I keep hitting the buy button on Apple (NASDAQ:AAPL | AAPL Price Prediction), and going into the back half of 2026 this is the largest position I own. I want to explain, in plain terms, why my money keeps landing here quarter after quarter.

What pulls me back is simple. Apple pairs a subscription-like Services engine with a hardware franchise that just posted its best March quarter ever, wrapped inside a capital return program built to compound in the background whether or not the stock cooperates in any given month.

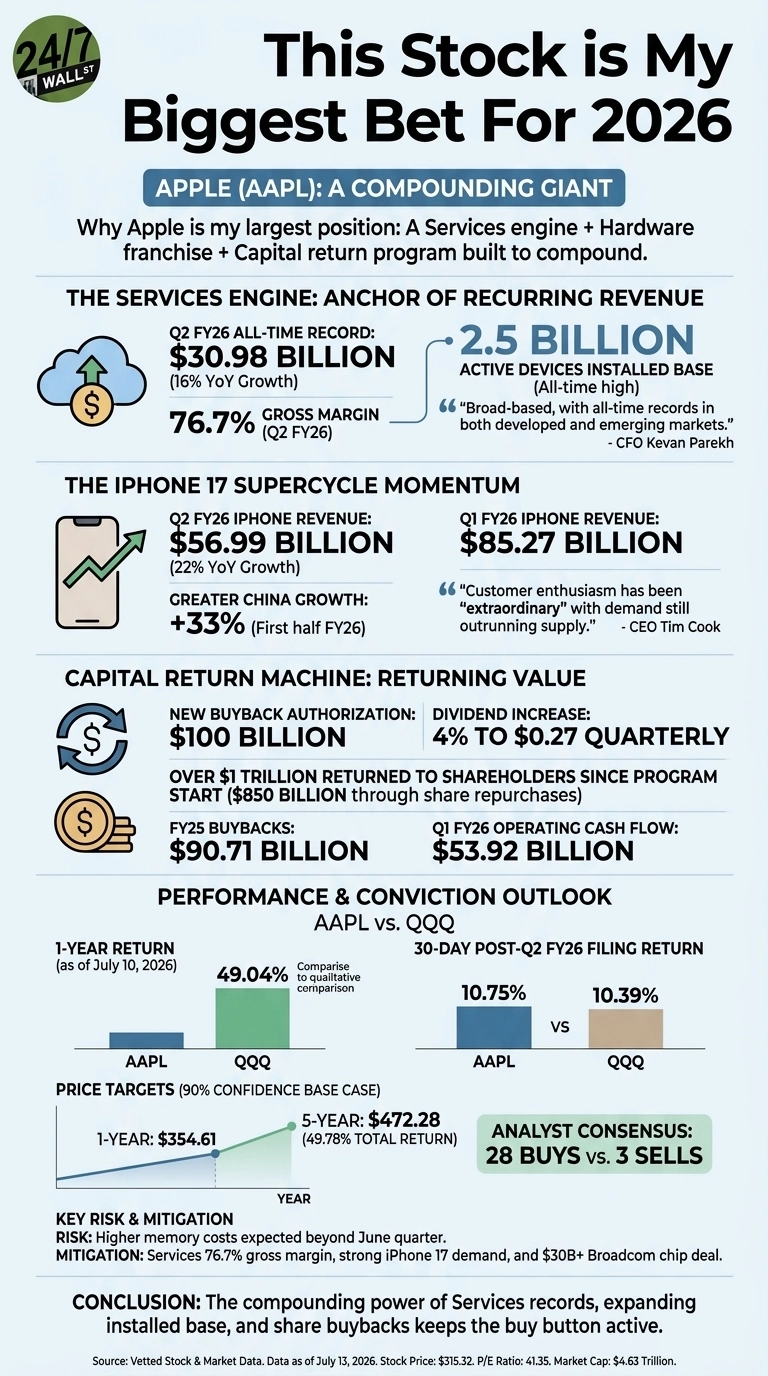

The Services Engine Is the Anchor

In Q2 FY26 the segment hit an all-time record of $30.98 billion at a 76.7% gross margin, growing 16% year over year. That is a software business hiding inside a hardware company, riding 2.5 billion active devices. CFO Kevan Parekh described the growth as “broad-based, with all-time records in both developed and emerging markets.” Recurring, high-margin, sticky.

The iPhone 17 Cycle Is Real

iPhone revenue climbed 22% to $56.99 billion in Q2 FY26. Q1 FY26 iPhone revenue reached $85.27 billion versus $69.14 billion a year earlier. Greater China rose 33% in the first half of FY26, and Tim Cook said customer enthusiasm has been “extraordinary” with demand still outrunning supply. This franchise is accelerating.

The Capital Return Machine

The board authorized a fresh $100 billion buyback, raised the dividend 4% to $0.27 quarterly, and Parekh noted Apple has returned over $1 trillion to shareholders since the program began, “$850 billion of which has been through share repurchases.” FY25 buybacks alone were $90.71 billion, and operating cash flow was $53.92 billion in Q1 FY26 alone.

Why Apple and Not the ETF

The obvious alternative a mega-cap tech buyer would reach for is Invesco QQQ Trust (NASDAQ:QQQ). I own it too. But over the last 12 months AAPL returned 49.04%, and in the 30 days after the Q2 FY26 filing AAPL rose 10.75% versus 10.39% for QQQ. When I want concentrated exposure to the ecosystem generating $53.92 billion of quarterly operating cash flow, I would rather own the single company than dilute it across 99 other tickers.

The Real Risk

Memory costs. Cook told analysts Apple expects higher memory costs in the June quarter and that beyond June, “memory costs will drive an increasing impact on our business.” That is real gross margin pressure.

The thesis still holds because Services carries a 76.7% gross margin, iPhone 17 demand still outruns supply, and Apple just signed a chip agreement with Broadcom (NASDAQ:AVGO) worth more than $30 billion, adding another supply lever alongside pricing and mix flexibility.

Where Conviction Points Next

Retail sentiment stays measured here, which is one reason I keep buying. Reddit sentiment sits at 44 to 56 through the OpenAI lawsuit news cycle. The stock trades at a P/E of 41. The 90% confidence base case projects $354.61 within a year and $472.28 over five years, a 49.78% total return. Analyst counts show 28 buys to 3 sells.

I own Apple for the compounding. As long as Services keeps printing records, the 2.5 billion device installed base keeps expanding, and the buyback keeps shrinking the share count, my finger stays on the buy button.

Contact [email protected] for any questions or corrections.