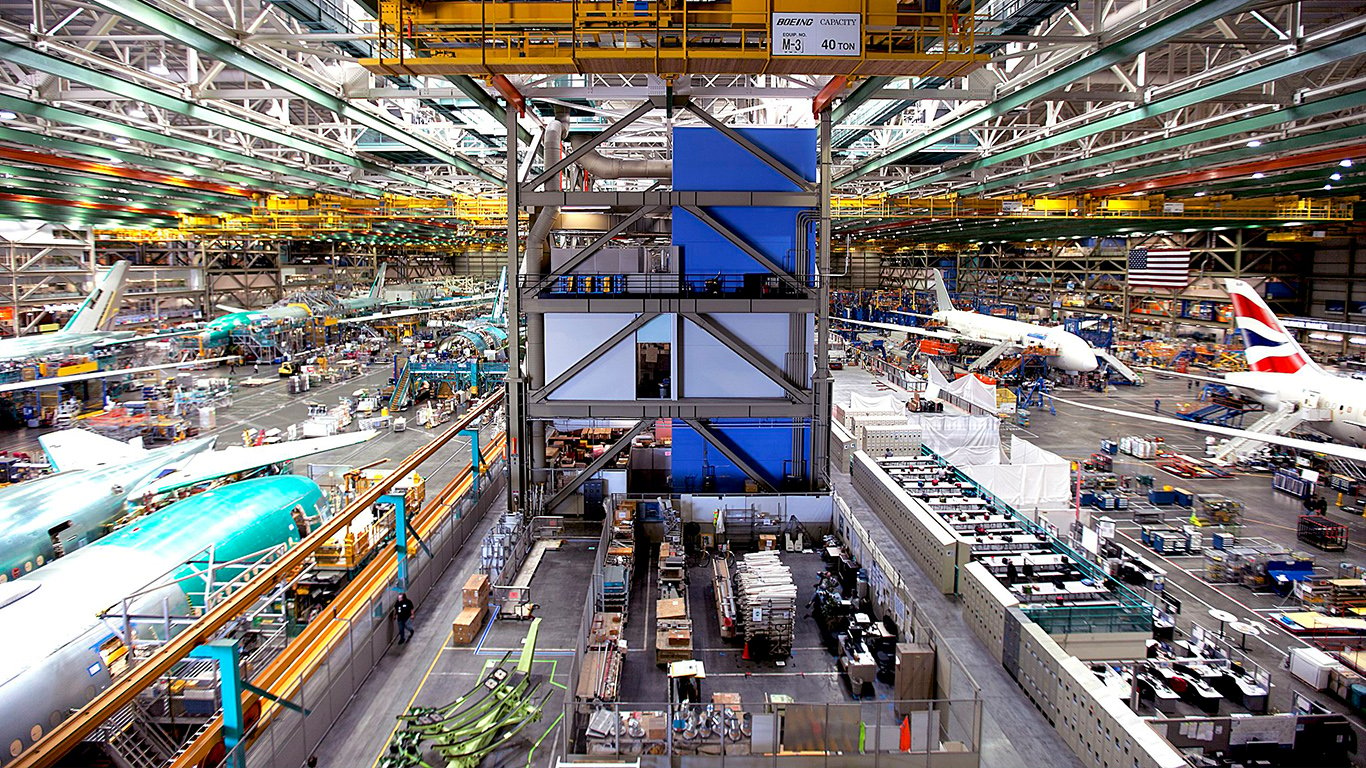

Boeing is one half of the global commercial aviation duopoly with Airbus and a dominant U.S. defense prime through programs like the F-15, KC-46 Tanker, and MQ-28 Ghost Bat. After years of grounded jets, strikes, and balance sheet damage, CEO Kelly Ortberg has steered the company back to shape: rising deliveries, a healing balance sheet, and a defense unit finally pulling its weight.

The stock recently slipped 7.68% in a week on a smaller-than-hoped China headline and a $49.5 million wrongful death verdict. That noise created the entry.

Why The China Reopening Changes The Math

The bull case starts with scale. Boeing’s backlog stands at a record $695B, with BCA alone holding $576 billion and more than 6,100 airplanes. Q1 2026 revenue rose 14% to $22.2 billion, and Boeing repaid $6.9 billion of debt in a single quarter, dropping total debt to $47.2B.

Trump’s trip reportedly produced an agreement for 200 Boeing aircraft with an option to expand to 750, the first major order from China in nearly a decade. Ortberg told analysts the opportunity is “a big number” tied to the U.S.-China relationship. Layer in 737 production at 42 per month heading to 47 this summer, plus 737-7 and 737-10 certifications expected later this year, and the delivery curve has room to bend upward.

Why The Bear Case Still Has Teeth

Commercial Airplanes ran a negative 6.1% operating margin in Q1, and free cash flow was a $1.5 billion usage. The 777X first delivery has slipped to 2027, and Boeing’s history with that program is not kind. Spirit AeroSystems integration is expected to drag roughly $1 billion of negative cash this year.

Valuation is rich on a reported basis, with a trailing P/E of 87 and book value of just $7.59. Legal exposure remains live, and the China headline itself was smaller than market expectations, which is why the stock sold off.

Why Some Investors Will Want To Wait

Net income was essentially zero in Q1 ($-7M), and management’s guide calls for positive free cash flow of $1 billion to $3 billion with the second half doing the heavy lifting. BCA margins are not expected to turn positive until mid next year. Investors wanting confirmation can wait for a clean FCF-positive quarter and 737-10 certification before adding.

What The Tape And The Street Say

BA currently trades near $219.92, sitting on its 50-day moving average of $217.93. The consensus analyst target is $269.84, implying meaningful upside, though targets are one input, not a guarantee. Of 27 analysts, 21 rate it Strong Buy or Buy, 5 Hold, and 1 Strong Sell. Weekly RSI sits at 50.06, neutral and uncluttered.

The Verdict On Boeing At $220

At $220, Boeing is a Buy.

The path to appreciation is mechanical. Deliveries are rising, the 737 line is moving from 42 to 47 per month this summer to 52, the 787 is heading to 10 per month, and management is targeting 500 airplane deliveries in 2026. Each incremental jet flows into a backlog priced higher than units coming off the books, which is how margins inflect.

China is the asymmetric piece. Even partial honoring of the reported 200 to 750 aircraft framework would reshape mid-decade delivery economics. Defense is the second leg, with BDS revenue up 21% and management guiding to roughly 3.5% margins for the year on the way to high single digits.

What invalidates the thesis: another 777X slip, a China deal that evaporates, or a fresh quality event that throttles the 737 ramp. Watch the 737-10 certification, Q2 free cash flow, and any formal Beijing confirmation. Management views $10 billion of free cash flow as “very attainable” beyond 2026.

Buying Boeing here is buying a duopoly franchise mid-turn, before the cash flow shows up in the numbers.

Contact [email protected] for any questions or corrections.