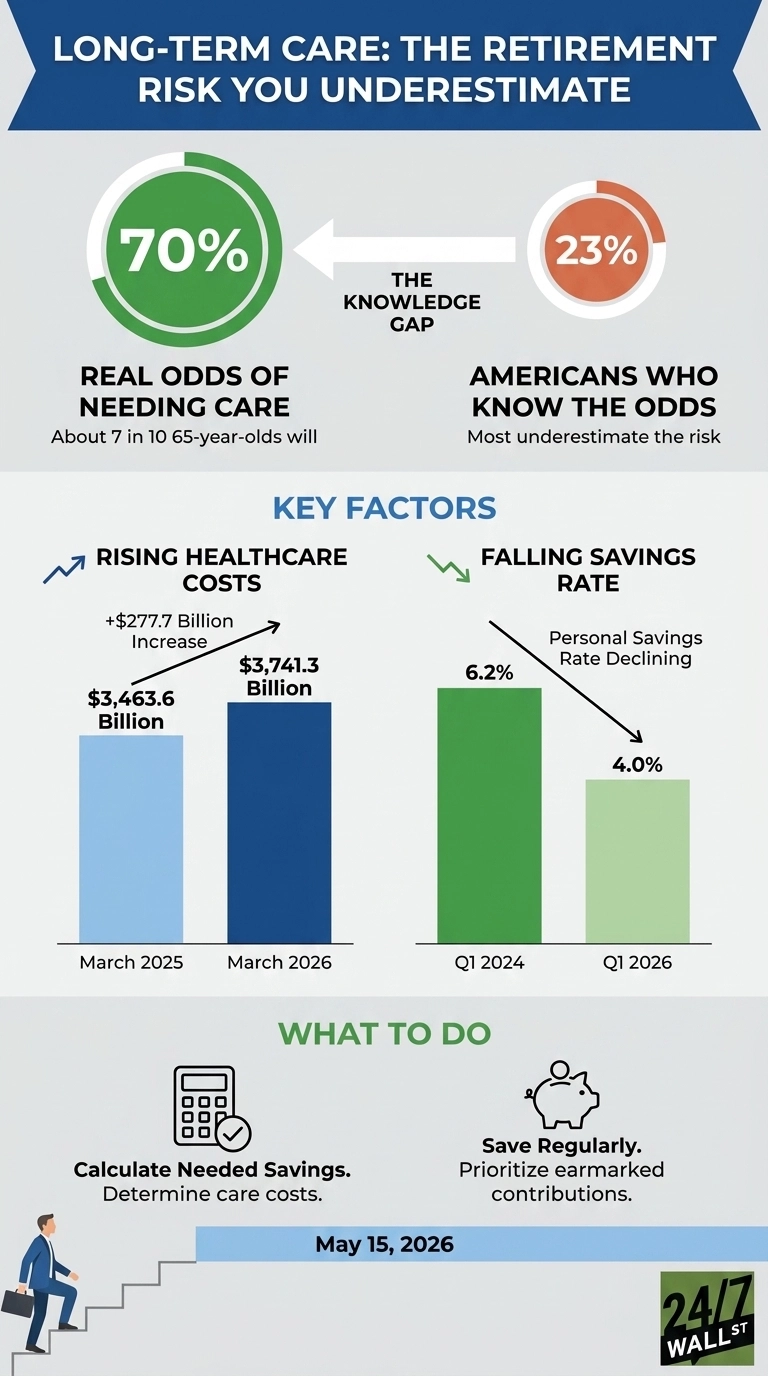

A new survey on retirement knowledge in America landed on a notable finding. When asked the likelihood that a 65-year-old will eventually need some type of long-term care, only 23% of U.S. adults answered correctly. The right answer, according to the 2025 P-Fin Index from the TIAA Institute and GFLEC, is about 70%, or 7 in 10. That gap between perception and reality frames the rest of the data, especially when you learn that most Americans are budgeting their retirements around a risk they have badly underestimated.

Long-term care is the part of aging that Medicare largely does not pay for: help with bathing, dressing, eating, and moving around, whether delivered at home, in assisted living, or in a nursing facility. It is the line item that quietly drains retirement accounts because households assumed it was covered. The P-Fin question is so consequential because the answer determines how much of a nest egg has to be earmarked for care rather than spent on living.

What it costs to be wrong

The price tag on that misunderstanding is rising in real time. U.S. personal consumption on healthcare reached $3,741.3 billion in March 2026, up from $3,463.6 billion a year earlier. This $277.7 billion increase outpaced every other major service category, including housing. Healthcare prices rise faster than overall inflation, and the headline Consumer Price Index at 332.4 in April 2026 understates what care-heavy households actually experience. This is especially dangerous, as only 36% of adults correctly understand financial risk.

The Federal Reserve’s preferred gauge tells the same story. Core PCE has climbed from 125.79 in May 2025 to 129.28 in March 2026, a steady grind upward that compounds for anyone planning a 20 or 30-year retirement. Currently, only 23% of Americans correctly understand the likelihood of needing long-term care in older age. A care need that looks affordable on today’s price sheet looks very different by the time it actually arrives, yet only 7% of adults demonstrate high retirement fluency regarding these core costs.

Households are saving less, not more

The financial cushion to absorb a surprise care bill is also thinning. The personal savings rate has fallen from 6.2% in the first quarter of 2024 to 4.0% in the first quarter of 2026, even as per capita disposable income rose to $68,617. Income gains are being spent, not banked.

Absolute personal savings have contracted from $1.33 trillion to $942.3 billion over that same window. Consumer sentiment data helps explain this behavior. The University of Michigan Consumer Sentiment index reads 53.3 as of March 2026, well inside pessimistic territory and within sight of recessionary levels near 60. When households feel squeezed today, planning for a care event that may be a decade or two away tends to slide down the list.

This shift in priority is dangerous because Americans already lack the basic knowledge required to navigate long-term costs. The 2025 P-Fin Index shows that only 23% of adults correctly understand the actual likelihood of needing long-term care services. Furthermore, adults with very low financial literacy are 5x more likely to have no emergency savings at all. When current sentiment is low and savings are shrinking, the knowledge gap regarding future care needs poses a massive risk to retirement security.

Who knows, and who doesn’t

The P-Fin survey confirms that the knowledge gap is not evenly distributed across the population. Men outperformed women on retirement fluency questions, and Asian and White respondents scored significantly higher than Black and Hispanic respondents. Generationally, Gen Z and Gen Y scored substantially lower than older cohorts. While that is intuitive, it cuts the wrong way because the people with the longest runway to prepare are the least informed about what they need to prepare for.

The link between knowing and doing is the part worth pausing on. Among workers who answered five or six retirement fluency questions correctly, 85% regularly save for retirement, and 63% have calculated how much they need to save. Among workers who answered none correctly, those figures fall to 48% and 23%. Knowing the odds appears to change behavior.

The honest read

The data is blunt: roughly 7 in 10 65-year-olds will eventually need some form of long-term care. Most Americans assume that number is much lower, and that misconception is colliding with healthcare costs that are climbing faster than household savings. Medicare is not the comprehensive safety net many households assume it to be, as it covers only about half of retiree healthcare expenses on average.

Anyone building a retirement plan without a dedicated answer for long-term care, whether through insurance, earmarked savings, or home equity, is making a massive mistake. Currently, only 23% of adults correctly understand the high likelihood of needing care. If you are not accounting for this, you are effectively planning around a 23% understanding of a 70% risk.

Contact [email protected] for any questions or corrections.