Comcast’s (NASDAQ: CMCSA | CMCSA Price Prediction) move to carve out its cable networks into the Versant spinoff marks a definitive turning point in the great conglomerate unbundling: the notorious “conglomerate discount” that has eroded shareholder value for over a decade is officially on the chopping block across the S&P 500.

The strategy isn’t just theory but is actively delivering results. Look no further than Honeywell International (NASDAQ: HON), whose shares have surged 16.8% year to date through June 29. As the century-old industrial giant executes its own historic breakup, Wall Street is making it clear that leaner, more focused businesses are winning the market. More conglomerates are sitting on the same setup. Here is the ranked list of who the market is pricing for a split next.

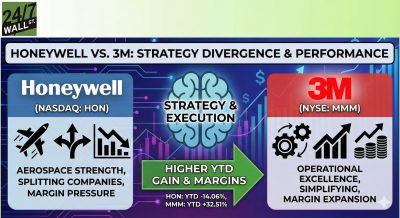

1. Honeywell: The Blueprint Is Already Live

The surprise pick is the one already pulling the trigger. Honeywell is a breakup in motion, and that is precisely why it leads this list. This demonstrates in real time what the market does when management stops defending a conglomerate structure and starts dismantling it. The Aerospace spin-off (HONA) is completed, Solstice Advanced Materials already trades as SOLS, and the Productivity Solutions and Warehouse Workflow units are being sold to Brady and (likely) American Industrial Partners, respectively.

The numbers behind the move reveal why management capitulated. Q1 FY26 segment revenue split into Aerospace Technologies at $4.32 billion (+4%), Building Automation at $1.88 billion (+11%), and Industrial Automation at $1.42 billion (−11%)—four businesses pulling in four directions inside one holding company. Adjusted EPS of $2.45 beat the $2.32 estimate, while the backlog hit $38.3 billion. CEO Vimal Kapur called it the “final steps to conclude our multi-year portfolio transformation.”

If Honeywell is the blueprint, the next name on the list is the one every activist on Wall Street has been circling for three years.

2. Disney: ESPN Is Already Standing on Its Own Two Feet

Walt Disney (NYSE: DIS) has the cleanest sum-of-the-parts gap on the board. Entertainment, Sports, and Experiences are three distinct businesses with three distinct multiples, and the market is treating the whole at the multiple of the slowest piece. Shares are down 13.3% year to date while the parks business sets records. The ESPN-NFL Network swap, in which ESPN acquired NFL Network in exchange for a 10% noncontrolling interest in ESPN, looks very much like the architecture one would build before separating a business.

The Q2 FY26 segment data underlines the divergence. Entertainment revenue of $11.72 billion grew 10%, Sports/ESPN posted $4.61 billion at +2%, and Experiences delivered a record $9.49 billion at +7%. Inside Entertainment, SVOD revenue of $5.49 billion grew 13%, and operating income surged 88% to $582 million. Three engines, three growth rates, one stock trading at a forward P/E of 13x.

If Disney’s discount is the most-discussed in media, the next name on this list is the most untouchable conglomerate in American finance, and the post-founder era has just begun.

3. Berkshire Hathaway: The Post-Buffett Test

Berkshire Hathaway (NYSE: BRK-B) is the ultimate conglomerate, and the question of whether insurance, BNSF, Berkshire Hathaway Energy, and the equity portfolio belong under one roof has been off-limits for 60 years. It is no longer off-limits. Shares are down 1.3% year to date through June 29 at $496, lagging the broader market while the company holds a fortress balance sheet. New CEO Greg Abel inherits a structure that, by sheer scale, invites the sum-of-the-parts conversation.

The valuation math is what makes this credible. Berkshire trades at a P/E of 15 and a P/B of 1.47, with a free cash flow yield of 3.61%. Operating margin is 15.9% with interest coverage of 11.6x, the kind of balance sheet that would let any one of the wholly-owned units stand alone immediately. Whether Abel ever pulls a thread is speculation, but the structural setup is unambiguous: this is the largest holding company on the New York Stock Exchange, and the discount is no longer protected by personality.

From the most fortified balance sheet in America to one of the most fragile, the next name has been openly speculated as a defense-versus-commercial split for years.

4. Boeing: Defense Prints Cash, Commercial Still Bleeds

Boeing (NYSE: BA) has already shown it is willing to surgically remove pieces. The $9.67 billion gain on the divestiture of Digital Aviation Solutions in Q4 FY25 proved CEO Kelly Ortberg will sell what does not fit. The deeper structural question, the one analysts have circled since the MAX crisis, is whether Defense, Space & Security belongs inside the same legal entity as a Commercial Airplanes franchise still operating at a −6.1% margin.

Q1 FY26 made the divergence concrete. Commercial Airplanes revenue of $9.20 billion grew 13%, Defense Space & Security hit $7.60 billion at +21% with operating earnings up 50% to $233 million, and Global Services posted $5.37 billion at +6%. Total backlog ramped to a record $695 billion, while debt was cut to $47.2 billion from $54.1 billion. Shares trade roughly flat year to date at $214.69, while the underlying defense business compounds at a rate that the consolidated reporting completely obscures.

Speculation about a defense carve-out is just that, speculation. Yet the divestiture machinery is already warm.

5. Intel: The Spin That Could Reprice the Entire Sector

The payoff slot belongs to Intel (NASDAQ: INTC), where the foundry-versus-products split is the single largest potential value unlock in semiconductors. CEO Lip-Bu Tan has not announced a separation, but every operational move points in one direction. Nvidia bought $5.0 billion of Intel common stock, the U.S. government took significant equity via CHIPS Act, and a multiyear Google partnership for custom ASIC IPUs all sit beside a Foundry unit still burning roughly $2.5 billion per quarter in operating losses. The market has noticed: shares are up 257.0% year to date.

Q1 FY26 made the segment divergence impossible to ignore. Client Computing revenue of $7.73 billion grew just 1%, Data Center & AI hit $5.05 billion at +22%, and Intel Foundry posted $5.42 billion at +16%. Non-GAAP EPS of $0.29 demolished the $0.0127 estimate, the sixth straight quarter of revenue above expectations. With headcount cut to 85,100 from 108,900 and a $4.07 billion restructuring charge already booked, the foundation for a separation has been laid.

Foundry as a standalone CHIPS-backed pure play, Products as a profitable design house anchored by Data Center & AI: that is the bull case the market has begun to price, and Reddit chatter has tracked it closely, with peak activity on June 26 at 303 upvotes and 163 comments, as the restructuring story developed.

The Market Has Already Spoken

Comcast made the playbook explicit, while Honeywell ran it and rerated. Disney has rebuilt ESPN’s legal architecture for separation. Berkshire’s post-founder era removes the cultural moat protecting the holding company structure. Boeing has already proven it will divest, and Intel’s foundry losses make the spin math straightforward. The conglomerate discount used to be a structural inevitability. In the current cycle, it is a closing window.

Contact [email protected] for any questions or corrections.