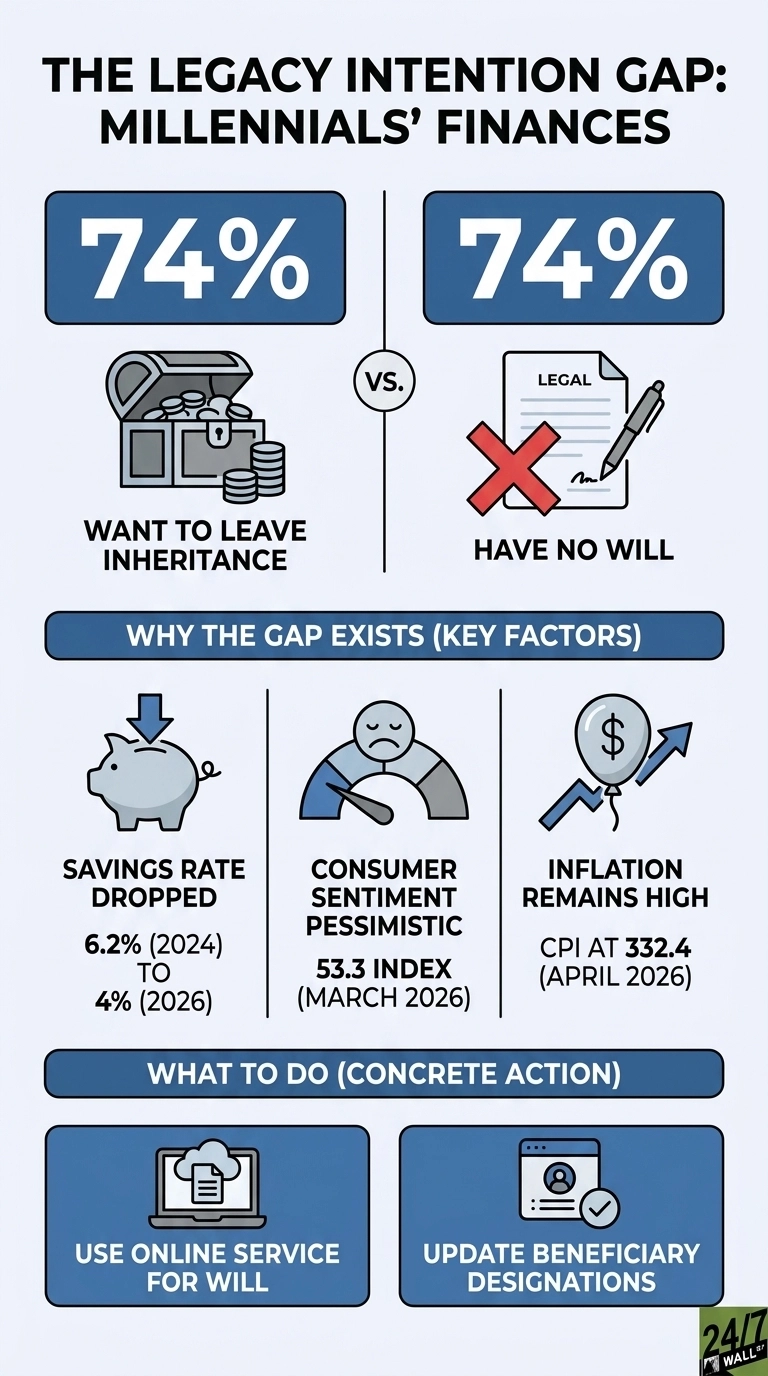

Two contrasting metrics from Northwestern Mutual’s 2025 Planning & Progress Study clash awkwardly when analyzed side by side. Fully 74% of Millennials say leaving an inheritance is either their paramount financial milestone or a highly important objective, marking the steepest legacy-priority rate of any age group besides Gen Z.

Yet across the broader survey pool, estate planning metrics remain incredibly bleak: 61% of Gen X and 39% of Baby Boomers have no written will, and Millennials mirror that exact lack of preparation. A demographic that elevates wealth transfer to the absolute peak of its financial aspirations has failed to execute the singular legal instrument required to make that dream enforceable.

The competing metrics cannot logically coexist. Either executing a wealth transfer represents a critical priority that demands legal paperwork, or the objective is merely a vague aspiration. The Northwestern Mutual data, gathered by The Harris Poll among 4,626 domestic adults between January 2 and January 19, 2025, makes this behavioral double standard impossible to ignore.

The intention side looks serious

Millennials are treating this as a deliberate financial goal: 32% expect to leave an inheritance or charitable gift, and, among that group, leaving something behind ranks above retirement security, debt payoff, and almost everything else they were asked about. That is unusual for a cohort whose oldest members are barely in their mid-forties and whose youngest are still building emergency funds.

The intention extends to their balance sheets. Northwestern Mutual found that 69% of millennials who expect to receive an inheritance call it critical or highly critical to their long-term financial security. Their retirement math, home-buying math, and debt-payoff math all rely on a transfer from parents who, according to the same study’s numbers, have not completed the legal work to make that transfer clean.

The preparation side does not

The persistent will gap is where the national narrative ceases to be merely aspirational. Among legacy-focused households, a modest 60% have even initiated a basic family dialogue regarding their asset distribution plans. The singular legal mechanism that actually dictates asset ownership remains entirely absent for most Gen X adults and a massive portion of aging Americans.

Passing away without a valid will surrenders all asset distribution decisions directly to state intestacy laws. Probate courts stall, administrative expenses skyrocket, and family wealth filters through a rigid statutory formula that frequently blindsides surviving relatives. For a younger demographic that elevates wealth transfer to the absolute peak of its long-term goals, that chaotic outcome represents the total destruction of a family legacy.

Why the document keeps getting deferred

The harsh economic backdrop helps explain the widespread behavioral inertia. The national personal saving rate has slipped from 6.2% in the first quarter of 2024 to 4.0% in the first quarter of 2026, even though nominal per capita disposable income climbed to $68,617. Working households are technically earning more paper wealth but keeping less cash, a squeeze that constantly pushes a few hundred dollars of estate-planning fees into next quarter, then next year.

The public mood further reinforces the documentation delay, with the University of Michigan consumer sentiment index registering a bleak 48.2 in May 2026, sitting deep in the pessimistic band below 80. The Consumer Price Index rose to 331.2 in April 2026, a painful 0.6% jump in a single month. When financial survival feels highly uncertain, distant administrative tasks like estate planning naturally slide.

The resilient labor market removes the usual job-loss excuse. National unemployment is hovering at 4.3% as of April 2026, which sits safely within the healthy 4% to 5% historical norm. Most employed Millennials are simply postponing.

Closing the gap

Most of the work fits into a single weekend, as an online service can produce a basic will and a durable power of attorney for a few hundred dollars. An estate attorney is worth the cost when there is a business, a blended family, or property in multiple states. Beneficiary designations on retirement accounts and life insurance policies override the will entirely and remain the single most common point of family conflict when an ex-spouse is still listed. The people named in any of these documents need to know they are named and where the documents live.

The Northwestern Mutual study documents an intention-action gap. Millennials who say leaving an inheritance is their most important financial goal, yet skip the will, contradict their own priorities. The data does not tell anyone what to do with that information, it just makes ignoring it harder.

Contact [email protected] for any questions or corrections.