Meta Platforms (NASDAQ:META | META Price Prediction | META Price Prediction) is the AI story hiding in plain sight. The stock trades at $612.91, down 6.99% year to date, while the underlying business just posted 33% revenue growth and a 41% operating margin.

Mark Zuckerberg told investors “we are on track to build a leading lab” after releasing Muse Spark from Meta Superintelligence Labs. Can this stock climb to $900 in 2027? I think it can, and here is exactly what needs to happen.

Why Meta Shares Are Stuck Despite Blowout Earnings

The market is punishing Meta for spending. Full-year 2026 CapEx guidance was raised to $125 to $145 billion, and total expenses will land between $162 and $169 billion. Shares fell 8.55% the day after a Q1 earnings release that beat EPS estimates by 56.79%. Investors saw the compute bill and blinked.

The one-month move of +2.16% and one-year return of -14.51% tell the story of a stock trapped between AI hope and AI capex fatigue. A beta of 1.229 means every macro tremor gets amplified.

Wall Street Sees Big Upside. Our Model Sees More.

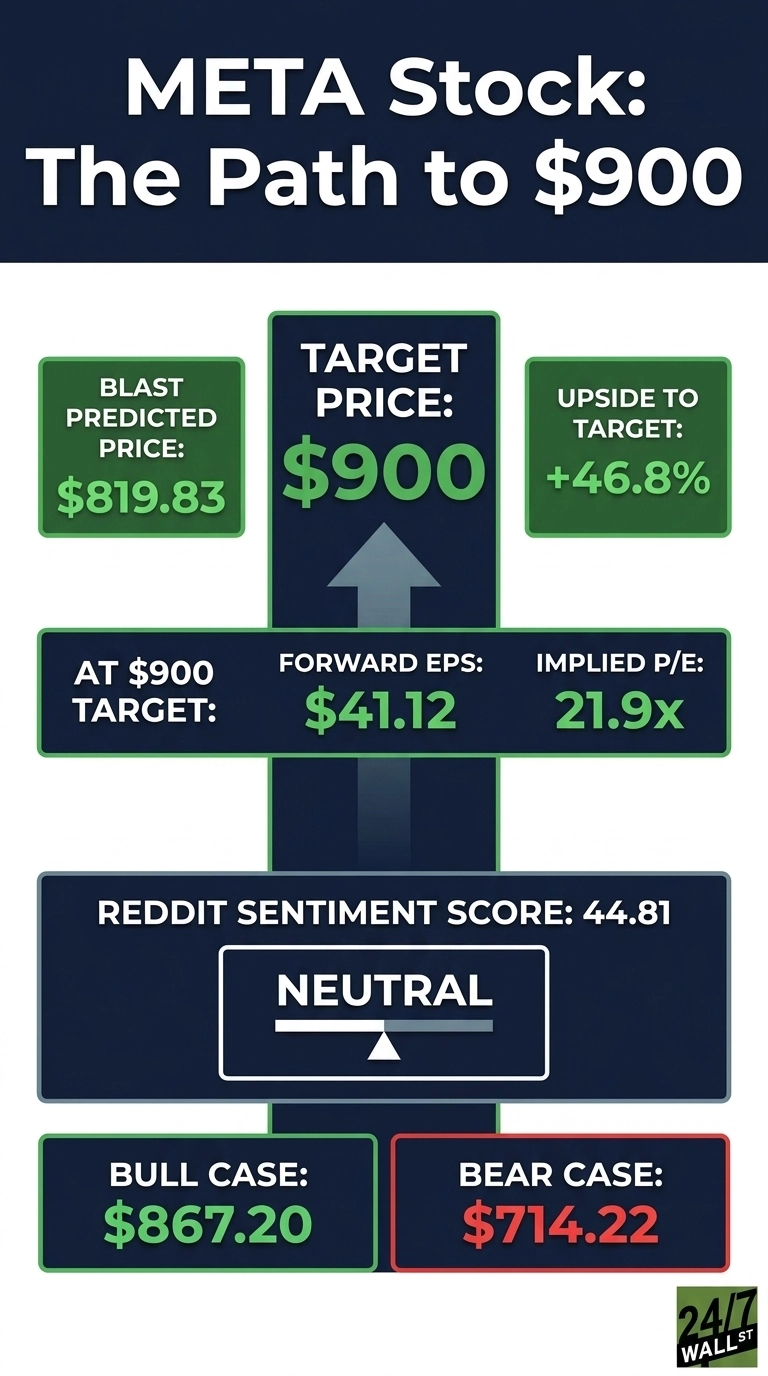

The consensus target sits at $827.32, backed by 8 strong buys, 49 buys, and 7 holds, with zero sells. That is 89% bullish sentiment. Our base-case model lands at $819.83 for a 1-year target, implying 33.76% upside, with a bull case of $867.20 and a bear case of $714.22. Confidence: 90%.

Analyst estimates have been consistently too low. Q1 2026 EPS beat by 7.18%, Q4 2025 by 8.03%, and Q2 2025 by 21.84%. Quarterly earnings growth of 62.4% is not showing up in most models. Consensus is anchored to yesterday’s Meta.

The Path to $900 Per Share

Reaching $900 from today’s price of $612.91 would require a gain of 46.8%. That is aggressive but not unhinged for a stock with a beta above 1.2 and this earnings profile.

With forward EPS of $41.12, a price of $900 implies a forward P/E of 22x. Our base case of $819.83 already implies 18x, meaning the bold target requires roughly 3.7x of additional multiple expansion. That is achievable if EPS growth keeps outrunning consensus and the market re-rates Meta as an AI compute owner, not just a spender.

CFO Susan Li said “Q1 total revenue was $56.3 billion, up 33%” and that business AI conversations scaled from 1 million to 10 million weekly. Zuckerberg added, “we are on track to deliver personal superintelligence to billions of people.” The primary risk is that CapEx keeps climbing without matching revenue conversion.

Where Meta Trades Today vs Its Earnings Power

At $612.91, Meta trades at a forward P/E of just 15x. For a business growing revenue in the low 30s and EPS in the 60s, that is cheap. The stock sits 4% below its 52-week high of $793.65 and well off the low of $519.78. Ten-year returns of 441.4% confirm the long-term compounding case. Any multiple recovery toward 22x on rising EPS gets you to $900.

The Bottom Line on $900

Meta needs to gain 46.8% to hit $900. I think it is a credible stretch for 2027.

Three things need to go right: Q2 revenue lands at the high end of the $58 to $61 billion guide, Reality Labs losses stop widening, and the Muse model family drives visible monetization gains. What derails it is a CapEx overrun without corresponding revenue leverage. We’ve outlined the blueprint for how Meta Platforms could reach $900 in 2027.

Contact [email protected] for any questions or corrections.