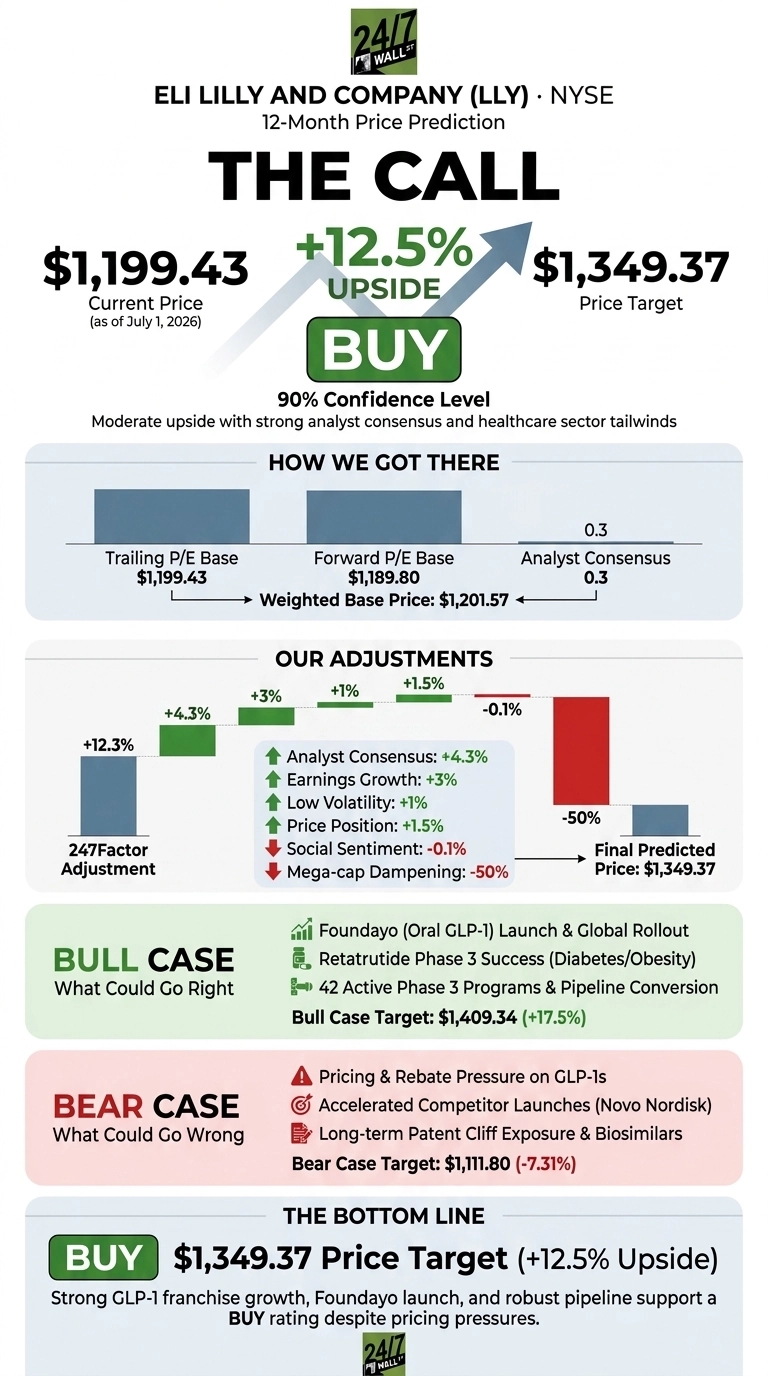

Our 24/7 Wall St. price target for Eli Lilly (NYSE:LLY | LLY Price Prediction) is $1,349.37, pointing to 12.5% upside from a recent price of $1,199.43. We rate LLY a buy with a 90% confidence score. The GLP-1 franchise is compounding faster than the market appreciated last spring, and Foundayo just opened a scalable oral channel to more than 1 billion people globally.

| Metric | Value |

|---|---|

| Current Price | $1,199.43 |

| 24/7 Wall St. Price Target | $1,349.37 |

| Upside | 12.5% |

| Recommendation | BUY |

| Confidence Level | 90% |

A Recovery Rally Built on Foundayo and a Q1 Blowout

Lilly has been one of 2026’s cleanest turnaround stories. Shares are up 8.34% in the past week, 8.55% over the past month, and 11.99% year-to-date, after climbing off an August 2025 low near $701. The stock now sits about 1% from its 52-week high of $1,238.

Q1 2026 lit the fuse. Revenue of $19.799 billion grew 55.5% year over year, and non-GAAP EPS of $8.55 beat consensus by 25.88%. Mounjaro delivered $8.662 billion (125% growth), Zepbound added $4.160 billion, and management raised full-year revenue guidance to $82 billion to $85 billion with EPS of $35.50 to $37.

The Case for $1,400+: Why Bulls See a Breakout Ahead

Our bull case target is $1,409.34, a 17.5% return. The engine is the incretin franchise. Combined Mounjaro and Zepbound revenue hit $12.8 billion in Q1, and international volume grew 81%.

Foundayo, the first oral GLP-1 with no food or water restrictions, is already tracking with 80% of prescriptions going to new-to-class patients, expanding the market rather than cannibalizing injectables.

Retatrutide’s Phase III diabetes readout showed 11.1 to 16.6 kilograms of weight loss, and the pipeline runs 42 active Phase III programs. Wall Street’s consensus target sits at $1,222.62, with 24 Buy ratings.

The Risks Worth Watching

Our bear case is $1,111.80, a 7.31% pullback. Realized prices fell 13% in Q1 as rebates, Zepbound cash-pay cuts, and China’s NRDL inclusion took bites out of net revenue.

Bulls will counter that volume grew 65% and gross margin still landed at 82.6%, so unit economics remain excellent. Insider activity leaned toward selling with 15 recent transactions, though heavy investment in four acquisitions and $584 million in IPR&D charges are cash going into future growth, not fundamental deterioration. Novo Nordisk competition and potential pharmaceutical tariffs remain overhangs.

The Bottom Line: A BUY Rating on Lilly

My 24/7 Wall St. price target is $1,349.37, a buy with 90% confidence. The tipping factor is the guidance raise: management moved both revenue and EPS ranges higher after just one quarter, and Foundayo contribution is barely in the numbers yet.

The setup strengthens if Foundayo’s Q3 DTC launch drives another guidance hike. The thesis weakens if pharmaceutical tariffs materialize or Q2 price erosion accelerates beyond the low-to-mid teens management has guided.

Looking further ahead, here is where our model projects Lilly could trade if current growth and margin trajectories hold.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 (year-end) | $1,263.70 |

| 2027 | $1,349.37 |

| 2030 | $1,798 |

These projections assume Lilly sustains GLP-1 leadership, executes the Foundayo global rollout, and its 42 Phase III programs deliver meaningful pipeline conversion. Significant upside could come from retatrutide approval; downside risk stems from patent-cliff exposure and accelerating biosimilar competition later in the decade.

Contact [email protected] for any questions or corrections.