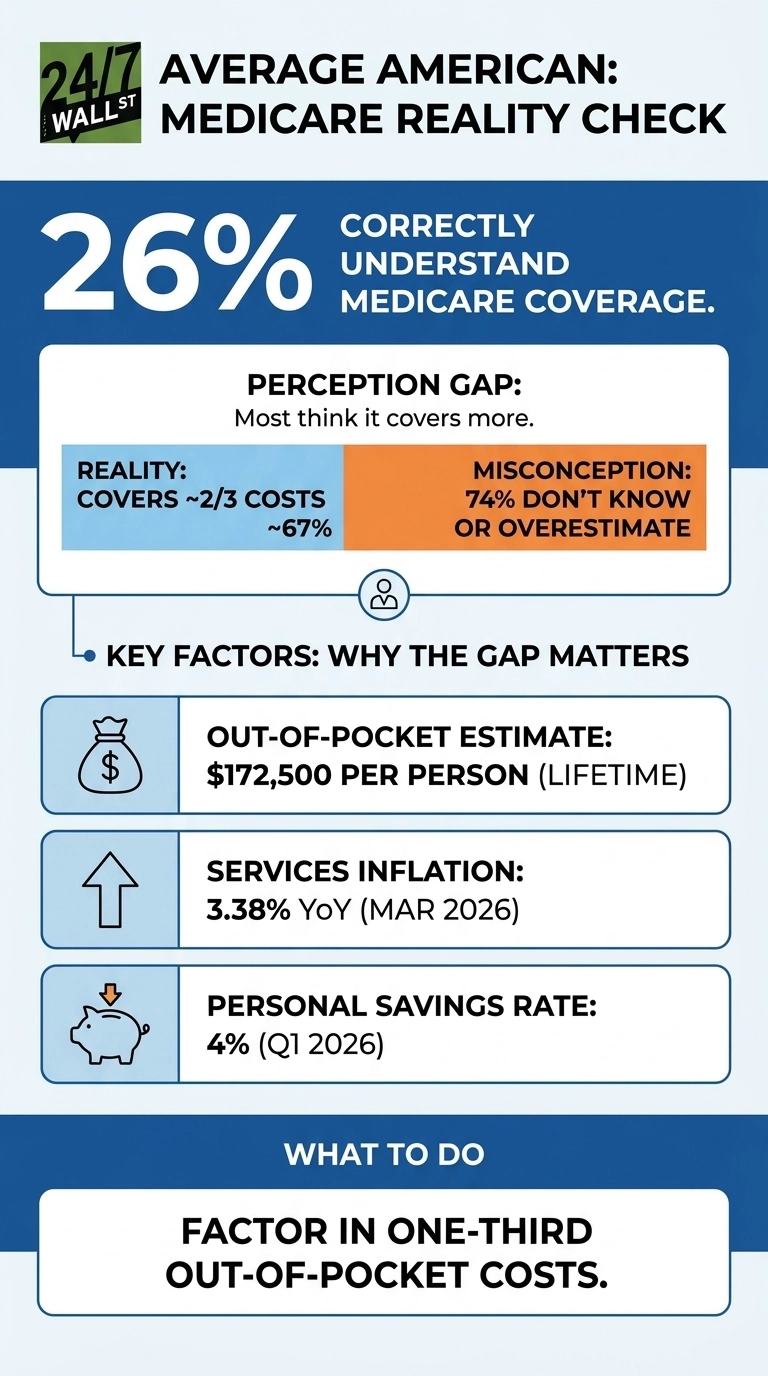

The TIAA Institute’s 2025 P-Fin Index put a deceptively simple question to U.S. adults: how much of a typical retiree’s healthcare expenses does Medicare actually cover? The big takeaway is that only 26% of respondents picked the right answer, and that is cause for concern.

The correct response, according to TIAA’s research summary of the survey, is that Medicare covers roughly two-thirds of retiree healthcare costs, leaving the rest to premiums, copays, deductibles, prescriptions, dental, vision, hearing, and long-term care. The other 74% of respondents either overestimated the program’s reach or admitted they did not know. That gap between perception and reality is a material planning risk for millions of household budgets right now.

What the misconception actually costs

The financial size of the remaining one-third is the part most pre-retirees miss. Fidelity’s 24th annual retiree health care estimate, published in 2025, projects that a 65-year-old retiring today could spend roughly $172,500 on health care over the course of retirement, and that figure is per person, not per couple. It also excludes long-term care, which Medicare does not pay for in any extended form. A household that walked into retirement assuming Medicare would handle 90% or more of the bill is, in practical terms, off by tens of thousands of dollars per person.

The macro data highlights exactly why the knowledge gap is becoming a chasm. Healthcare has surged to become the second-largest services spending category in the U.S. economy, trailing only housing at $3,741.3 billion as of March 2026. This massive footprint accounts for roughly 24.8% of all services spending. Meanwhile, Medicare transfer receipts to households jumped from $1,172.6 billion in Q1 2025 to $1,301 billion in Q1 2026. While the program is pumping out more cash, the share it covers per beneficiary remains static. For the 74% of Americans who don’t understand Medicare’s actual coverage limits, these rising costs are an unmitigated disaster in the making.

Why the gap is getting harder to absorb

Services inflation, the category where healthcare sits, remains stubbornly higher than goods inflation. The PCE services index rose 3.38% year over year in March 2026 and has maintained a 24-month run between 3.30% and 4.34%. Headline CPI tells a similar story, climbing from 313.548 in April 2024 to 333.020 in April 2026. Out-of-pocket healthcare costs do not sit still, even if a retiree’s income does.

Household balance sheets are heading in the wrong direction at the same time. The personal savings rate fell from 5.2% in Q1 2025 to 4% in Q1 2026, even as per capita disposable income rose to $68,617. Higher income, a lower savings rate, and persistent service inflation are a toxic combination. Since only 26% of adults understand what Medicare actually covers, that knowledge gap turns rising costs into a cash flow crisis during the first decade of retirement.

The literacy picture behind the number

The Medicare question did not fail in isolation. The same TIAA study found that U.S. adults correctly answered about 37% of retirement fluency questions on average, and only 7% got five or six of the six questions right. Retirement readiness tracks closely with that score: workers who answered zero questions correctly saved at a 48% rate, versus 85% among those who answered five or six questions correctly. The Medicare blind spot is one symptom of a broader fluency problem that the survey also documented as being more pronounced among women, Black Americans, and Hispanic Americans, even after controlling for income and education.

Consumer mood is not helping either, as the University of Michigan Consumer Sentiment Index shows, with a score of 48.2 in May 2026, down from 61.7 in July 2025, and historically at the 27th percentile. Ultimately, the learning is that households are making healthcare decisions while already anxious about everything else.

The takeaway

The data lines up cleanly, as one in four Americans understands what Medicare actually covers. The other three quarters face a roughly one-third out-of-pocket share, which Fidelity estimates at $172,500 per person over retirement, on top of a services inflation rate above 3% and a savings rate of 4%. The Medicare misconception is the single planning input that determines whether a retirement budget can absorb the first major hospital bill.

Contact [email protected] for any questions or corrections.