Synopsys (NASDAQ:SNPS | SNPS Price Prediction) has become one of the most important picks-and-shovels plays on the AI buildout, yet the stock has quietly slipped 16.43% over the past year.

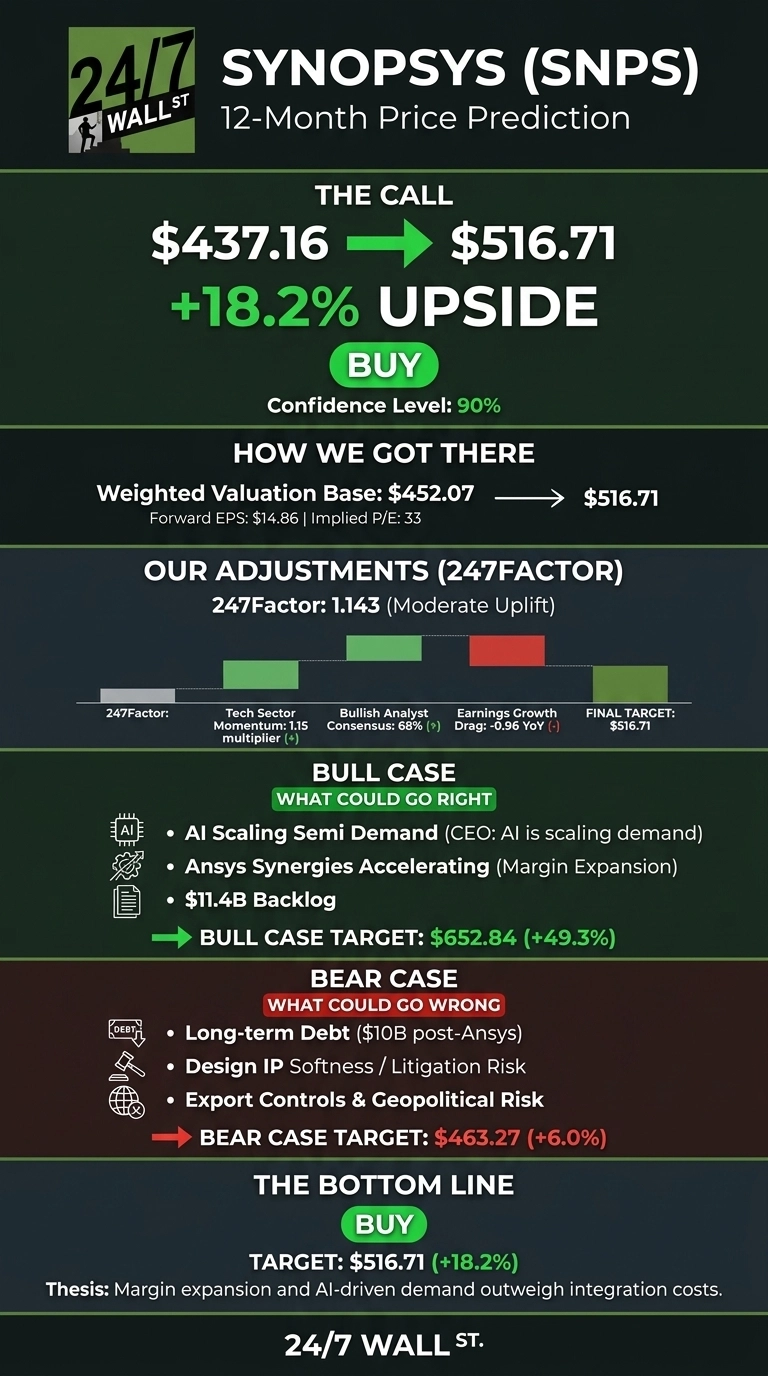

Our 24/7 Wall St. price target for Synopsys is $516.71, implying 18.2% upside from the current $437.16 level. Our recommendation is buy, at a 90% confidence level, one of the higher conviction readings in our large-cap software coverage.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $437.16 |

| 24/7 Wall St. Price Target | $516.71 |

| Upside | 18.2% |

| Recommendation | BUY |

| Confidence Level | 90% |

A Post-Ansys Reset That Masks the Underlying Business

Synopsys is down 14% over the past month and 6.93% year to date, sitting 14% below its 52-week high of $651.73.

Q2 FY2026, reported May 27, 2026, delivered revenue of $2.28 billion, up 41.98% year over year, and non-GAAP EPS of $3.35 against a $3.16 estimate. Management raised FY2026 revenue guidance to a midpoint of $9,665 million and non-GAAP EPS to $14.76.

The overhang is optical. GAAP net income fell 95.05% year over year, weighed down by $403.6 million in quarterly amortization of acquired intangibles from the $35 billion Ansys deal that closed in July 2025. Piper Sandler upgraded to Overweight on June 28, lifting its target to $550, and Elliott Investment Management pushed a board seat for Jesse Cohn to accelerate synergy realization.

The Case for $650 and Higher

The bull scenario runs to $652.84, a 49.34% return. It rests on three pillars. First, AI is a genuine tailwind for EDA. CEO Sassine Ghazi described it plainly: “AI is scaling semiconductor demand, architectural diversity and complexity of chips and the systems they power.”

Second, Design Automation adjusted operating margin expanded to 43.3% from 40.9%, and Ansys synergies are still ramping.

Third, the backlog stands at $11.4 billion. The Street consensus target of $563.74 sits comfortably between our base and bull cases.

The Risks Worth Watching

Our bear case targets $463.27. Long-term debt sits near $10 billion post-Ansys, though Synopsys has already repaid $3.46 billion in the first half of FY2026. Design IP softened to $454.2 million, and a securities class action alleges the segment’s economics were misrepresented.

Bulls would counter that the planned Processor IP Solutions divestiture is a deliberate reallocation to higher-growth areas, and that 91% institutional ownership plus a Piper Sandler upgrade suggest smart money views the Design IP concern as contained.

Synopsys Price Prediction 2026-2030

My verdict is a buy with a 24/7 Wall St. price target of $516.71 at 90% confidence. The factor that tips the scale is margin expansion in Design Automation against a backdrop of accelerating AI chip design workloads.

The bullish case strengthens if Ansys synergies land on schedule and export controls remain manageable. The setup weakens if the securities litigation escalates or if Design IP weakness spreads into the core EDA franchise.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $469.92 |

| 2027 | $516.71 |

| 2028 | $591.79 |

| 2029 | $663.17 |

| 2030 | $736.97 |

These projections assume Synopsys continues to execute on its silicon-to-systems roadmap and Ansys synergies compound. Significant upside or downside could come from a step-change in AI chip design intensity or a material regulatory action tied to export controls.

Contact [email protected] for any questions or corrections.