Software M&A is heating up again as private equity dry powder collides with depressed SaaS (software as a service) multiples and AI-driven stack consolidation among hyperscalers. Public market valuations have compressed enough that strategic buyers and private equity (PE) rollup specialists like Thoma Bravo, Vista, and Silver Lake are circling profitable, sticky enterprise software with recurring revenue and clear artificial intelligence angles. The setup mirrors the take-private wave that swept finance, security, and analytics software in prior cycles.

To rank acquisition likelihood, the most important filters are market cap digestibility, recurring revenue quality, free cash flow, strategic AI assets, founder or leadership transitions, and a beaten-down stock that frames a deal premium as both achievable and rewarding for existing shareholders. Three names check enough boxes to merit serious takeout speculation in 2026. Here, we count down to the most likely target.

3. Pegasystems

Pegasystems (NASDAQ: PEGA | PEGA Price Prediction) carries a market cap of roughly $6.3 billion, the largest of this trio and the hardest single bite. The workflow automation and decisioning platform would fit naturally inside Salesforce, ServiceNow, IBM, or Oracle, and the Pega Blueprint AI layer plus an enterprise installed base would appeal to a Thoma Bravo or Vista rollup of BPM assets.

The valuation case is mixed. Pegasystems missed badly in Q1, with revenue of $429.97 million falling 9.6% year over year and non-GAAP EPS of $0.46 against a $0.69 consensus. Shares trade at $37.93, down 36.5% year to date, on a forward multiple of 12x. Governance is a hurdle, as founder-CEO Alan Trefler controls a substantial voting bloc, and insiders hold 47.0% of shares. Pega Cloud ACV growth of 29% and a fresh $1.0 billion buyback signal that management still wants to drive its own outcome.

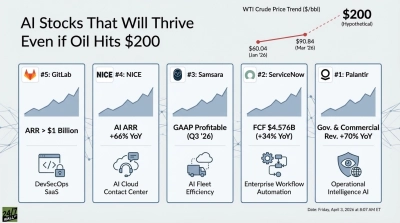

2. GitLab

GitLab (NASDAQ: GTLB) is the strategic asset on this list. The AI-native DevSecOps platform overlaps directly with Microsoft’s GitHub, which creates antitrust friction for Redmond but makes the company a defensive prize for AWS, Google Cloud, IBM/Red Hat, or Cisco.

GitLab crossed $1.0 billion in ARR in FY26, with Q4 revenue of $260.4 million up 23.2%, dollar-based net retention of 118%, and 155 customers spending more than $1 million annually. Free cash flow reached $219.6 million for the year. Shares trade at $33.79, down 25.8% over the past year, on an EV/Sales of 4.17x. CEO Bill Staples and a new CFO took the reins this year, and the board’s inaugural $400 million buyback hints at perceived undervaluation. The Duo Agent Platform, AI Catalog, and integrations with Claude Code, OpenAI Codex, and Google Gemini make this a strategically loaded asset at a digestible $5.7 billion market cap.

1. BlackLine

BlackLine (NASDAQ: BL) is the cleanest takeout setup in software for 2026. Mission-critical financial close software, a market cap of just $1.8 billion, a founder stepping back, and a stock cut nearly in half make BlackLine a textbook target for SAP, Oracle, Workday, or Intuit — or a private equity carve-up by Thoma Bravo or Vista.

Q1 FY26 revenue rose 9.7% to $183.16 million, non-GAAP EPS came in at $0.56 versus $0.45 expected, RPO surged 17.9% to $1.10 billion, and subscription revenue accounted for 94.9% of the total. Management raised full-year guidance to $765 million to $769 million in revenue with non-GAAP operating margin of 24.0% to 24.5%.

Shares trade at $31.32, down 43.4% year to date and 69.2% over five years, against an analyst target of $41.77. The company repurchased shares for $47.1 million in Q1, with $217.4 million still authorized. CEO Owen Ryan describes BlackLine as “the essential governance layer for the AI era,” citing Verity AI and Agentic Financial Operations. Therese Tucker’s transition to a founder role effective October 1, 2025, removes the last governance obstacle to a sale.

The Consolidation Backdrop

The broader software setup favors more deals, not fewer. PE take-privates continue to exploit the spread between public SaaS multiples and private market valuations, while strategic buyers are racing to consolidate AI-native platforms into their stacks before pricing resets higher. Pegasystems and GitLab fit that story. BlackLine occupies the sharpest intersection of all the M&A triggers: a small, accretive check size, recurring revenue tied to the financial close, an AI governance narrative CFOs already pay for, a founder stepping aside, and a stock the market has already discounted. Among the three, BlackLine will attract would-be acquirers first.