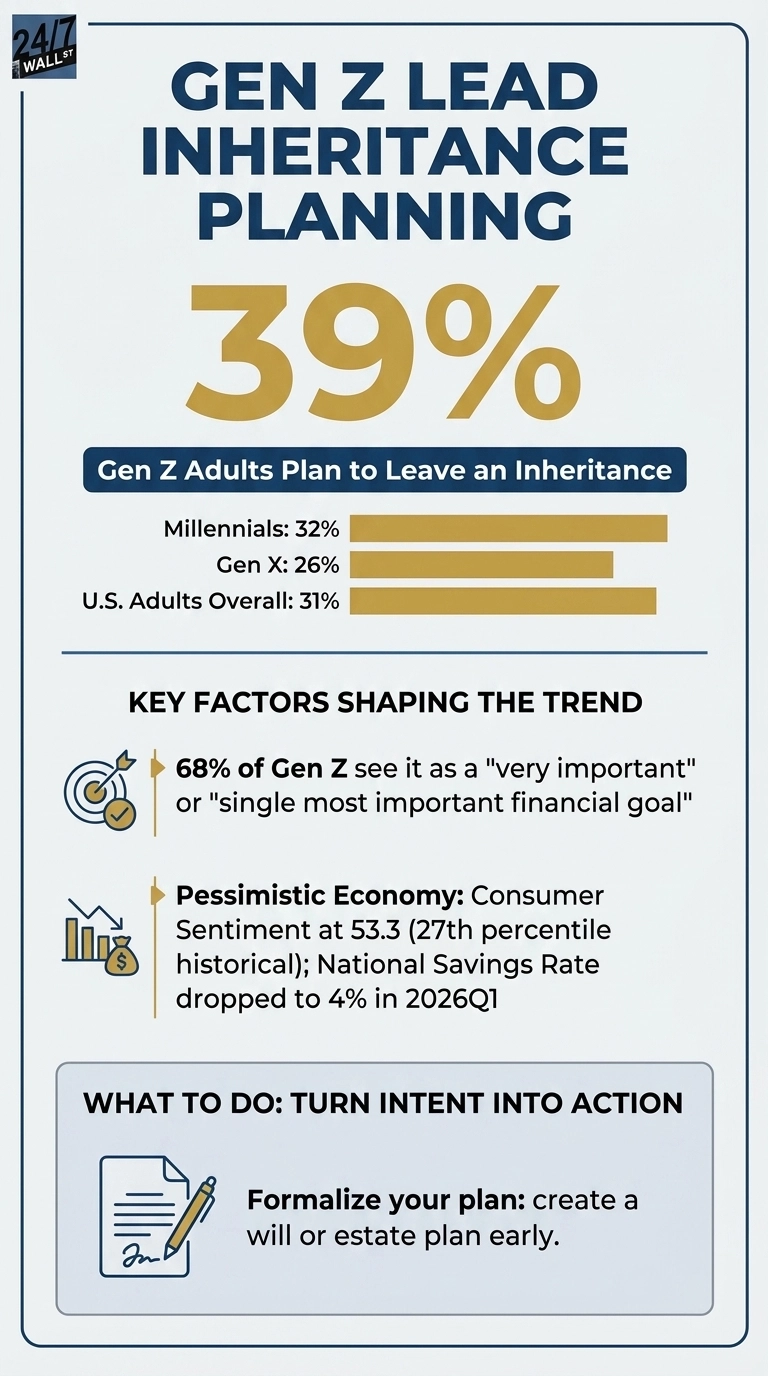

Northwestern Mutual’s 2025 Planning & Progress Study revealed a unique finding that runs counter to the usual generational script: 39% of Gen Z adults plan to leave an inheritance, a higher share than any other living generation. The exact cohort most often described as financially fragile, saddled with historic student debt, priced out of housing, and highly skeptical of traditional institutions is, ironically, the one most committed to passing wealth down the line.

That ambitious figure stands noticeably above the rest of the domestic population. Millennials come in at 32%, Gen X lands at 26%, and a baseline of 31% of U.S. adults overall expect to leave a legacy behind. Baby Boomers, the demographic closest to the actual wealth transfer window, track at 30% for execution expectations, meaning the older generation simply places a much lower psychological priority on the goal than their younger counterparts do.

Why the youngest adults rank legacy highest

The intensity behind the Gen Z number is what makes it more than a curiosity. Among those expecting to leave an inheritance, 68% of Gen Z call it their “single most important financial goal” or “very important,” compared with 66% of Gen X and 47% of Boomers+. For a generation that has not yet hit peak earnings, ranking legacy above other financial goals is a structural statement about how they view money, treating it as something that moves through families rather than something accumulated and spent within a single life.

Part of the explanation sits in the macro backdrop Gen Z came of age in. The University of Michigan Consumer Sentiment Index stands at 48.2 as of May 2026, indicating consumer confidence has plunged into pessimistic territory. The Consumer Price Index sits at 331.2 in April 2026, up from 320.1 a year earlier, representing a sustained squeeze on the categories that younger adults spend most on. The national savings rate has dropped to 4% in 2026Q1 from 6.2% in 2024Q1. Growing up watching disposable income absorb steady price pressure shapes how a 22-year-old defines financial success.

Inheritance as financial infrastructure, not a windfall

Gen Z views inheritance as a core financial pillar rather than a luxury bonus. Within the younger demographic expecting family assets, a striking 63% view those incoming funds as critical to their enduring financial stability, mirroring the 69% peak reported by Millennials. Labeling an inheritance as a load-bearing necessity proves that modern long-term blueprints are completely broken without family help. Recognizing that their own survival hinges on parental wealth sparks a fierce determination in these young adults to pass the torch forward.

Fierce real estate hurdles are directly driving this intergenerational mindset. Domestic housing starts notched 1.42 million annualized units in March, which fails to ease the affordability crisis crushing first-time buyers. Total per capita disposable income climbed to $68,617 during the first quarter, while average hourly earnings ticked up to $36.85 this spring from a $34.47 baseline in early 2024.

Even though take-home pay is increasing, it cannot keep pace with the ballooning down-payment requirements in the current market. Cash gifts from parents are the only mechanism bridging that massive gap for younger buyers, and experiencing that dependency shapes their goal of providing the exact same safety net later.

Intent runs ahead of execution

The same study flags a separate problem, as 39% of Boomers+ and 61% of Gen X do not have a will. Older generations who intend to pass wealth on have not formalized how to do so. Gen Z’s stated intent sits atop a system where the mechanics of transfer often fail when needed. The labor market backdrop, with unemployment at 4.3% in April 2026, is supportive enough that Gen Z has the runway to do the planning their parents and grandparents have largely deferred.

What the number actually says

The Northwestern Mutual data documents an attitude rather than a realized outcome. Gen Z has not yet built the balance sheets needed to make 39% a realized statistic decades from now. What the study captures is a generation that watched wealth get harder to assemble and concluded that the answer is to think about money in multi-generational terms from the start. Whether that intent survives child care costs, mortgage rates, and the savings-rate environment they are inheriting remains an open question. For now, the youngest adults are the most committed to leaving something behind, and that itself is a shift in how Americans talk about wealth.

Contact [email protected] for any questions or corrections.