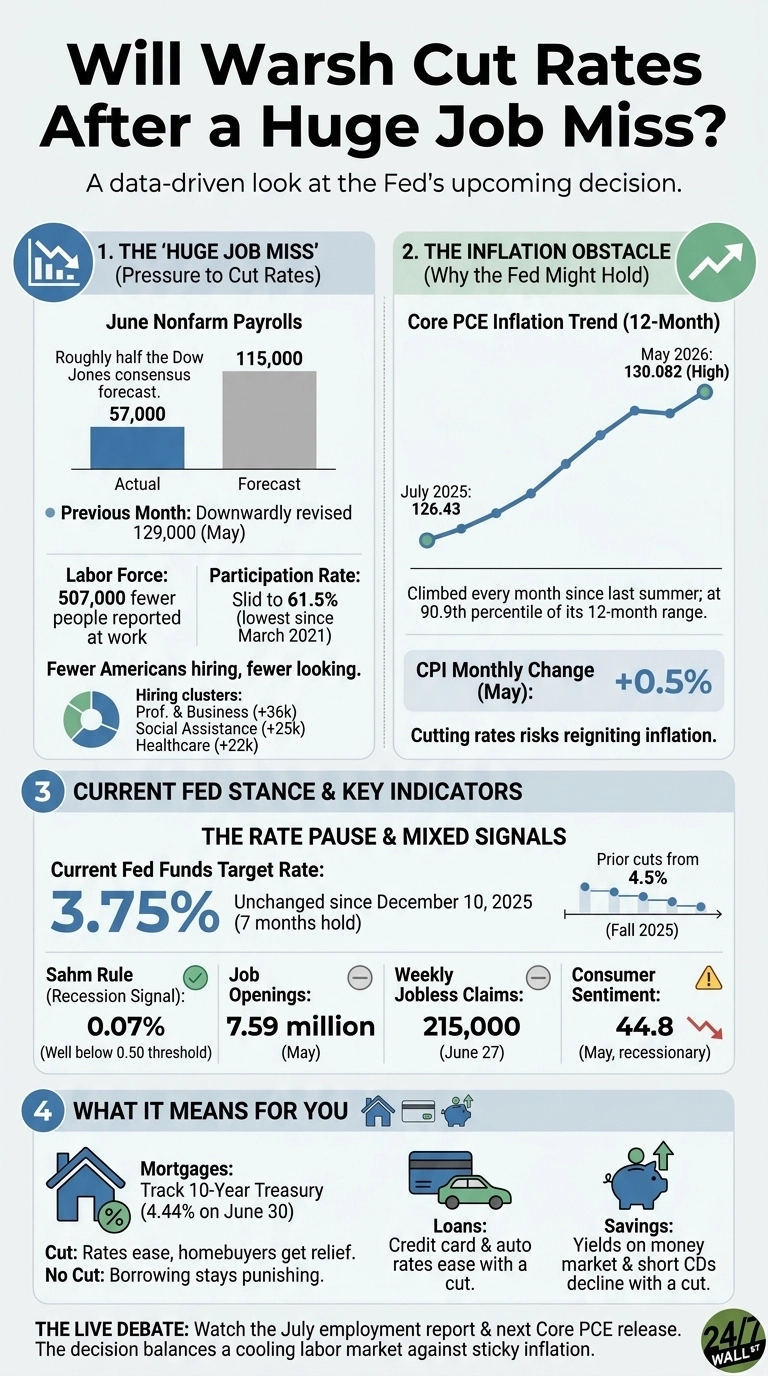

The June jobs report landed with a thud. American employers added just 57,000 nonfarm payrolls, roughly half the 115,000 Dow Jones consensus forecast and a sharp cooldown from the downwardly revised 129,000 added in May. The unemployment rate ticked down to 4.2%, but the mechanics behind that drop were ugly: 507,000 fewer people reported being at work in the household survey, and the labor force participation rate slid 0.3 percentage point to 61.5%, the lowest since March 2021. Fewer Americans hired. Fewer Americans looking. That is the report Chair Kevin Warsh’s Federal Reserve now has to interpret.

Good headline, bad guts

The falling unemployment rate would normally take pressure off the Fed to move. This time it does the opposite. Unemployment fell because people stopped searching, while payrolls stayed weak. Where hiring did happen, it clustered in a narrow band of service sectors: professional and business services added 36,000 jobs, social assistance 25,000, and healthcare 22,000. Manufacturing, construction, and retail were essentially absent from the tally. That is a labor market breathing through a straw.

The Sahm Rule, a widely watched recession trigger, still reads a benign 0.07 percentage points as of June 1, well under the 0.50 threshold. Job openings sit at 7.59 million and weekly jobless claims at 215,000, both consistent with a slowdown rather than a break. But consumer sentiment tells a darker story: the University of Michigan index fell to 44.8 in May from 49.8 in April, deep in recessionary territory.

The rate the country actually feels

The federal funds target sits at 3.75%, where it has been parked since December 10, 2025. That followed three quarter-point cuts last fall that brought the rate down from 4.5%. Seven months of hold. The question the June report forces open: does the Warsh Fed break the pause?

Here is why it is a live debate rather than a foregone conclusion. Core Personal Consumption Expenditures inflation, the Fed’s preferred gauge, sits at the 90.9th percentile of its 12-month range and has climbed every month since last summer. The Consumer Price Index rose 0.5% in May alone. Cutting into that inflation picture carries obvious risk. Not cutting into a hiring slowdown carries a different one.

What a cut — or no cut — means at the kitchen table

For regular Americans, the transmission is direct. Mortgage rates track the 10-year Treasury, which closed at 4.44% on June 30, still near the top of its 12-month range. A Fed cut would nudge the short end lower and, if credible, pull the long end with it. Homebuyers waiting for a 6-handle on a 30-year fixed would finally get relief. That’s industry jargon for mortgage rates moving into the 6% range (the “handle” is the percentage value).

Credit card and auto loan rates — which reprice quickly off the front end — would ease. Savers holding money market funds and short CDs would lose yield.

No cut means the opposite. Borrowing stays punishing, deposit yields stay generous, and a labor market that just printed 57,000 jobs has to absorb another quarter of restrictive policy. The signal to watch is the July employment report and the next Core PCE release. If payrolls print soft again while inflation cools even a tenth, the pause ends. If inflation stays sticky, Warsh keeps the rate exactly where it is, and the household survey’s missing 507,000 workers become someone else’s problem.

Contact [email protected] for any questions or corrections.