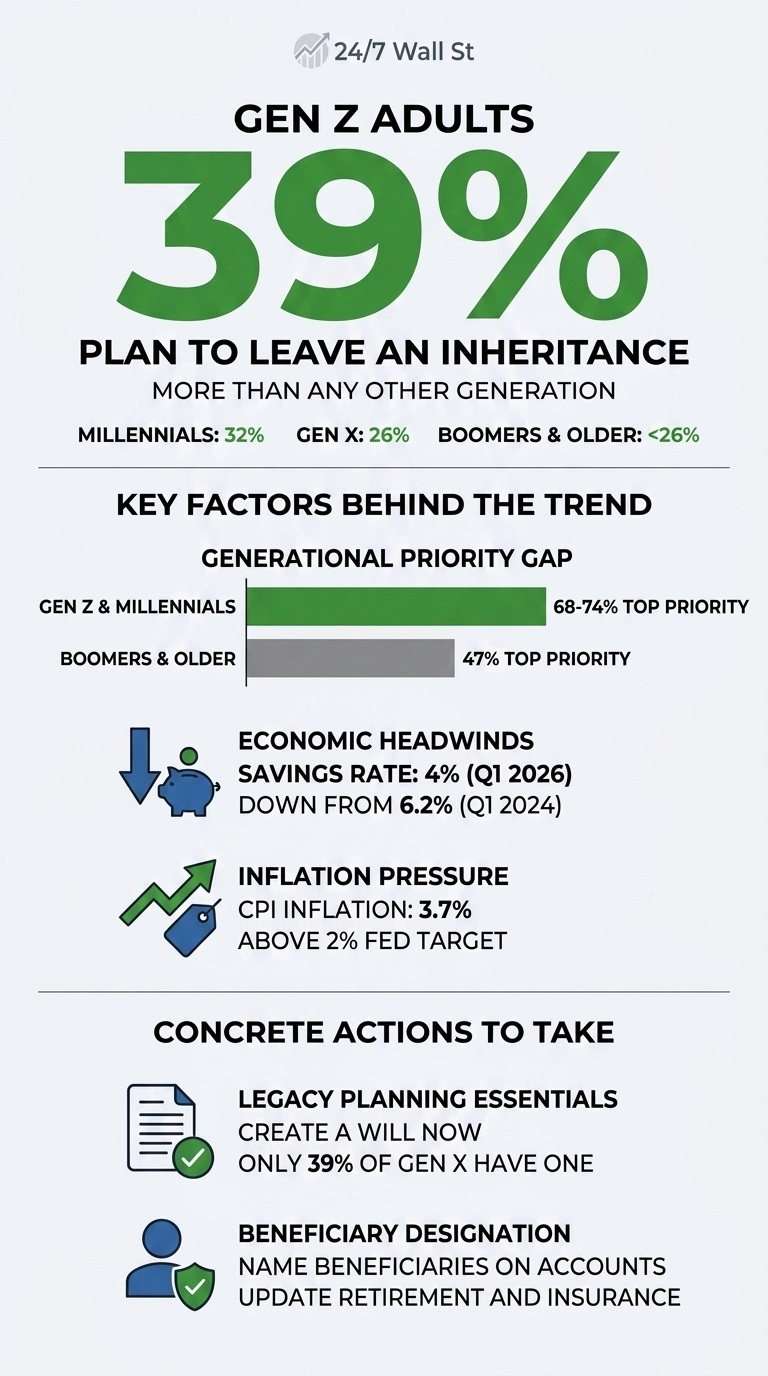

The headline finding from Northwestern Mutual’s 2025 Planning & Progress Study on Leaving a Legacy is the kind of result worth reading twice. The bottom line and biggest takeaway from this study is that 39% of Gen Z adults plan to leave an inheritance, more than any other generation. That share tops 32% among Millennials, 26% among Gen X, and an even lower share among Boomers and older Americans. In a surprising turn of events, it’s the youngest cohort that is the most committed to a financial legacy.

The Numbers Behind the Shift

The intuition most people carry is that legacy planning is something you grow into. People build assets, raise kids, watch parents pass, and eventually start thinking about what they leave behind. The Northwestern Mutual data says Gen Z skipped that arc entirely. Among the cohort that does plan to leave an inheritance, 68% of Gen Z and 74% of Millennials describe it as either their single most important financial goal or very important, compared with just 47% of Boomers and older. Younger adults are not only thinking about legacy earlier but also ranking it higher when they do.

The shift is showing up at the national level, too, with 31% of U.S. adults now expecting to leave an inheritance or charitable gift in 2025, a number that is up from 26% in 2024. A five-point jump in a single year is large for a survey question this stable. The easy answer is that something in the country’s financial mood has changed.

Why Younger Adults Are Planning Earlier

The economic backdrop shapes the way people think about planning. Consumer sentiment remains weak, with the University of Michigan index at 48.2 in May 2026, down from the prior month and well below the pessimistic band of 80. Inflation continues to weigh on households as well, with CPI growth running at 3.3% in March, still above the Federal Reserve’s 2% target, and the personal saving rate sliding from 6.2% in the first quarter of 2024 to 4.0% in the first quarter of 2026. When the present feels unstable, the planning horizon narrows, and tomorrow becomes the only point people feel confident modeling.

Wages, however, are moving in the opposite direction, giving younger adults something tangible to build on. Average hourly earnings reached $37.41 in April 2026, up from $35.84 in January 2025, marking a fresh high. The labor market has held steady, with unemployment at 4.3% in April 2026, comfortably within the 4.1% to 4.5% range that has persisted for a year. Against that backdrop, per capita disposable income climbed to $68,617 in the first quarter of 2026, up from $63,638 two years earlier, the kind of raw material a young saver needs to imagine building something worth passing on.

Generational Priority on Inheritance

Stacking the survey’s importance ratings against the planning rate makes the generational divide unmistakable.

- Gen Z — 39% expect to leave an inheritance, and among those who do, 68% say it is either their single most important financial goal or a very important one.

- Millennials — 32% plan to leave one, and 74% of that group rate it as a top priority.

- Gen X — 26% expect to leave an inheritance, but the study does not report a comparable “importance” percentage for this cohort.

- Boomers+ — 30% expect to leave one, and 47% of those who do call it a top priority.

The pattern is consistent across the data, starting with the reality that as generations get younger, both the intention to leave something behind and the urgency attached to it rise. Older Americans built wealth in an era when retirement security was the central objective and any remaining assets were incidental. Younger adults appear to be treating legacy as a primary goal rather than an afterthought.

The Intent-Action Gap

The shortfall shows up in the execution, as 61% of Gen X and 39% of Boomers+ do not have a will, even though both groups are closest to the point in life when one matters most. If the cohorts nearing retirement have not formalized their plans, the likelihood that Gen Z will do it early is even lower. Preference is not a plan. A real legacy strategy requires a will, updated beneficiary designations on retirement accounts and life insurance, and account titling that aligns with those documents. Without that structure, state intestacy rules determine the outcome.

What the Data Actually Says

The Northwestern survey shows Gen Z thinking about legacy earlier than any prior generation did at the same age, even as they navigate softer saving rates and weaker consumer confidence. The study does not tie this mindset to macro conditions, but it does make the generational pattern clear: intent is strong, and preparation is thin. Whether that intent becomes actual inherited wealth depends on three concrete steps: opening a will, naming beneficiaries on every retirement and insurance account, and saving at a level that leaves something behind. Ultimately, this survey captures the aspiration, but whether or not there is going to be follow-through remains uncertain.

Contact [email protected] for any questions or corrections.