I keep hitting the buy button on Apple (NASDAQ:AAPL | AAPL Price Prediction), and I stopped apologizing for it a long time ago. Every time a fresh paycheck lands, or a dividend clears, or the stock takes a breather, I add. This is the position in my brokerage account that I plan to hand down for the long term.

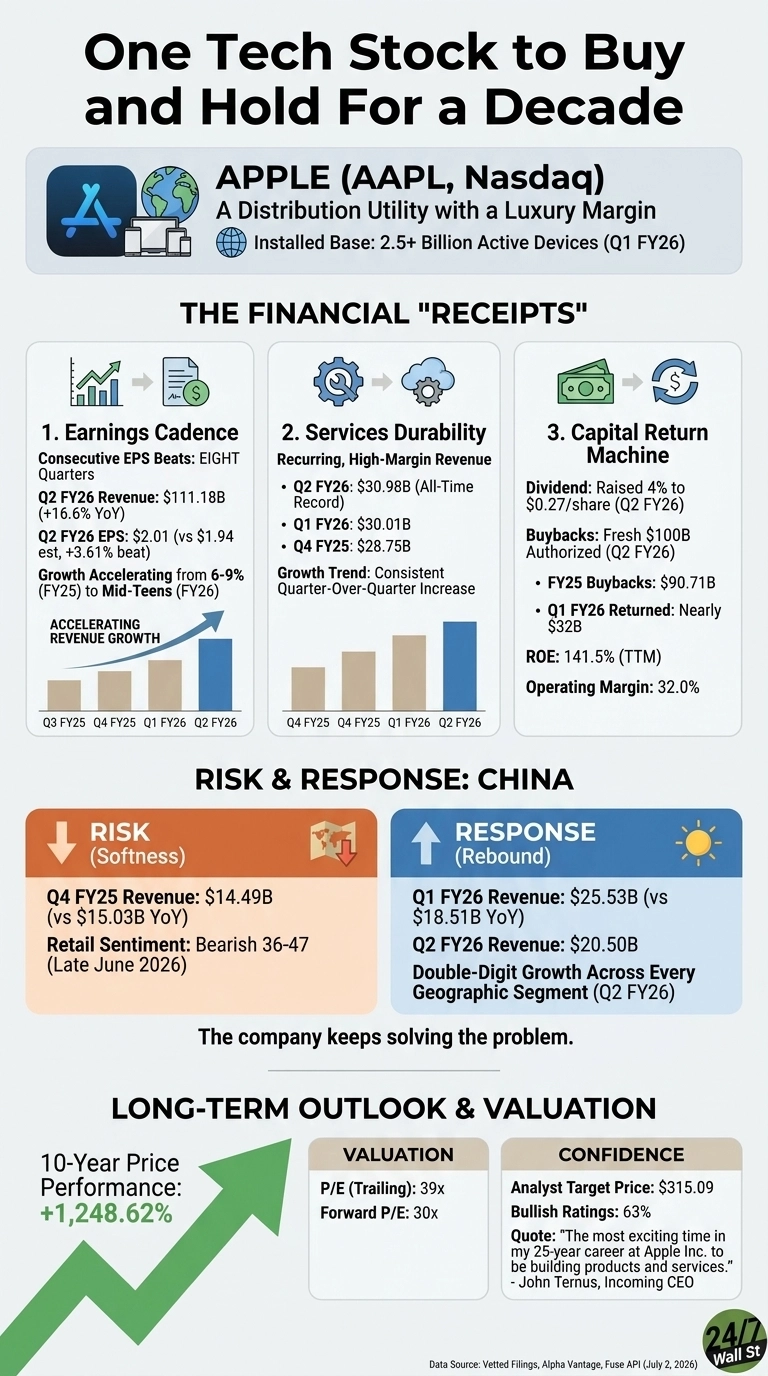

The pull is simple. Apple sits inside 2.5+ billion active devices that people voluntarily carry, wear, and open every day. That is a distribution utility with a luxury margin bolted on top. When a company owns the front door to that many pockets, revenue becomes a rhythm.

The three receipts I keep coming back to

First, the earnings cadence. Apple has now beaten EPS estimates for eight consecutive quarters. In the most recent March quarter, revenue came in at $111.18B, up 16.6% YoY, with EPS of $2.01 versus a $1.94 estimate.

The quarter before that put up $143.76B in revenue, up 15.7%, with operating cash flow of $53.93B, up 80.1% YoY. Growth is accelerating from the 6% to 9% band of Q3 to Q4 FY25 into the mid-teens. That is the shape of a company hitting a new gear.

Second, Services. This is the piece I care about most as a holder. Services printed $30.98B in Q2 FY26, an all-time record, on top of $30.01B the prior quarter. Recurring, high-margin, sticky revenue attached to that installed base is what turns Apple from a hardware cycle stock into a compounding platform.

Tim Cook framed the quarter as “our best March quarter ever, with revenue of $111.2 billion and double-digit growth across every geographic segment.”

Third, the capital return machine. The board just raised the dividend 4% to $0.27 per share and authorized a fresh $100B buyback. In Q1 FY26 alone, Apple returned nearly $32B to shareholders, and full-year FY2025 buybacks totaled $90.71B.

Profitability sits at 32% operating margin and 26.9% net margin, with an ROE of 141.5%. Every share I own becomes a larger slice of a widening pie, quarter after quarter.

The risk I refuse to wave off

China. Apple discloses reliance on third-party components and manufacturing, trade disputes, and geopolitical tensions as real risks, and Greater China softened in Q4 FY25 to $14.49B from $15.03B. Retail chatter picked up on this too, with a Reddit post about Apple seeking memory chips from a blacklisted Chinese company pushing sentiment into the bearish 36 to 47 range in late June.

I hold that risk in view every time I add. What has not changed is the response. Greater China rebounded to $25.53B in Q1 FY26 (up from $18.51B) and $20.50B in Q2 FY26. The company keeps solving the problem I am worried about.

Why the buy button stays green

Valuation is not cheap at a P/E of 39x and a forward P/E of 30x. I pay it willingly.

Analyst consensus sits at a $315.09 target with 63% bullish ratings, and the stock has delivered 1,248.62% over ten years. Incoming CEO John Ternus told the Street this is “the most exciting time in my 25-year career at Apple Inc. to be building products and services.”

I believe him, because the receipts back him up. As long as the installed base grows and Services keeps compounding, I keep buying, and the next decade takes care of itself.

Contact [email protected] for any questions or corrections.