Oracle (NYSE: ORCL | ORCL Price Prediction) has been the AI cloud story of the year, then the AI cloud panic of the last month. Shares are down 35.29% year to date and 33.43% over the past month, yet the underlying business is growing faster than at any point in Oracle’s history.

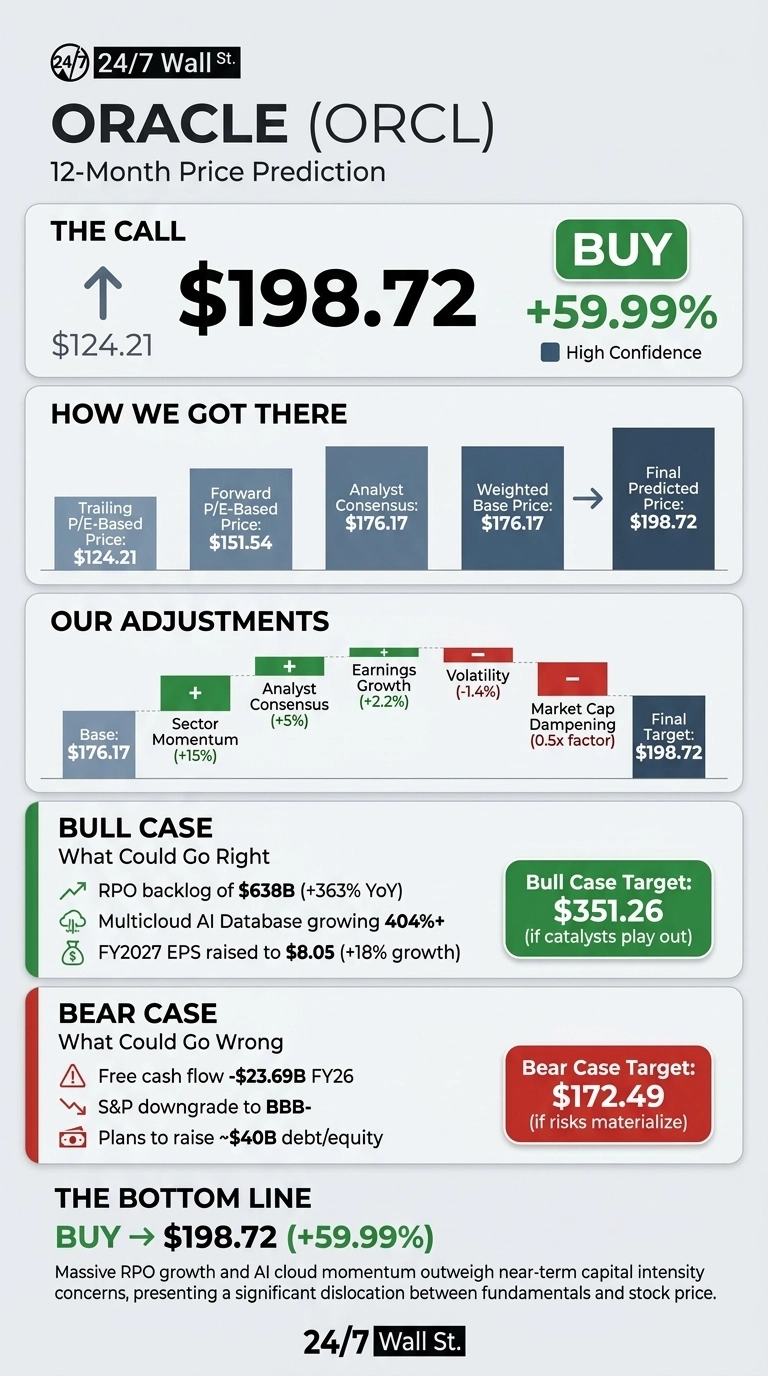

Our 24/7 Wall St. price target for Oracle is $198.72 over the next 12 months, implying 59.99% upside from current levels. Our recommendation is buy with high confidence.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $124.21 |

| 24/7 Wall St. Price Target | $198.72 |

| Upside | 59.99% |

| Recommendation | BUY |

| Confidence Level | 90% |

Why Oracle Just Cratered

Oracle sits 26% below its 52-week high of $341.82 and just above the 52-week low of $123.66.

Recent catalysts include S&P Global downgrading Oracle from BBB to BBB- on July 13 tied to AI infrastructure debt, New Mexico rejecting a gas pipeline permit for an Oracle data center, and sector contagion after IBM (NYSE:IBM) shares dropped more than 25% on a Q2 miss.

Yet Q4 FY2026 delivered EPS of $2.11 on revenue of $19.18 billion, with IaaS growing 93% year over year to $5.79 billion and remaining performance obligations exploding 363% to $638 billion. The fundamentals and the tape have completely decoupled.

The Case for $250+

The bull thesis rests on two engines that both accelerated last quarter. First, multi-cloud database revenue grew 531% year over year, with Oracle now live in 33 Microsoft regions, 14 Google regions, and exiting Q4 with 22 AWS regions.

Second, $75 billion of the $638 billion RPO is tied to customer-supplied GPUs, dramatically shrinking Oracle’s capex burden.

Management guides FY2027 revenue of $90 billion with non-GAAP EPS raised to $8.05, and Safra Catz’s five-year OCI roadmap climbs from $18 billion to $144 billion. Our bull case implies $351.26 within 12 months, roughly matching the Street’s $251.85 consensus.

What Could Go Wrong

The bear case starts with the balance sheet. Free cash flow was negative $23.69 billion for FY2026 against capex of $55.66 billion, and Oracle plans to raise roughly $40 billion in debt and equity in FY2027, including a $20 billion at-the-market equity program.

S&P’s downgrade to BBB- leaves Oracle one notch above junk. Bulls counter that greater than 90% of AI capacity is fully funded through partners and negative cash flow reflects heavy investment in capacity buildout. If AI demand cools, the bear case sits at $172.49.

How Oracle Compares to Microsoft and Salesforce

Microsoft (NASDAQ: MSFT) is the direct hyperscaler comp. Microsoft trades at a trailing P/E of 29 with Azure growing 40% and commercial RPO of $627 billion. Oracle’s trailing P/E of 23 and $638 billion RPO now match or exceed Microsoft’s backlog at a discount, making our target look conservative.

Salesforce (NYSE: CRM) is the applications-side comparison. Salesforce trades at a P/E of 19 after its own drawdown, growing revenue 13.3% in Q1 FY27. Oracle’s Fusion suite grew 11% on a much larger cloud infrastructure base, suggesting the sum-of-parts case is stronger for ORCL.

| Company | Forward P/E | Recent Cloud Growth |

|---|---|---|

| Oracle | 16 | IaaS +93% |

| Microsoft | 29 | Azure +40% |

| Salesforce | 19 | Agentforce ARR +205% |

The Setup After the Selloff

Our 24/7 Wall St. price target of $198.72 implies 59.99% upside with 90% confidence. RPO grew 363% while the stock lost a third of its value. That dislocation rarely lasts.

The bullish setup depends on the FY2027 $90 billion revenue target holding through the first two earnings reports. The key risk to watch is whether equity issuance dilutes shareholders faster than RPO converts to recognized revenue.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $141 |

| 2027 | $198.72 |

| 2028 | $257 |

| 2029 | $332 |

| 2030 | $429 |

These projections assume Oracle converts its RPO backlog on schedule and OCI compounds toward management’s $144 billion five-year target. Significant upside or downside could result from AI capex discipline, GPU sourcing, or the pace of Oracle Health rollout.

Contact [email protected] for any questions or corrections.