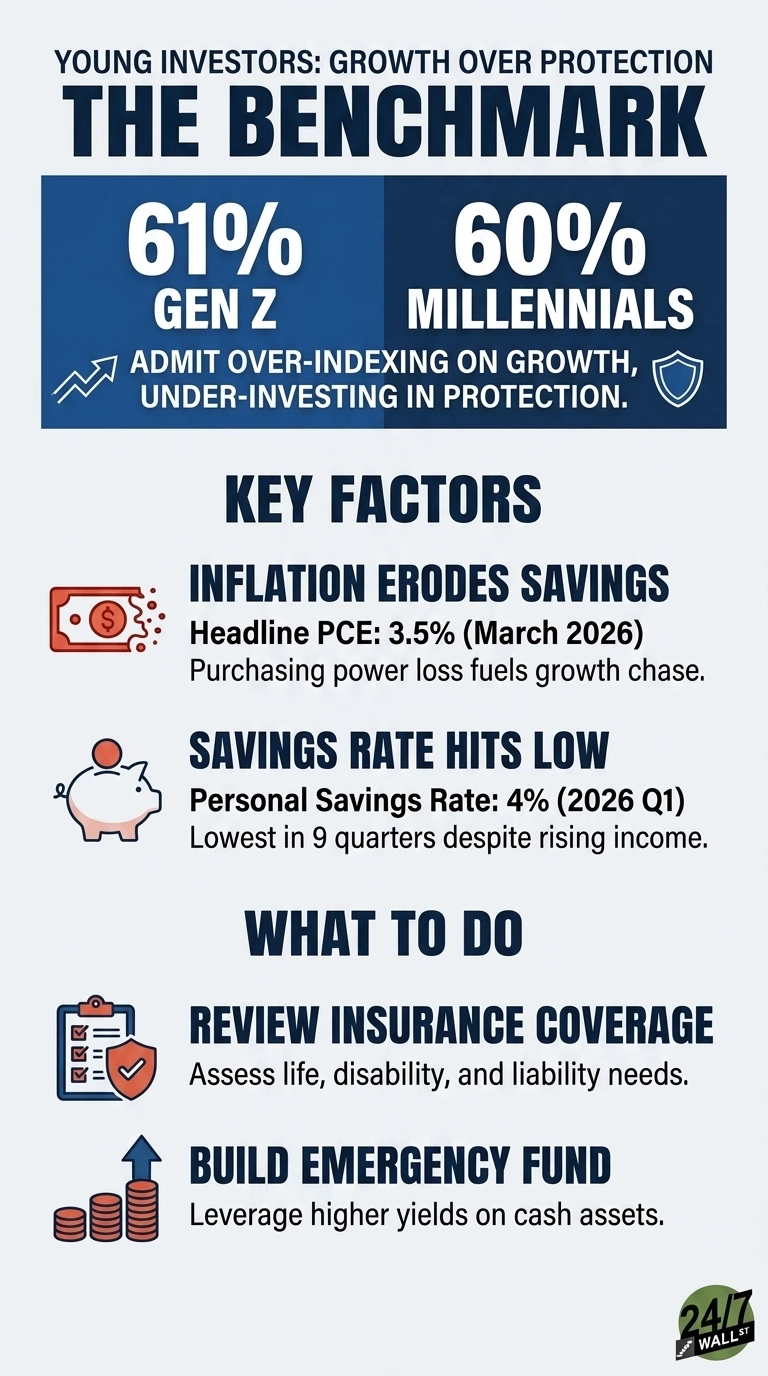

Most of the coverage around the latest Northwestern Mutual Planning & Progress Study centered on retirement readiness and the anxiety that comes with longer life expectancies. The more telling detail sat deeper in the report. Sixty‑one percent of Gen Z and 60% of Millennials say they are leaning too heavily on growth and not putting enough into protection. That is a majority of two generations acknowledging that their financial plans tilt toward building wealth rather than defending it. The surrounding data helps explain how that imbalance took shape.

What younger savers are actually doing

Protection, in this context, means term and permanent life insurance, disability coverage, an emergency fund deep enough to absorb a job loss, and estate basics. Growth means the brokerage account, the 401(k) allocation tilted toward equities, the crypto wallet, and the side bets. For a 28-year-old watching headlines about AI and housing prices, growth feels productive, while protection feels like a drag on returns.

The macro backdrop reinforces that instinct, with headline PCE inflation running at 3.5% year over year in March 2026 and core PCE at 3.2%. Core PCE sits at the 90.9th percentile relative to its historical distribution. A dollar parked in a checking account in early 2024 has lost roughly 6.6% of purchasing power by March 2026. For anyone who internalized that math, conservative savings can feel like guaranteed loss, and growth assets can feel like the only rational response.

What the savings rate shows

The Bureau of Economic Analysis data shows the squeeze in real time. The personal savings rate has fallen from 6.2% in the first quarter of 2024 to 4% in the first quarter of 2026, the lowest reading in the 9-quarter window. All the while, disposable personal income per capita rose to $68,617, and average hourly earnings climbed to $37.41 in April 2026 from $36.12 a year earlier. The simple truth is that income rose while the amount actually getting saved fell, with total personal savings dropping from $1.33 trillion to $942.3 billion.

That is the financial profile of households spending more on day‑to‑day living and lifestyle while keeping the protection layer thin, a pattern that lines up with the broader mood. The University of Michigan index registered 48.2 in March 2026, placing it in the 27.3rd percentile of its historical range and firmly in recessionary territory. When sentiment is that low, two behaviors often show up together: trimming discretionary insurance premiums and leaning harder into growth within the accounts people already have.

Where the dollars are actually going

Spending patterns make the picture even clearer, and financial services, which cover insurance and advisory costs, have inched up from 7.9% of total personal consumption in January 2025 to 8.3% in March 2026. People aren’t walking away from protection altogether. The category is growing, just slowly, while housing at 25.9% of services spending and healthcare at 24.8% continue to dominate the household budget. Recreation holds a modest 5.7%, but the real squeeze on protection comes from how little room is left once those fixed costs are covered, not from any broad reluctance to buy it.

Why the Northwestern Mutual finding lands harder for younger generations

The 2025 Planning & Progress Study notes that many non-retirees cannot quantify their savings as a multiple of current income, and a significant share worry about outliving their money. Younger respondents also envision a retirement that looks different from their parents’: longer working lives, more travel, more active years. That model implies a longer protection runway. A 35-year-old planning to work until 70 has 35 years of income to ensure, a longer period of disability exposure, and a longer window for a single bad event to derail compounding.

The 10-year Treasury yield at 4.47% changes part of the calculation, too. Cash and short-duration bonds now pay a real return, which lowers the opportunity cost of holding an emergency fund. The historical argument that protection assets earn nothing is weaker than it was three years ago.

What the data does and does not say

The Northwestern Mutual finding captures a self‑reported imbalance. It doesn’t claim that every young saver is underinsured, and it doesn’t argue that leaning toward growth is the wrong instinct in a 3.5% inflation environment. What it does show, when set alongside a 4% savings rate and a 53.3 sentiment reading, is that the protection side of the household balance sheet is getting less attention than the growth side at a time when unemployment, at 4.3%, is steady but hardly untouchable. For households that see themselves in the 61% and 60% figures, the real question is whether a single layoff, illness, or accident would undo years of progress

Contact [email protected] for any questions or corrections.