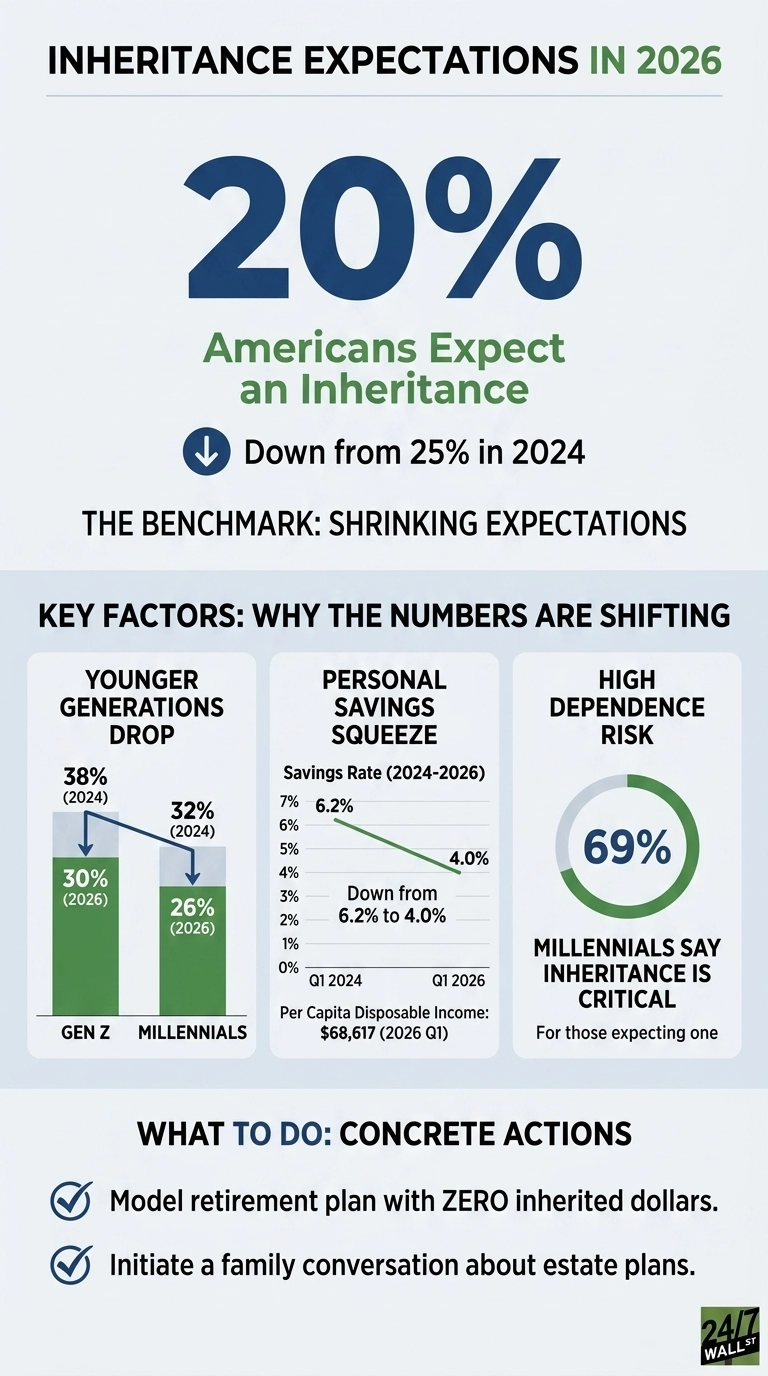

Inheritance expectations are shrinking just as more Americans are quietly counting on them. According to Northwestern Mutual’s 2025 Planning & Progress Study, only 20% of U.S. adults now expect to receive an inheritance, down from 25% in 2024. That five-point drop in a single year is a meaningful signal for anyone in their 40s building a retirement plan around a future windfall. The math behind the windfall is deteriorating.

The decline is sharpest among those with the most years of compounding ahead of them. Gen Z expectations dropped from 38% to 30% year over year, and Millennials fell from 32% to 26%. Younger workers were the demographic most likely to fold an inheritance into their long-term assumptions, and they are now revising those assumptions down faster than anyone else. Parents and grandparents are living longer, spending more on healthcare, and watching their own savings capacity erode.

Why the windfall is shrinking

The structural savings squeeze on the people who would otherwise be leaving a legacy is evident in federal data. The personal savings rate has slid from 6.2% in the first quarter of 2024 down to 4.0% in the first quarter of 2026, even as nominal per capita disposable income climbed to $68,617. Wages consistently climbed while savings receded because essential daily costs absorbed the difference. Essential housing and healthcare expenditures have both expanded rapidly over the past 15 months, allowing inflation to systematically compound household pressures.

Consumer sentiment highlights exactly how this financial environment feels at the kitchen table. The University of Michigan index crashed all the way down to 48.2 for May 2026, landing deep inside pessimistic territory and matching classic recessionary readings. When the segment of the population that intends to leave money behind feels financially restricted by basic living expenses, they are forced to spend down legacy assets that would otherwise transfer to the next generation.

The dangerous part: how many are counting on it anyway

Even as the share of individuals expecting to receive an inheritance tightens, financial dependence among those heirs intensifies. The Northwestern Mutual study found that 57% of Americans expecting a wealth transfer say the incoming funds are critical or highly critical to their long-term financial security. For Millennials, that specific dependency metric rises to 69%. Roughly seven in ten Millennials who still anticipate an inheritance have woven it into the load-bearing parts of their retirement roadmaps, creating a stark contrast with overall expectations for volatile assets.

The planning side of the equation remains no better organized than the receiving side. While 31% of Americans say they expect to leave an inheritance or charitable gift, only 60% of that cohort have actually had a direct family conversation about their intentions. The formal estate paperwork is even thinner across households. Exactly 39% of Baby Boomers lack a foundational will, and 61% of Gen Xers lack one as well. A retirement strategy that hinges entirely on a generational transfer that nobody has documented, costed, or actively discussed introduces substantial execution risk to the family structure.

What it means for a 40-something to build a retirement plan

The honest read of the data is that, for the typical American household, inheritance has become a possibility rather than a line item. Independent saving has to do the work, and the macro backdrop makes that harder. Unemployment is steady at 4.3% as of April 2026, so paychecks are intact, but the savings rate trend shows the surplus is thinning.

Two adjustments follow from the data. The first is modeling retirement plans with zero inherited dollars and treating any transfer that does arrive as upside, particularly for households under 45, where the expectation rate fell the most.

The second is the family conversation itself. With 40% of would-be givers never having discussed the topic with family and a majority of Gen X lacking a will, the gap between assumed and actual transfers is likely to widen before it narrows. The number to plan around is the one already in the account.

Contact [email protected] for any questions or corrections.