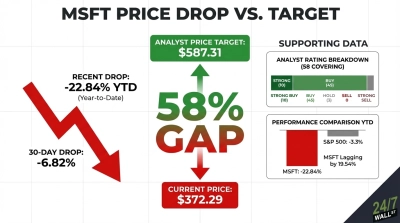

Microsoft (NASDAQ:MSFT | MSFT Price Prediction) has quietly built a $37 billion AI business, yet the stock has done the opposite of what you would expect. Shares of Microsoft closed at $390.49, down 18.9% YTD, while Azure grew 40% and commercial backlog nearly doubled to $627 billion.

Satya Nadella runs one of the most profitable software franchises ever assembled. So why is the stock below where it started the year? And can it climb to $500 by July 2027?

The Real Reason Microsoft Is Down 18.9% This Year

MSFT peaked near $520 in August 2025 and has not recovered. Shares are down 11.52% over the past month, 18.9% YTD, and 19.85% over one year. The drawdown exceeds what a beta of 1.13 would suggest.

Two forces weigh on the stock. Capital expenditure jumped 84% to $30.88 billion last quarter, with payback years away. Rising OpenAI investment losses hit $3.1 billion in Q1 FY26 versus $523 million a year earlier. Broader Magnificent 7 selling has erased trillions in mega-cap value, dragging multiples lower even as earnings accelerate.

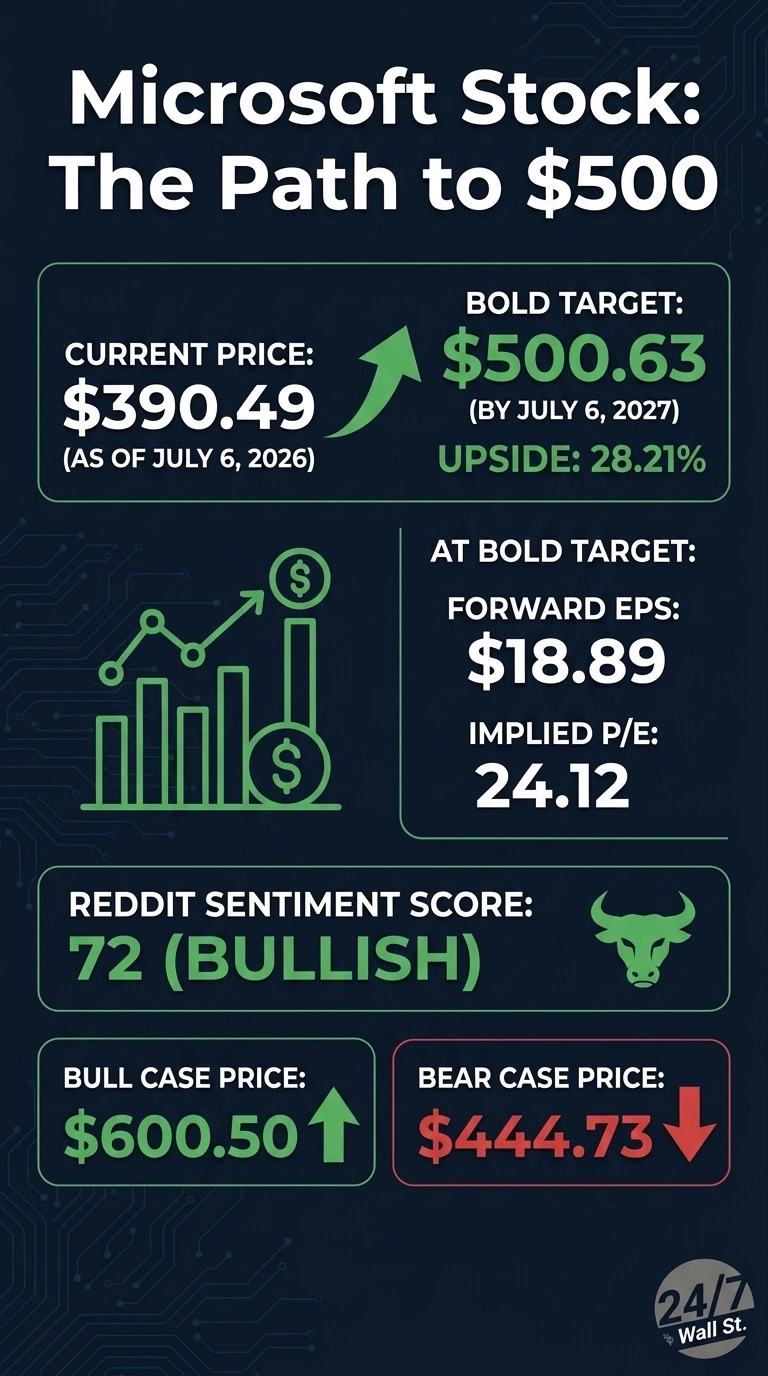

Wall Street Sees 44% Upside. Our Model Says 28%

Consensus analyst target sits at $561.11, implying roughly 44% upside. Of 56 analysts, 13 rate Strong Buy, 40 Buy, 3 Hold, and zero Sell. That is 95% bullish, zero bearish. Our model lands at $500.63 in twelve months, an upside of 28.21% with 90% confidence.

The optimistic case runs to $600.50 and the bear case sits at $444.73. Analysts anchor to peak-2025 multiples that may not snap back this year. Our lower call reflects the mega-cap dampener in the 247Factor and the reality that a $2.9 trillion company re-rates slowly. If earnings growth of 23.4% YoY holds, Wall Street eventually wins.

The Path to $500 Per Share

Reaching $500 from today’s price of $390.49 requires a gain of 28%. With forward EPS of $18.89, a price of $500 implies a forward P/E of 27x. Our base case of $500.63 already implies 24x, meaning the bold target requires 2.4x of additional multiple expansion.

Microsoft has topped EPS estimates four consecutive quarters. Earnings grew 23.4% YoY, and the AI business runs at a $37 billion annualized rate, up 123% YoY. Commercial RPO of $627 billion, up 99% YoY backstops the next several years of revenue. Nadella stated directly on the last call: “Our AI business surpassed an annual revenue run rate of $37 billion, up 123% year-over-year.”

If Azure holds near +40% and forward EPS drifts toward $20, the multiple resets. Main risk: capex intensity compressing margins if AI monetization lags.

Where Microsoft Trades Today vs Its Earnings Power

At $390.49 and forward EPS of $18.89, MSFT trades at 21x forward earnings. That is a discount to the trailing P/E of 23 and below where mega-cap software normally clears. Operating margin sits at 45.62% and ROE at 33.28%.

Shares are 11% off the 52-week low of $349.20 and 29% below the $551.05 high. The ten-year return of 763.3% shows what compounding at scale delivers. Shares trade at a discount to historical multiples for one of the highest-quality software franchises in the market.

Is $500 Realistic? Here’s My Take

Reaching $500 requires a gain of 28% from $390.49. Realistic, and arguably the base case.

Three things need to go right. Azure must hold near +40% growth. Forward EPS estimates need to drift toward $20. Mega-cap multiples need to firm as the AI capex cycle proves out. What derails it: a slowdown in enterprise AI adoption combined with capex-driven margin compression. We’ve outlined the blueprint for how Microsoft could reach $500 in 2027.

Contact [email protected] for any questions or corrections.