Tesla (NASDAQ:TSLA | TSLA Price Prediction) and BYD (OTC:BYDDF) sit at opposite poles of the electric vehicle world.

Tesla just posted a sharp Q1 margin rebound while pouring cash into robotics and autonomy. BYD, the world’s largest new energy vehicle maker by volume, keeps flooding global markets with affordable EVs and plug-in hybrids. The businesses barely resemble each other anymore, which is exactly why this quarter is worth comparing.

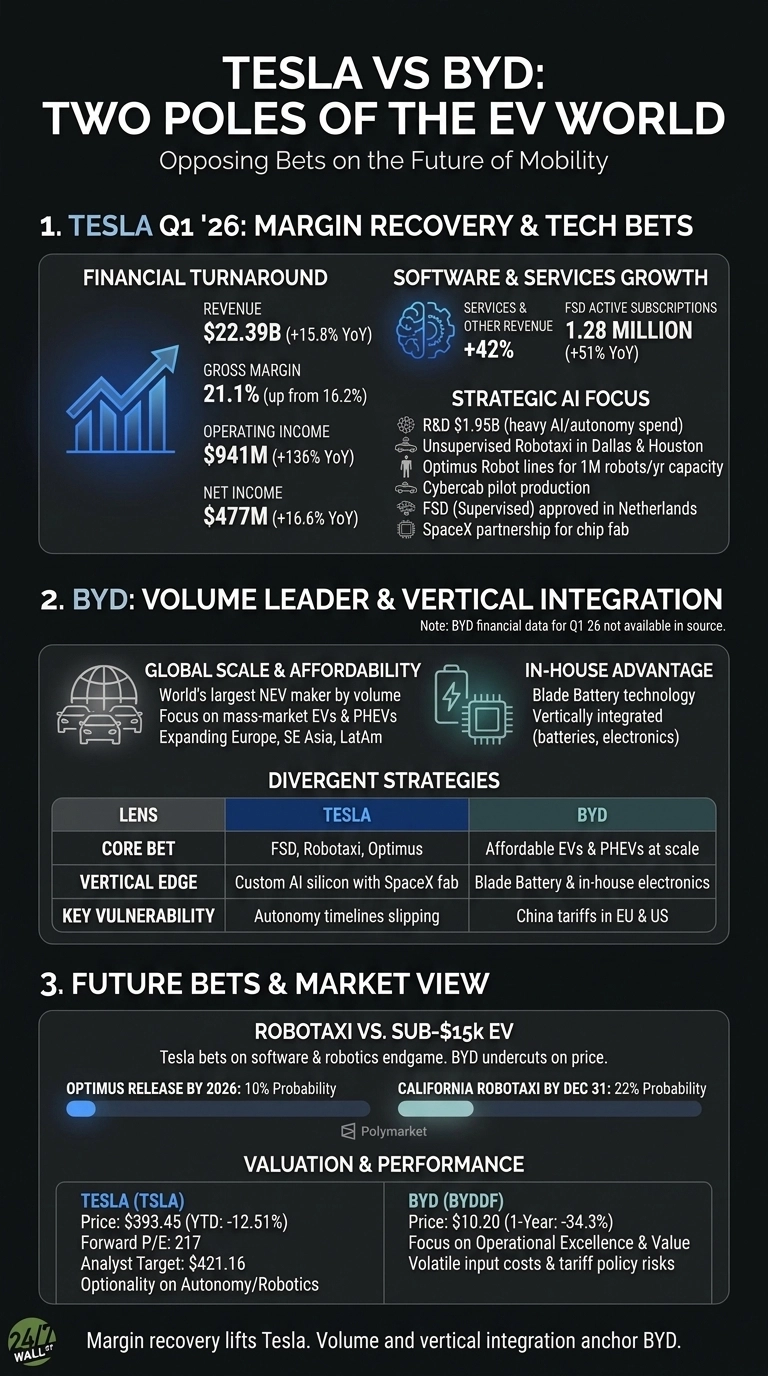

Margin Recovery Lifts Tesla. Volume and Vertical Integration Anchor BYD.

Tesla’s Q1 2026 print was a genuine turnaround quarter. Revenue hit $22.387 billion, up 15.78% year over year, and automotive gross margin snapped back to 21.1% from 16.2%. Operating income jumped 135.84% to $941 million. That is a real profitability inflection after a brutal 2025, when full year net income fell 46.79%.

The mix tells the story. Services and other revenue climbed 42% as FSD active subscriptions reached 1.28 million, up 51% year over year. Software is finally showing up in the P&L. Energy revenue slipped 12%, a rare soft spot after a record 2025.

BYD’s business runs on a different engine. It builds Blade Battery cells in-house, sells across the Dynasty, Ocean, Denza, Yangwang, and Fang Cheng Bao brands, and pushes hard into Europe, Southeast Asia, and Latin America. Chairman Wang Chuanfu has kept the company obsessively focused on cost per vehicle and battery supply, not autonomy software.

Robotaxi Bet vs. Sub-$15,000 EV Bet

| Lens | Tesla | BYD |

| Core bet | FSD, Robotaxi, Optimus | Affordable EVs and PHEVs at scale |

| Vertical edge | Custom AI silicon with SpaceX fab | Blade Battery and in-house electronics |

| Key vulnerability | Autonomy timelines slipping | China tariffs in EU and US |

Tesla’s $1.95 billion R&D quarter, unsupervised Robotaxi launches in Dallas and Houston, and Optimus lines designed for 1 million robots per year in Fremont point to a software and robotics endgame. Prediction markets are less convinced. Polymarket traders put only a 0.1 probability on an Optimus release by year-end and just 0.22 on a California Robotaxi launch by December 31.

BYD is taking a different path, undercutting legacy automakers on sticker price and betting anti-involution policy support flagged by Morningstar will consolidate share toward Chinese EV conglomerates such as BYD and Geely.

Deliveries, Tariffs, and Whether Software Revenue Compounds

I will be watching Tesla’s Q2 delivery cadence, the Cybercab pilot ramp at Gigafactory Texas, and whether FSD subscriber growth keeps compounding above 50%.

For BYD, tariff outcomes in Europe and export volumes into ASEAN and Brazil are the swing factors. You should also keep an eye on battery pack capacity, which Tesla flagged as its limiting factor on vehicle production.

Why I Lean Toward BYD on Value, Tesla on Optionality

Tesla trades at a forward P/E of 217 with a $421.16 analyst target against a current $393.45. The stock is down 12.51% year to date after a 7.49% single-day drop.

BYD shares sit at $10.20, off 34.3% over one year. If I want optionality on autonomy and robotics, Tesla is the vehicle, and I accept the multiple.

In case I want an operationally excellent, cash-generative automaker at a beaten-down price, BYD looks more interesting to me. If input costs and tariff policy stay volatile, I would rather wait than force either position.

Contact [email protected] for any questions or corrections.