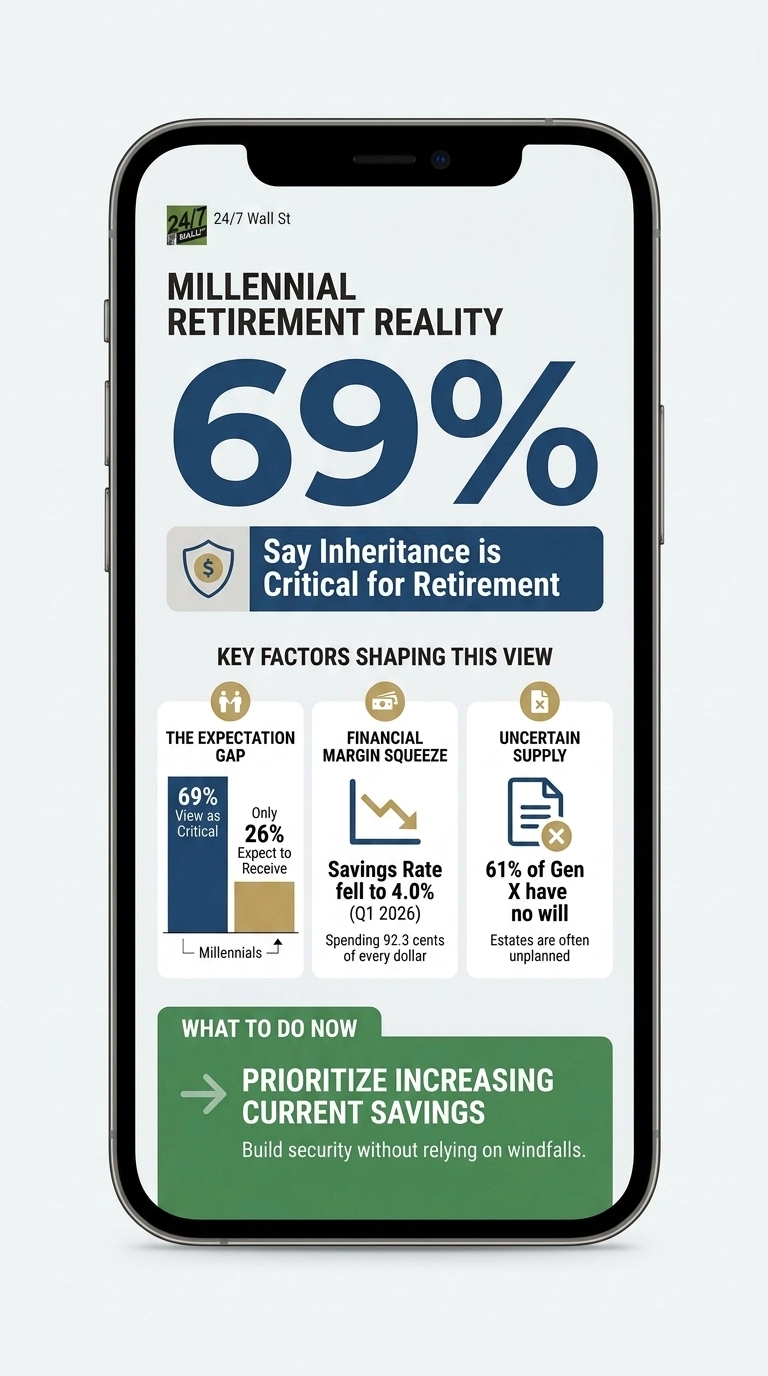

Northwestern Mutual’s 2025 Planning & Progress Study landed on a number that reframes how a generation is approaching retirement. 69% of Millennials say an expected inheritance is “critical” or “highly critical” to their long-term financial security or retirement, well above the 57% average across all inheritance-expecting adults. The framing matters, as a generation that came of age through two recessions, a pandemic, and a housing market that priced many of them out is now telling pollsters that someone else’s estate is a critical component of their retirement plan.

The mathematical reality presents a massive complication: only 26% of Millennials now expect to receive an inheritance, down from 32% in 2024. Gen Z expectations simultaneously slipped from 38% to 30% over the exact same period. Building an entire retirement strategy around a wealth transfer that the vast majority of recipients no longer expect to receive turns a financial plan into a mere gamble. The widening gulf between critical dependence and actual likelihood is exactly where structural fragility lives.

Why inheritance feels load-bearing

The harsh macro backdrop directly explains why an anticipated generational windfall has morphed into a critical planning anchor. The national personal saving rate plummeted from 6.2% in the first quarter of 2024 to 4.0% in the first quarter of 2026, even as per capita disposable income rose from $63,638 to $68,617. Working households are technically earning more paper wealth while keeping far less of it. Modern consumers are currently burning through 96 cents of every single disposable dollar, leaving an incredibly thin margin for independent retirement contributions on top of immediate daily obligations.

It’s important to acknowledge that wages have moved, but the cost of living has moved with them. Average hourly earnings rose from $34.47 in January 2024 to $37.41 in April 2026. Over a similar window, the Consumer Price Index climbed from 308.417 in January 2024 to 333.020 in April 2026. Wage growth has tracked prices closely, which means the real surplus available for long-horizon saving has barely expanded.

Essential consumer spending reveals exactly where the inflationary pressure concentrates. Annualized housing services consumption jumped from $3,745.9 billion in March 2025 to $3,904.5 billion in March 2026, while healthcare expenditures climbed rapidly from $3,463.6 billion to $3,741.3 billion. Domestic consumer sentiment registered a bleak 53.3 in March 2026, a depressed level that the University of Michigan firmly classifies within traditional recessionary territory. Any modern household watching housing and healthcare costs rise faster than its base paycheck has rational reasons to treat a future inheritance as a critical financial life-support system.

The planning gap on the other side

The supply side of the generational wealth equation remains significantly weaker than the soaring demand side assumes. Exactly 61% of Gen X and 39% of Boomers do not have a formal will, while a meager 60% of individuals planning a legacy have had direct family conversations about their intentions.

Undocumented estates routinely dissolve through aggressive probate court battles, tax liabilities, late-stage healthcare expenses, and intense legal disputes. A Millennial blindly banking on a massive six-figure windfall might ultimately inherit a minor sliver of that capital, long after the ideal wealth-building window has slammed shut.

Younger generations are aggressively internalizing this legacy obligation in reverse. Fully 74% of Millennials and 68% of Gen Z who expect to leave an inheritance describe the task as a paramount financial goal, compared with 66% of Gen X and 47% of Baby Boomers. A cohort that treats incoming family wealth as an absolute survival necessity is simultaneously prioritizing outgoing wealth transfers above other financial milestones, a compounding pressure that radically compresses their immediate cash savings.

What the data actually shows

Structuring a long-term retirement plan around a future inheritance relies on a volatile gamble regarding mortality timelines, asset valuations, sibling dynamics, and legal documents that frequently do not exist. The Northwestern Mutual report reveals a vulnerable demographic tying its financial destiny to that unstable projection anyway, simply because accumulating a sufficient nest egg from squeezed household paychecks remains incredibly difficult under a restrictive 3.75% benchmark interest rate and a 4.61% 10-year Treasury yield that aggressively inflates consumer borrowing costs.

The honest read is that 69% is less a plan than a measurement of fragility. Inheritance dependency rises when current income cannot stretch to cover both today’s essentials and tomorrow’s retirement. The figure captures what a generation is hoping arrives, and how much of their retirement security they have quietly pinned to that hope.

Contact [email protected] for any questions or corrections.