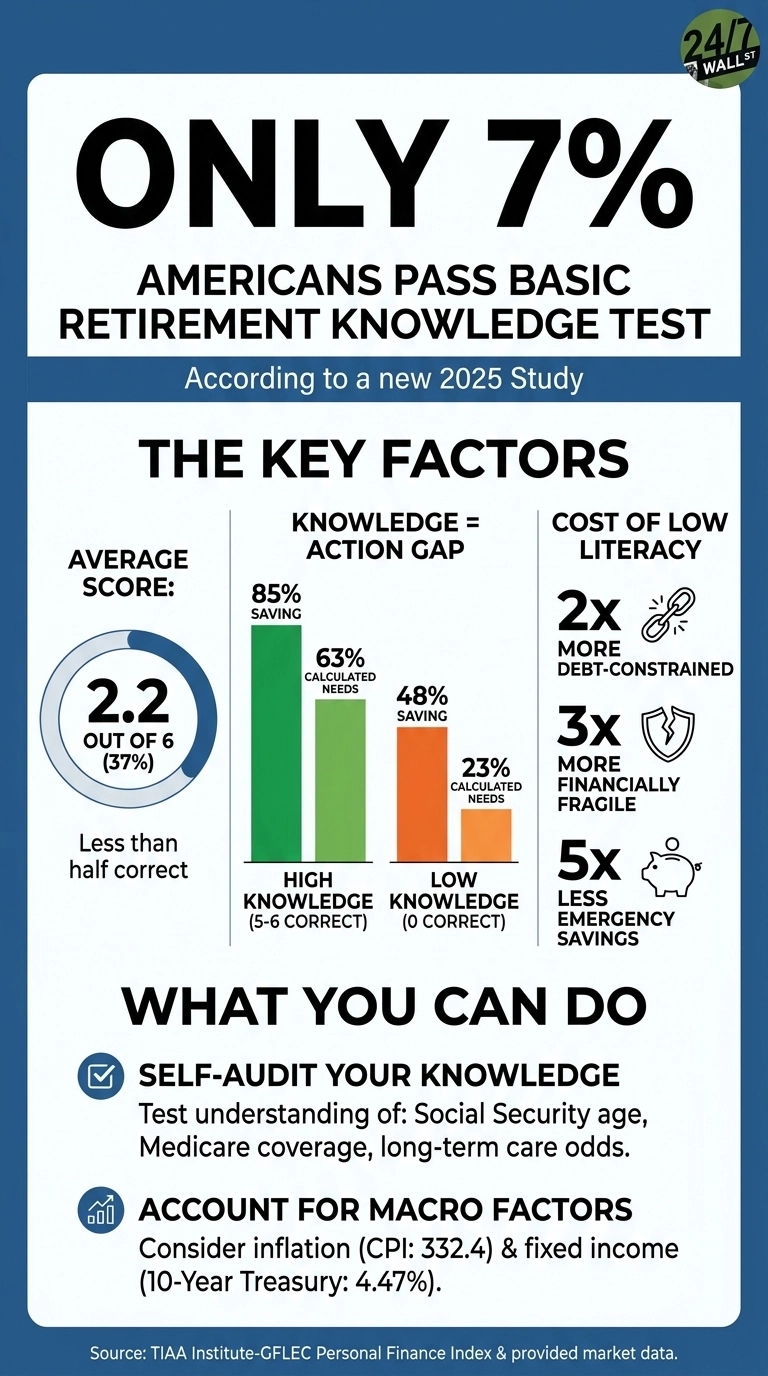

A new study from the TIAA Institute and the Global Financial Literacy Excellence Center sets a deliberately low bar for retirement knowledge, then watches almost everyone walk under it. The test covers six essential topics, including Social Security, Medicare, workplace savings, annuities, long-term care odds, and life expectancy. Only 7% of Americans can answer five or six of these correctly. With an average score of just 37%, most adults are guessing on the fundamentals, and that knowledge gap translates directly into higher debt, lower savings balances, and a much greater risk of running out of money.

The Bar Is Low. Most People Still Miss It.

The six questions are not technical. They ask whether Social Security benefits adjust for inflation, what Medicare covers, and what an annuity does. The average American gets only 2.2 of the 6 right, or a measly 37%. Accuracy ranges from 53% on the annuity question down to 23% on the likelihood of needing long-term care. The long-term care question is particularly revealing (and concerning), as most adults over 65 will need some form of paid care, and Medicare does not cover it beyond a few weeks. Three out of four Americans do not know that.

The 7% figure functions as a competence cutoff. Below that line, retirement decisions are made without basic facts. This includes when to claim Social Security, whether to roll a 401(k) into an IRA, what an annuity guarantees, and how long a portfolio must last.

What the Gap Actually Costs

The study connects knowledge scores to behavior, and the spread is wide. Among workers who answer five or six questions correctly, 85% are saving for retirement, and 63% have calculated how much they will need. Among workers who answer zero correctly, only 48% are saving, and just 23% have run the numbers. The high-fluency group is nearly three times more likely to have done basic retirement math.

The cost extends beyond retirement accounts, as adults with very low financial literacy are twice as likely to be debt-constrained, three times as likely to be financially fragile, and five times as likely to lack one month of emergency savings as those with very high literacy. A household without one month of cash reserves is one car repair away from credit card debt, and current credit card rates compound faster than most retirement accounts grow.

The Macro Backdrop Makes It Worse

The savings environment offers no cover for those lacking the basics. Americans are earning more but saving less, and inflation is the silent predator that most retirement-illiterate savers ignore. The study shows that “comprehending risk” is the weakest area of adult knowledge, meaning most people don’t realize how rising costs quietly erode their real-world purchasing power.

Fixed-income yields might offer a path forward, but they are only useful if you understand the mechanics of an income plan. While current rates provide a baseline for retirees, the reality is that most adults struggle with the fundamentals of investing and insuring. The gap between nominal returns and real yield is where plans fail, simply because the average saver lacks the fluency to tell a usable number from a risky bet

Who Is Falling Furthest Behind

The averages hide sharper splits. Gen Z scores 38% on overall financial literacy compared with 55% for older generations. Women score roughly 10 percentage points below men, and Black and Hispanic Americans average 38% to 39% correct compared with 53% to 55% for White and Asian Americans. These variances are substantial, marking the difference between entering retirement with a plan and entering it with a guess.

How to Check Whether You Are in the 7%

The six topics on the test serve as a reasonable self-audit. A reader who can answer the following without looking anything up is likely in the top decile: the age at which Social Security benefits maximize, what share of medical costs Medicare covers, the lifetime probability of needing long-term care, what an immediate annuity guarantees, average life expectancy at age 65, and roughly how much a 401(k) needs to replace a middle-class income. A reader who cannot answer most of these is in the same position as the 93% who fail the test, and the study is clear about what that position costs.

Contact [email protected] for any questions or corrections.