SoFi Technologies (NASDAQ: SOFI | SOFI Price Prediction) doesn’t have a ten-year track record on the public markets, so let’s set expectations up front. The company went public via SPAC merger with Social Capital Hedosophia V in June 2021, which means we only have a 5-year window plus a 1-year snapshot to work with. Still, that window covers one of the wildest round trips in fintech.

From Student Loan Refi to a Digital Bank With a Stablecoin

SoFi started in 2011 as a student loan refinancing shop and spent the last few years morphing into something much bigger. It bought Galileo in 2020, picked up a national bank charter in early 2022 by acquiring Golden Pacific Bancorp, and now runs lending, brokerage, a credit card, and a tech platform under one roof. In the last year alone it rolled out crypto trading, the SoFiUSD stablecoin, and blockchain remittances through a Mastercard partnership.

The numbers caught up to the story. FY2025 revenue hit $3.61 billion, up 38.32% year over year, and Q4 2025 was the first billion-dollar revenue quarter in company history. Q1 2026 brought record loan originations of $12.18 billion, up 68% YoY, with membership up 35%.

Your $1,000 Survived a 79% Drawdown to End Up Underwater

1-Year Return (June 2025 to June 2026)

- Initial Investment: $1,000

- Current Value: $1,172.60

- Total Return: 17.26%

- S&P 500 (same period): $1,243.70 (24.37%)

5-Year Return (June 2021 to June 2026)

- Initial Investment: $1,000

- Current Value: $769.90

- Total Return: -23.01%

- Annualized Return: -5.10%

- S&P 500 (same period): $1,745.30 (74.53%, about 11.78% annualized)

The 5-year picture hides the trauma. Anyone who bought near the SPAC debut watched SOFI fall 79.65% from $22.65 to $4.61 between June 2021 and December 2022 as rates spiked and the student loan moratorium dragged on. The recovery was real, but the stock has whipsawed again in 2026, down 38.77% year-to-date from a peak near $30.

I’d Buy It Here, But Only With a Three-Year Stomach

I’d put $1,000 into SoFi today if I believed management can hit the medium-term plan of 30%+ adjusted revenue CAGR and 38-42% adjusted EPS CAGR through 2028. The deposit franchise sits at $40.24 billion, funding over 90% of liabilities, and a 43% cross-buy rate says the one-stop-shop pitch is actually landing.

I’d avoid it if I’m worried about credit. Personal loan charge-offs climbed to 3.03%, Technology Platform revenue dropped 27% YoY on a client departure, and a forward P/E of 29 with a beta of 2.15 leaves zero room for a recession scare.

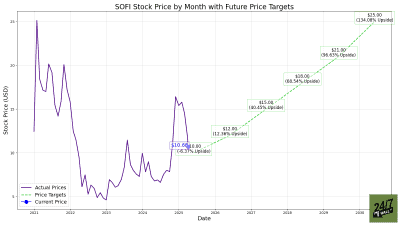

I lean buy at $16, but only with money I can leave alone for three years. The real prize beyond the $21 analyst target is compounding through the next cycle.

Contact [email protected] for any questions or corrections.