Microsoft (NASDAQ:MSFT | MSFT Price Prediction) has been brutalized in 2026, down 26.72% year to date and 7% in the past week alone, even as fundamentals accelerate.

With shares at $352.83 heading into the final trading days of June 2026, the question is whether this is capitulation or the start of something worse. Our model says capitulation, and the setup over the next 12 months looks asymmetric to the upside.

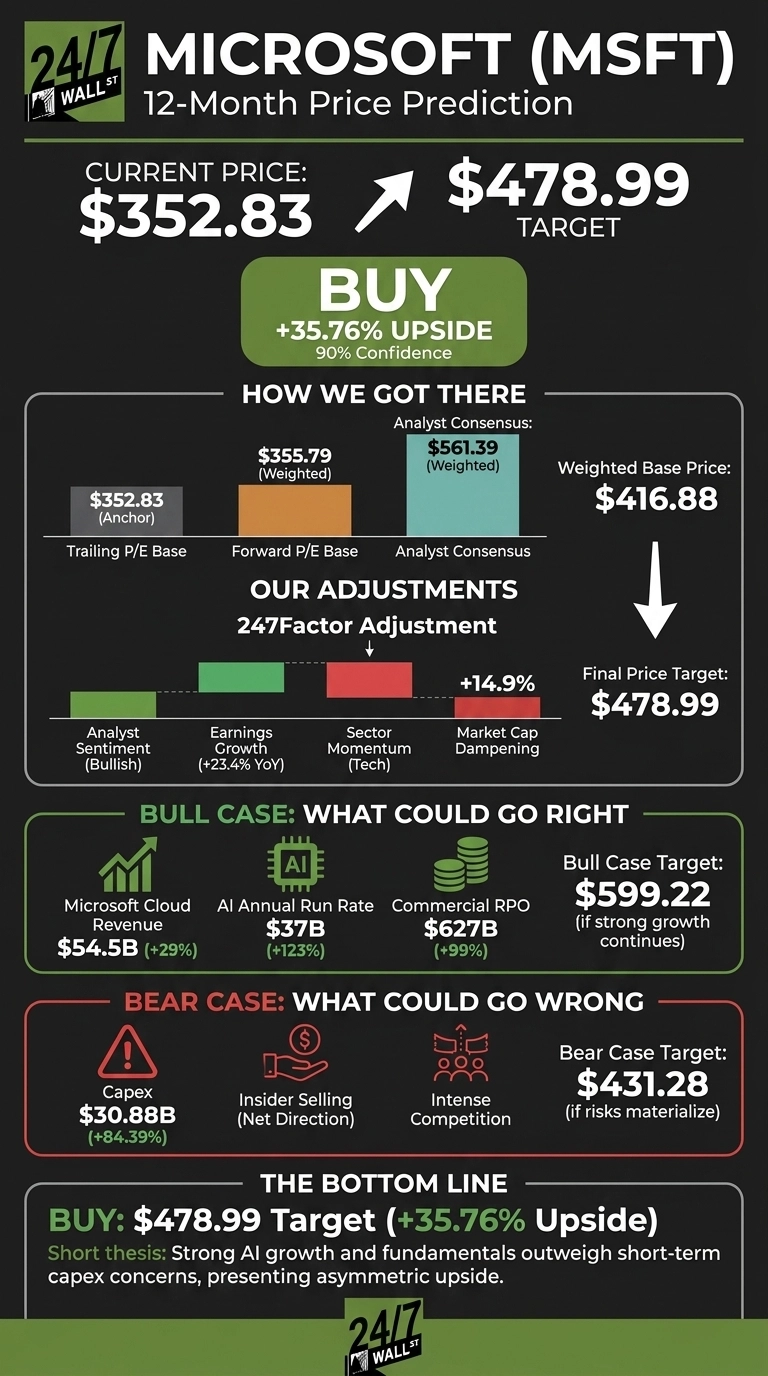

The 24/7 Wall St. Price Target for Microsoft

Our 24/7 Wall St. price target for Microsoft is $478.99 over the next 12 months, implying 35.76% upside from current levels. We rate MSFT a buy with 90% confidence. Prediction markets imply 67.5% probability that MSFT finishes this week near $350 and 76.6% probability of closing above $345 at month end.

| Metric | Value |

|---|---|

| Current Price | $352.83 |

| 24/7 Wall St. Price Target | $478.99 |

| Upside | 35.76% |

| Recommendation | BUY |

| Confidence Level | 90% |

A Selloff That Has Outrun the Fundamentals

MSFT is off 27.75% over the past year and 15.19% in the last month, with shares falling 3.46% on June 25 alone.

Yet the Q3 FY26 earnings report showed the fourth consecutive EPS beat: $4.27 EPS on revenue of $82.89 billion (+18.3% YoY). Azure grew 40%, the AI business crossed a $37 billion annual run rate (+123% YoY), and commercial RPO ballooned to $627 billion, nearly double the prior year.

The bear story centers on capex. Q3 capital expenditures hit $30.88 billion, up 84.39% YoY, and a viral r/wallstreetbets post titled “Satya and Zuckerberg are incinerating capital” drew over 1,000 upvotes. That tension between earnings growth and infrastructure spend explains the selloff better than any deterioration in the business.

The Case for $599 and Beyond

Our bull case price is $599.22, or 69.83% upside. Microsoft Cloud reached $54.5 billion in quarterly revenue growing 29%, and the restructured OpenAI partnership extended Microsoft’s IP rights through 2032 and locked in a $250 billion incremental Azure commitment from OpenAI.

With analyst consensus at 52 buy ratings, 3 hold, 0 sell and a Street target of $561.39, even partial rerating to historical multiples gets shares back near $500. One r/stocks post noted “Microsoft is now cheaper than the April 2025 Tariff crash, yet TTM EPS is up 30%”.

What Could Drag Shares to $431

Our bear case lands at $431.28, still 22.23% above the current quote, showing how much pessimism is already priced in. Capex doubled, OpenAI investment losses widened to $3.1 billion in Q1 FY26, and insiders have been net sellers across 33 recent transactions.

Bulls counter that capex funds the RPO backlog that grew 99%, and OpenAI losses are paper marks against a stake Microsoft values near $135 billion.

Microsoft Price Prediction 2026-2030

The 24/7 Wall St. price target of $478.99 reflects a buy with 90% confidence. The disconnect between a 22x forward multiple and 123% AI growth on a $37 billion run rate tips the scales.

The model favors accumulation on a 12-month horizon, with tolerance for capex-driven volatility built into the thesis. The thesis weakens if FY27 Azure growth decelerates below 30% or commercial RPO conversion slows materially.

Our model projects Microsoft could trade as follows, assuming current growth and AI monetization trajectories hold.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $405 |

| 2027 | $478.99 |

| 2028 | $575 |

| 2029 | $695 |

| 2030 | $835 |

These projections assume Microsoft sustains Azure and Microsoft 365 growth while capex returns on AI infrastructure begin flowing through to operating margins. Material upside could come from agentic computing monetization at scale; downside risk centers on sustained AI capex overbuild without commensurate revenue conversion.

Contact [email protected] for any questions or corrections.