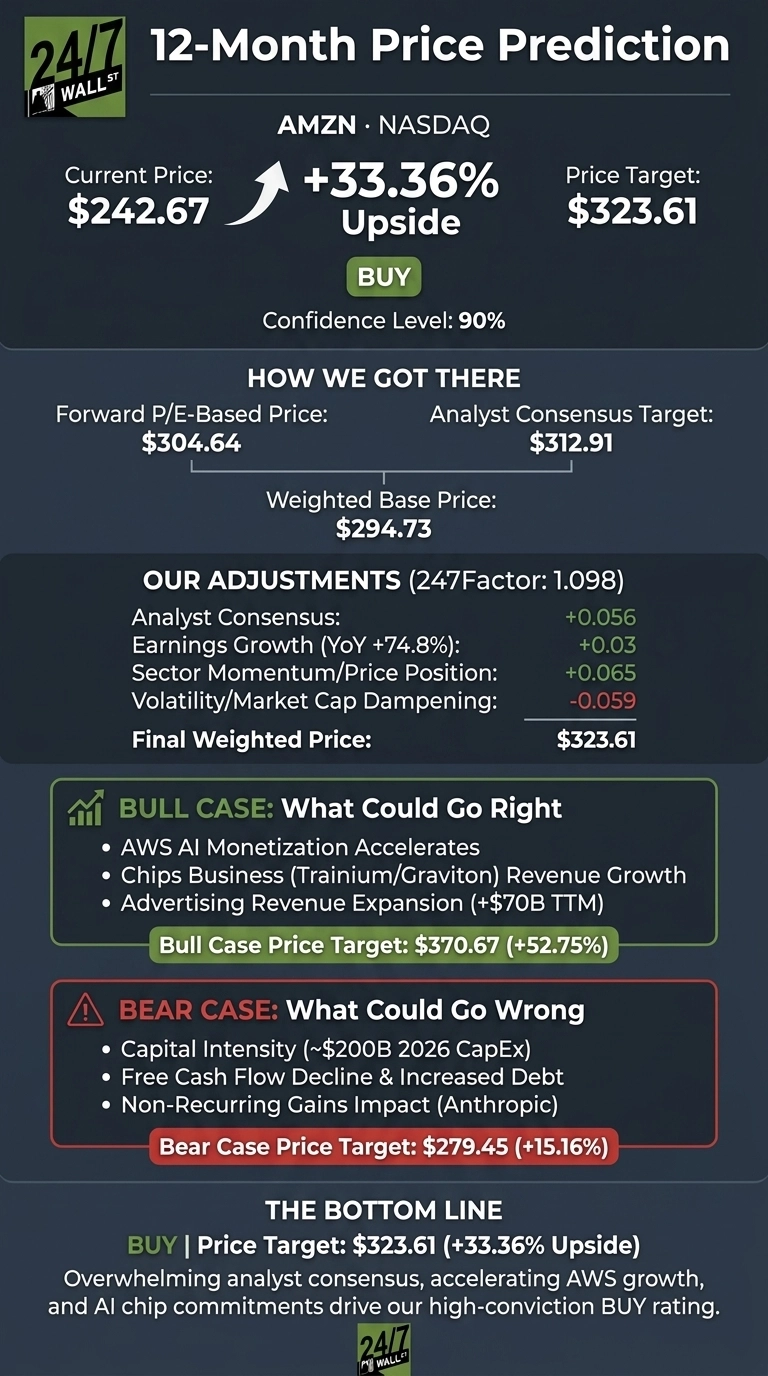

Amazon (NASDAQ:AMZN | AMZN Price Prediction) heads into the back half of 2026 with an overwhelming Wall Street consensus behind it. Our 24/7 Wall St. price target for Amazon is $323.61, implying 33.36% upside from the current price of $242.67. I rate Amazon a buy with a 90% confidence level, which qualifies as high conviction in our framework.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $242.67 |

| 24/7 Wall St. Price Target | $323.61 |

| Upside | 33.36% |

| Recommendation | BUY |

| Confidence Level | 90% |

Prime Day Momentum Meets a Post-Selloff Setup

Amazon shares rose 6.9% in the week ending July 2, even though the stock is still down 5.4% over the past month and sits roughly 12% below its 52-week high of $278.56. Year to date, AMZN is up 5.13%, with a ten-year return of 568.81%.

The Q1 2026 report set the tone. Amazon delivered EPS of $2.78 against a $1.73 estimate, a 60.69% beat, on revenue of $181.52 billion, up 16.6% year over year. AWS grew 28%, its fastest pace in 15 quarters, and now runs at a $150 billion annualized clip. Prime Day 2026 landed in June and is baked into Q2 guidance of $194B to $199B in net sales.

The Case for $370 and Beyond

Bulls have plenty to work with. Amazon’s chips business surpassed a $20 billion annual run rate with triple-digit growth, and Andy Jassy noted the company has “over $225 billion in revenue commitments for Trainium“. AWS backlog stood at $364 billion at quarter end, before a $100 billion Anthropic deal was added. Advertising crossed $70 billion in TTM revenue.

Of the 66 analysts covering AMZN, 15 rate it Strong Buy and 47 rate it Buy with zero sells. Our bull case scenario points to $370.67, a 52.75% return, if AWS AI monetization accelerates and Prime Day flows through to margin expansion.

What Could Go Wrong

The bear case centers on capital intensity. Amazon plans roughly $200 billion in 2026 capex, and TTM free cash flow already collapsed 95% to $1.2 billion. Long-term debt climbed to $119.1 billion from $65.6 billion, and Q1 net income was boosted by $16.80 billion in non-recurring Anthropic gains. Reddit thread activity around hyperscaler overinvestment underscores the sentiment risk.

Bulls would counter that Jassy has already flagged the payoff structure, saying “we have high confidence this will be monetized well, as we already have customer commitments for a substantial portion of it”. Still, if AI capex enthusiasm cools, our bear scenario projects $279.45.

I’d Buy This Pullback

My final call is buy with a 24/7 Wall St. price target of $323.61 and 90% confidence. The key factor tipping the scale is AWS re-acceleration paired with the chips business hitting escape velocity. I’d be a buyer here if AWS growth stays above 25% into Q3. I’d step aside if free cash flow keeps deteriorating without visible AI monetization by year-end.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $323.61 |

| 2027 | $385 |

| 2028 | $445 |

| 2029 | $500 |

| 2030 | $549.34 |

These projections assume AWS growth stabilizes in the 20% range and advertising continues expanding above 20%. Meaningful upside or downside could come from Trainium adoption curves and Amazon Leo’s commercial ramp.

Contact [email protected] for any questions or corrections.