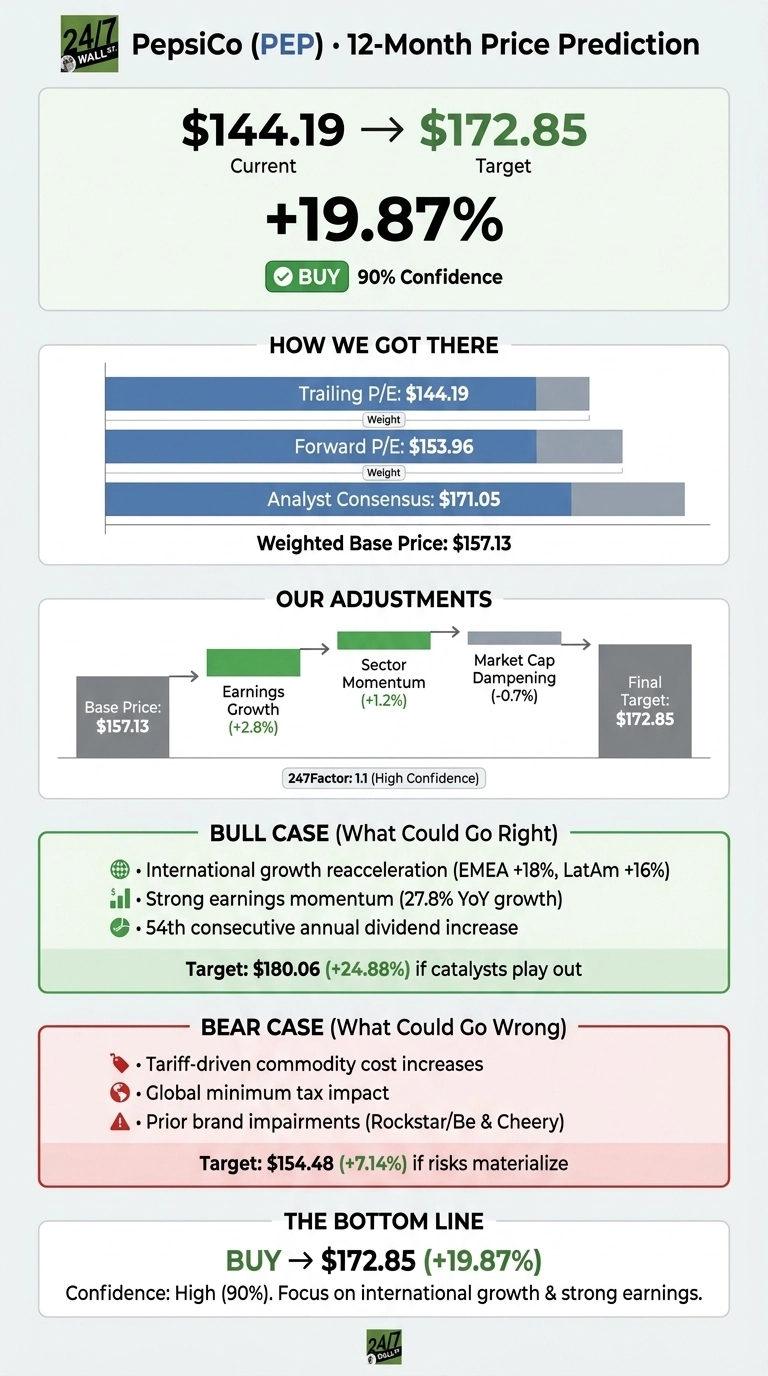

The question of whether PepsiCo (NASDAQ:PEP | PEP Price Prediction) can punch through to a new all-time high in 2026 is closer to a coin flip than the chart suggests. Shares trade at $144.19, sitting roughly 1% below the 52-week high of $169.96, but the stock has lost 7.15% over the last month. Our proprietary model frames that pullback as a setup worth watching.

Our 24/7 Wall St. price target for PepsiCo is $172.85, implying 19.87% upside over the next 12 months and a fresh all-time high. The recommendation is buy, and our confidence is high at 90%.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $144.19 |

| 24/7 Wall St. Price Target | $172.85 |

| Upside | 19.87% |

| Recommendation | BUY |

| Confidence Level | 90% |

An International Reacceleration Story

PepsiCo’s recent price action has been choppy. The stock is down 4.24% on the week and up just 1.36% year to date, though the one-year return of 13.67% reflects a sharp recovery off the $124.03 52-week low.

The Q1 FY26 report, released April 15, 2026, was the inflection. Core EPS came in at $1.61 against a $1.5442 consensus, revenue hit $19.44 billion, and operating margin expanded 210 basis points to 16.5%.

The international story is doing the heavy lifting. EMEA grew 18%, Latin America Foods 16%, and Asia Pacific Foods 11%. CEO Ramon Laguarta noted the quarter featured “an acceleration in both net revenue and organic revenue growth, with a notable improvement in convenient foods organic volume.”

The Case for $180+

The bull setup is straightforward. PepsiCo’s FY26 guidance calls for core constant currency EPS growth of 4-6%, with reported growth approaching 5-7% once FX and M&A are layered in.

Forward P/E of 17x is modest for a Dividend Aristocrat on its 54th consecutive annual hike, with $8.9 billion of cash returns planned this year. Our bull case projects $180.06 by June 2027, a 24.88% total return that would clear the ATH cleanly. Of 23 covering analysts, 8 rate PEP Buy or Strong Buy, with consensus at $171.05.

What Could Go Wrong

The risks are real. Tariff-driven commodity costs hit Pepsi Beverages North America with an 11-percentage-point input cost headwind last quarter, and global minimum tax regulations are shaving roughly 2 points off reported EPS growth. PEP also booked $1.993 billion in Rockstar and Be & Cheery intangible impairments in 2025, and recent insider activity skews to net selling.

Bulls would counter that the impairments are non-cash legacy cleanup and that the underlying core EPS of $8.14 for FY25 still beat consensus. Our bear case lands at $154.48, still positive but well short of an ATH.

Where the Setup Stands

The 24/7 Wall St. price target is $172.85, the recommendation is buy, and confidence sits at 90%. The factor tipping the scale is the combination of an international segment growing double digits and a forward P/E under 17 on a Dividend Aristocrat yielding nearly 3.9%.

The bullish thesis strengthens if the July 13 Q2 earnings report confirms North America volume continues its turn positive. It weakens if tariff pass-through stalls and PBNA margins compress further. On balance, the risk/reward skews constructive into a potential new high.

PepsiCo Price Prediction 2026-2030

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $172.85 |

| 2027 | $188.00 |

| 2028 | $205.00 |

| 2029 | $226.00 |

| 2030 | $251.45 |

These projections assume PepsiCo continues compounding core EPS in the mid-single digits while the international business sustains its double-digit operating profit trajectory. Significant upside could come from a poppi-led functional beverage breakout. Downside would emerge from a structural shift away from carbonated and salty snack categories.