Apple’s (NASDAQ:AAPL | AAPL Price Prediction) stock hit a fresh all-time high around $317.40 in late May, then slid 7.82% in a week as investors digested CEO succession news, valuation concerns, and softer sentiment.

With Tim Cook delivering his final WWDC keynote and Siri AI getting its overhaul, the next 12 months are pivotal. Here is what our model says about where shares of Apple are headed.

Our 24/7 Wall St. Price Target for Apple

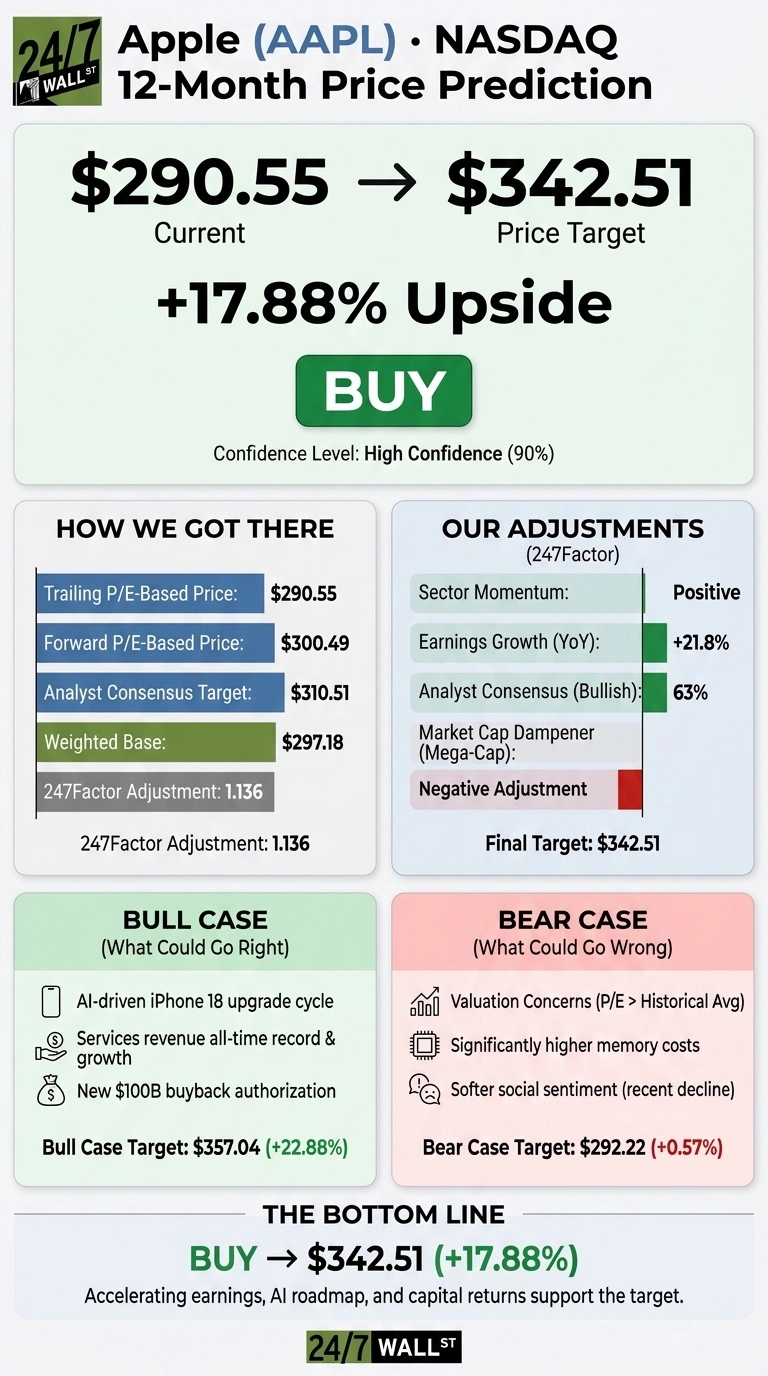

Our 24/7 Wall St. price target for Apple is $342.51 over the next 12 months, implying 17.88% upside from the current $290.55 price.

We rate Apple a buy with high confidence (90%). Accelerating earnings, a refreshed AI roadmap, and a $100 billion buyback authorization give this name a clearer path higher.

| Metric | Value |

|---|---|

| Current Price | $290.55 |

| 24/7 Wall St. Price Target | $342.51 |

| Upside | 17.88% |

| Recommendation | BUY |

| Confidence Level | 90% |

A Cook Farewell, A Siri Reboot, and a Q2 Blowout

Apple is up 44.8% over the past year and 7.07% year to date, though the past month has cooled (down 0.85%). Shares sit roughly 2% off the 52-week high of $317.40.

Q2 26 delivered: revenue of $111.2 billion, up 17% YoY, iPhone revenue of $57 billion, up 22%, and Services hitting an all-time record of $31 billion. EPS of $2.01 topped expectations, marking nine consecutive beats.

At WWDC this week, Apple unveiled a significant overhaul of Siri, branded Siri AI, alongside expanded child-safety tools. It was also Tim Cook’s final WWDC keynote before John Ternus takes over as CEO in September.

Why Bulls See a Breakout Ahead

The bull case rests on three pillars: AI-driven iPhone upgrades, Services compounding, and capital returns. Cook told investors R&D is “accelerating much higher than the company overall”, and the new Siri AI rollout could drive a real upgrade catalyst.

Greater China grew 33% in the first half, MacBook Neo is supply-constrained on “off the charts” demand, and June-quarter guidance calls for 14% to 17% revenue growth. Apple authorized a new $100 billion buyback and raised the dividend 4%. The bull-case scenario points to $357.04, a 22.88% total return.

The Risks Worth Watching

The bear case starts with valuation. Apple trades at a trailing P/E of 38 and forward P/E of 32, well above its historical average. Reddit’s loudest thread argued there is “underappreciated risk of AAPL re-rating significantly downward”, and the composite sentiment score has fallen 17.48 points over 30 days.

Cook flagged “significantly higher memory costs” for the June quarter, and Polymarket traders peg the highest probability June close at just $280.

Insider activity skews net selling. The counter is that memory pressure reflects deliberate investment in AI silicon to support AI workloads. The bear-case scenario settles at $292.22, essentially flat.

Apple Price Prediction 2026-2030

My verdict is buy with a 24/7 Wall St. price target of $342.51 and 90% confidence. Earnings acceleration meets a credible AI catalyst at a moment when sentiment has reset lower. The bull thesis hinges on Siri AI driving a meaningful iPhone 18 upgrade cycle. The key risk is memory costs compressing product margins below 37% for multiple quarters.

Here is where our model projects Apple could trade, assuming current growth trajectories hold.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $342 |

| 2027 | $378 |

| 2028 | $415 |

| 2029 | $450 |

| 2030 | $486 |

These projections assume Apple executes on Services growth and AI integration. Significant upside or downside could come from a foldable iPhone launch, regulatory action on the App Store, or faster-than-expected Services deceleration.