The Aggregate Hides Who Is Falling Furthest Behind

The national average masks wide differences across groups. Women answered 45% of the P‑Fin Index questions correctly, while men reached 53%. Racial and ethnic gaps were just as pronounced, with black respondents averaging 38% correct and Hispanic respondents 39%, compared with 53% for White adults and 55% for Asian adults. The study makes clear that these gaps are not simply artifacts of income or education. It notes that the disparities remain even after adjusting for sociodemographic factors, stating that “financial literacy remains lower among Blacks and Hispanics relative to Whites after controlling for various socioeconomic factors such as age, education, and income”.

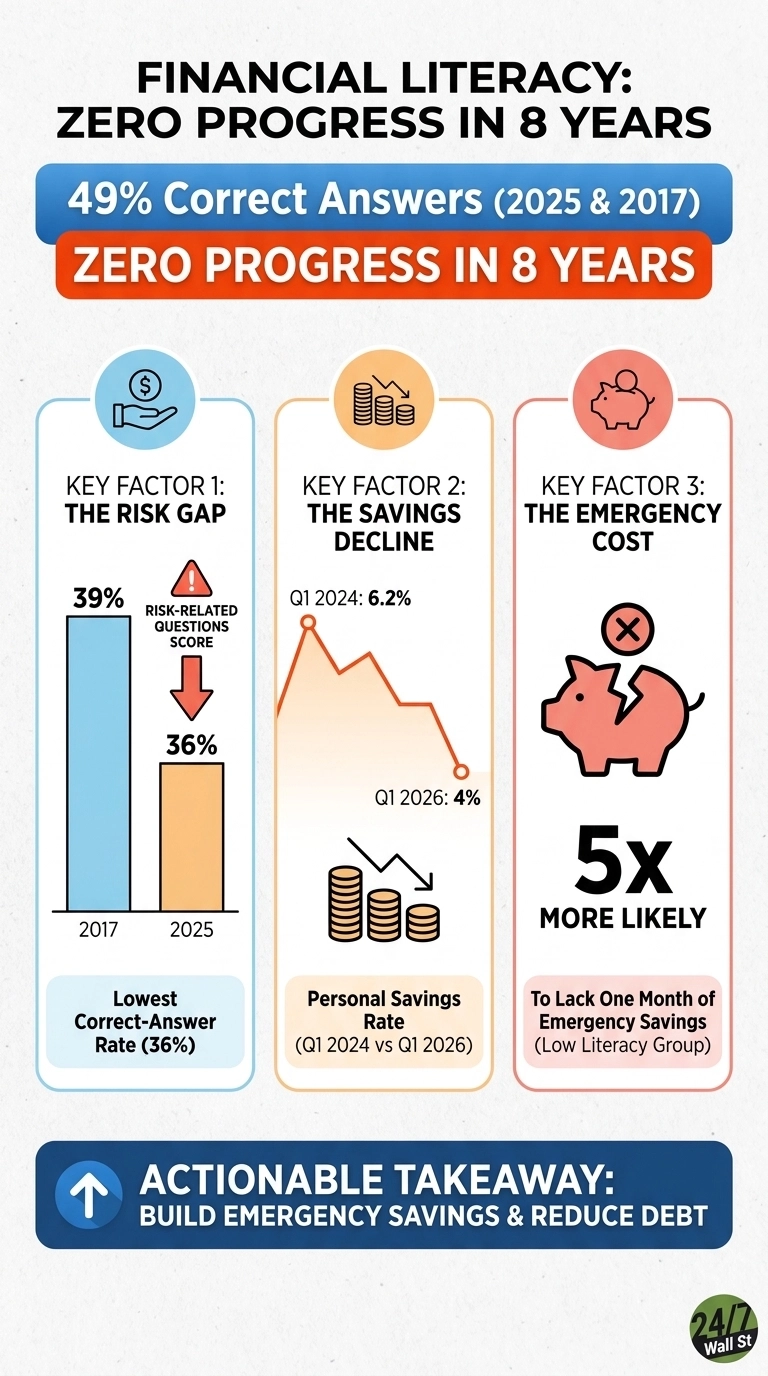

Risk Is the Weakest Domain, and It Got Weaker

Of the eight functional areas the P-Fin Index measures, risk-related questions had the lowest correct-answer rate in 2025 at 36%, down from 39% in 2017. Insurance, investing, retirement timing, and emergency planning all hinge on probability and uncertainty.

The Real-World Cost of Low Literacy

Adults with very low financial literacy are 2x as likely to be debt-constrained, 3x more likely to be financially fragile, and 5x more likely to lack even one month of emergency savings. They burn 10 hours every week obsessing over financial issues, while those with high literacy spend just 4. This isn’t just a knowledge gap, but a massive drain on time and mental energy.

The pressure is mounting as retirees rethink how to generate income without draining their principal in a volatile market. With only 23% of adults understanding the likelihood of needing long-term care and just 26% clear on what Medicare actually covers, the margin for error is razor-thin. Shifting toward a 5% income strategy is becoming a necessary response to rising costs and longer life expectancies.

Eight Years, Same Score

Wage growth hasn’t moved the needle on financial understanding. Even with a stable employment market and years of post-pandemic adjustments, the results remain stuck at the same low levels. We have cycled through multiple policy environments and persistent inflation, yet the answer key produces the exact same stagnant score. This consistency proves that simply living through a cycle isn’t enough to build real financial fluency.

Contact [email protected] for any questions or corrections.