For much of the past three years, Wall Street has treated artificial intelligence as a single trade. Buy the chipmaker, sell the laggard, repeat. Jay Jacobs of BlackRock, speaking with Troy Millings on the Earn Your Leisure podcast, drew a sharper line. The AI trade is short. The AI investment, he argued, "is going to be a decade." That distinction matters more than any single earnings report, because history says the surplus from infrastructure manias rarely lands where the first wave of money expected it to.

Jacobs broke the opportunity into three phases. Today’s winners sit in infrastructure: data centers, power, and semiconductors. The next phase belongs to companies implementing AI into their businesses. The third, further out, is "real-world AI" like autonomous vehicles and robotics. What’s particularly useful about this map is that the historical precedents already exist. We have walked this hallway before.

Phase 1: The picks-and-shovels story is loud

Start with the obvious. NVIDIA (NASDAQ:NVDA | NVDA Price Prediction) printed $81.615 billion in Q1 FY27 revenue, up 85% year over year, with Data Center revenue of $75.246 billion, up 92%. Jensen Huang called it "the largest infrastructure expansion in human history." Total supply commitments reached $119.0 billion, and the board approved an additional $80.0 billion buyback.

The supplier ring around NVIDIA is moving faster. Marvell (NASDAQ:MRVL) has vaulted 303% over the past year, trading at a 96 trailing P/E and 69x forward. Micron (NASDAQ:MU) has skyrocketed 747% in twelve months, with Q2 FY26 revenue of $23.86 billion, up 196% year over year. CEO Sanjay Mehrotra said "in the AI era, memory has become a strategic asset."

I’ve been watching infrastructure cycles for two decades now, and the pattern rhymes. From 1996 to 2001, telecoms spent roughly $500 billion laying fiber. Capacity was overbuilt. Cisco fell about 89% from its 2000 peak. Yet internet usage rose tenfold over the following decade, and the application layer that grew on top of those wires minted Google and Amazon. Britain’s 1840s railway mania tripled track mileage and wiped out the equity. The rails ran for a century. In the 1920s, utilities built out rural electrification, crashed in 1929, then powered American productivity through the 1950s.

The precedent is consistent. Phase 1 rewards the shovel makers first, then punishes them on overbuild, then hands the surplus to Phase 2.

Phase 2: The platforms with structural moats

Jacobs leaned into the mega-cap advantage. Big companies, he said, hold "really entrenched moats" through proprietary data, engineering talent, and cheap capital, and they "are going to spend close to a trillion dollars this year on CapEx." The receipts back him up.

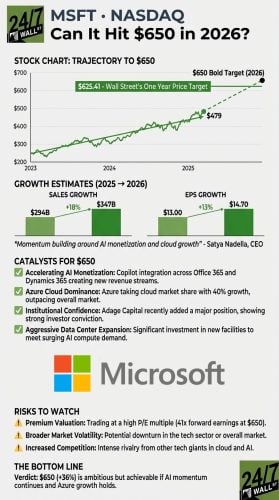

Microsoft (NASDAQ:MSFT) reported its AI business at a $37 billion annual run rate, up 123% year over year, with commercial remaining performance obligations of $627 billion and Q3 FY26 capex of $30.88 billion, up 84%. Satya Nadella said "our AI business surpassed an annual revenue run rate of $37 billion, up 123% year-over-year."

Alphabet (NASDAQ:GOOGL) reported Q1 2026 Google Cloud revenue of $20.03 billion, up 63%, with backlog nearly doubling quarter on quarter to over $460 billion and 2026 capex guidance of $175 to $185 billion. Gemini is now processing 16 billion tokens per minute. I own Alphabet, bought in April 2012, and the valuation gut-check still surprises me: a 16 P/E on a business compounding cloud at 60%-plus. Compare that to Marvell at 69x forward and the price-of-admission gap between Phase 1 and Phase 2 becomes visible.

Note the divergence in market response. Microsoft is down 18% over one year, even with the run-rate doubling. Crowds at Polymarket pin a 53.5% probability on a June close near $375. The platforms are doing the work. The stock is reluctant.

Phase 3: Real-world AI is still early

Jacobs was direct about the third phase. Real-world AI "is much harder AI" and more compute intensive, which is why it remains early-stage. Tesla is the loudest single bet on the thesis: active FSD subscriptions of 1.28 million, up 51%, an Optimus line in Fremont designed for 1 million robots per year, and a trailing P/E above 400. Polymarket assigns only a 3.1% probability to a California robotaxi launch by June 30 and 0.8% probability to an Optimus commercial release this month. The crowd is signaling the story is real but the timing is years out.

The long memory

Here is what I keep coming back to. Buy NVIDIA, Marvell, and Micron IF you believe the capex cycle has more years to run. Buy Microsoft and Alphabet IF you believe the platforms capture the application-layer surplus the way Google and Amazon did after 2001. Buy Tesla IF you believe Phase 3 lands inside this decade and not the next.

The honest answer, the one Jacobs settled on, is that it will be "a little bit of a blend." Long term, Wall Street tends to absorb the overbuild and reroute capital to the platforms and applications that monetize it. Short term, the trade has been concentrated. The investment, if history holds, will be wider, slower, and more durable than the current stock action suggests.

Contact [email protected] for any questions or corrections.