Netflix (NASDAQ:NFLX | NFLX Price Prediction) terminated a Warner Bros. acquisition with a $2.8 billion fee, raised full-year free cash flow guidance to $12.5 billion, and built an ad business on pace to do $3 billion in 2026. Yet shares are down 25.42% over the past year and 5.5% year to date. Can NFLX hit $350 by 2027? Here’s the analysis.

Why Netflix Shares Are Stuck Despite Record Cash Flow

Netflix generates record cash, but the stock has declined. After peaking at $134.12 in the last 52 weeks, shares bottomed at $75.01 in February and now sit at $88.60. The one-month read is -4.98%, only partially offset by a 1.82% bounce over the past week.

Two factors weigh on sentiment. First, EPS of $1.23 in Q1 2026 missed $1.345 consensus, the second miss in three quarters. Second, with a beta of 1.548, Netflix amplifies macro volatility. Add a $700 million Brazilian tax overhang and competition from Alphabet, Amazon, Apple, and Disney, and the stock stalls.

Wall Street Sees Modest Upside. Our Model Sees Much More

The consensus target is $114.56, with 8 Strong Buys, 29 Buys, 12 Holds, no Sells, and 1 Strong Sell. Bullish sentiment sits at 74%.

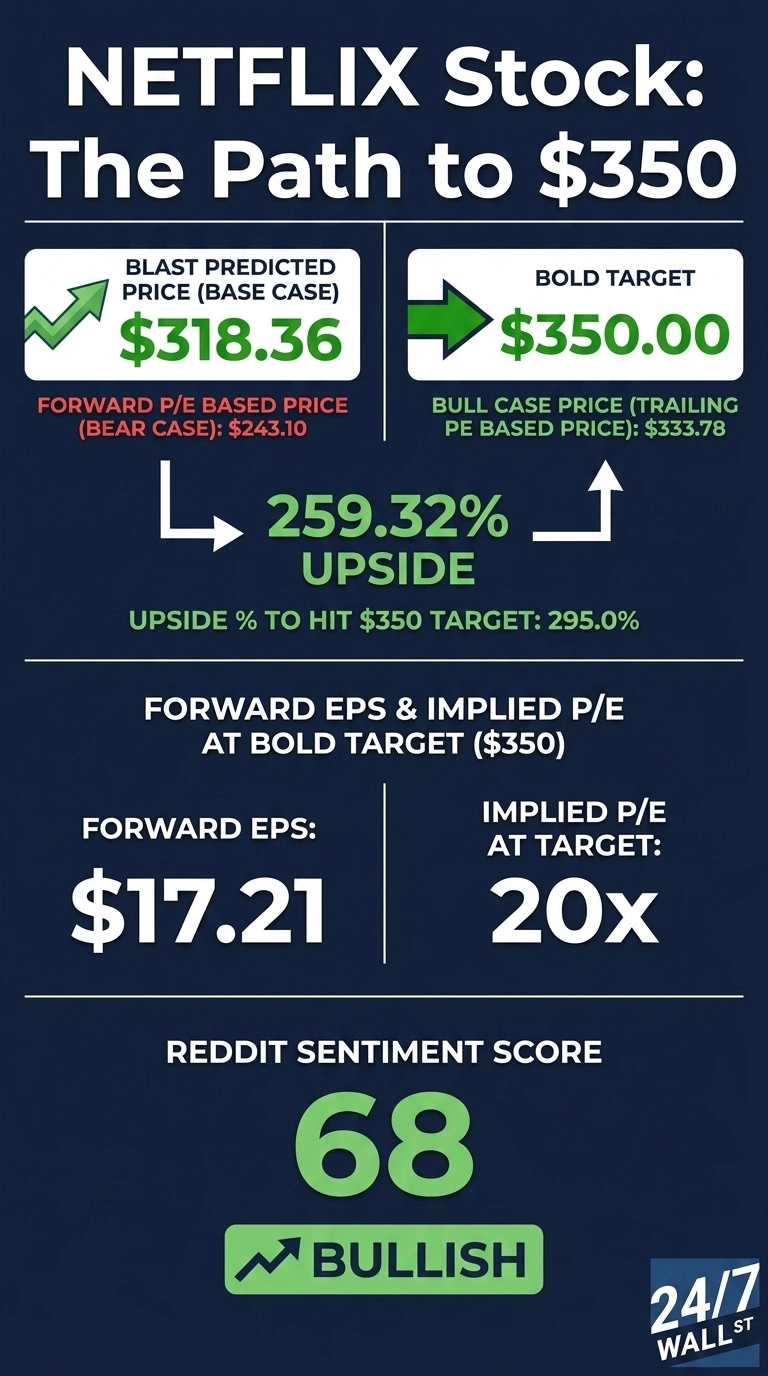

Our model is far more aggressive. The base case is $318.36, implying 259.32% upside, with a bull case of $333.78 and bear case of $243.10. Confidence reads 90%. Quarterly earnings grew 86.4% year over year, and analysts have been slow to update for the post-Warner Bros. capital return story.

The Path to $350 Per Share

Reaching $350 from today’s $88.60 requires a 295% gain. With forward EPS of $17.21, $350 implies a forward P/E of 20x. Our base case of $318.36 already implies 6x, meaning the target requires roughly 14x additional multiple expansion.

That sounds extreme until you see how compressed Netflix is relative to forward earnings. Ad revenue is on track to double to $3 billion, the ad-supported tier drove 60%+ of sign-ups in ads markets, and advertiser count jumped 70% to 4,000+ clients.

Co-CEO Greg Peters noted: “His vision, entrepreneurship, and steadfast commitment to our values have shaped every stage of our journey and continue to shape how Ted and I lead Netflix today.” Operating margin is guided to 31.5%, up from 29.5% in 2025. Content amortization peaking in Q2 2026 poses the primary risk to near-term margins.

Where Netflix Trades Today vs Its Earnings Power

At $88.60 against forward EPS of $17.21, Netflix trades at roughly 5x forward earnings. That is cheap for a company growing free cash flow 91.44% year over year. Shares sit 15% below the 52-week high of $134.12. The 10-year return is 805.1%. Current valuation does not reflect the cash machine Netflix has become.

Is $350 Realistic?

Hitting $350 requires a 295% gain. That is a stretch in 12 months, even with the model showing a $333.78 bull case.

Three things must break right: the forward P/E must expand from 5x to 20x as the market digests new earnings power, ad revenue must keep doubling, and the $6.8 billion remaining buyback authorization must be deployed aggressively. A content slate stumble that resets subscriber expectations would derail it. We’ve outlined the blueprint for how Netflix could reach $350 in 2027.