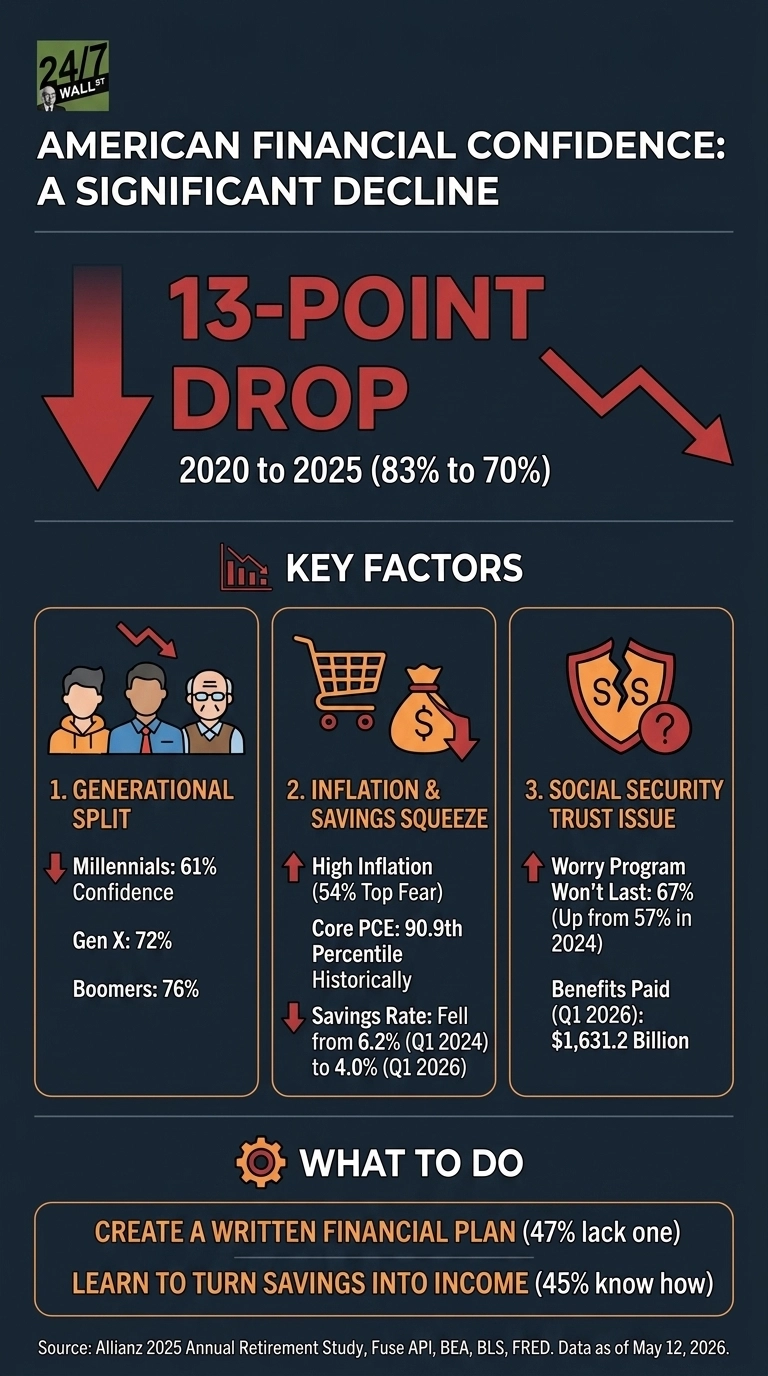

The Allianz 2025 Annual Retirement Study put a number on something many Americans already felt: confidence in their financial future has eroded at a measurable rate. Overall financial confidence dropped 13 percentage points from 2020 to 2025, falling from 83% to 70%. The decline is not evenly distributed, and the underlying macro data explains much of why the floor moved.

A 13-Point Drop, and Where It Hit Hardest

The headline figure obscures a generational split that is well worth discussing. Overall, Millennials report just 61% confidence, well behind Gen X at 72% and Boomers at 76%. Across racial demographic groups, confidence ranges from 68% to 75%. Millennials are the cohort that came of age during the 2008 financial crisis, bought homes (or tried to) during the post-2020 price surge, and are now staring at retirement timelines that depend on assumptions their parents never had to question.

Independent sentiment data corroborates the pattern. The University of Michigan Consumer Sentiment Index sat at 48.2 in May 2026, down from 61.7 in July 2025, and well below the 60-point threshold typically associated with recessionary readings. The index has historically been in the 27th percentile. Two separate measurements, one from a retirement insurer and one from a federally tracked survey, are pointing in the same direction.

The Fear Hierarchy

What Americans are afraid of has shifted from market crashes to grocery receipts. The Allianz study found 64% worry more about running out of money than about death itself. The top-ranked threats are high inflation (54%), Social Security not providing enough support (43%), and high taxes (43%). These reflect everyday cost pressures rather than portfolio anxieties.

Inflation data continues to validate the pressure households describe. The Consumer Price Index moved from 308.417 in January 2024 to 330.213 in March 2026, a climb that reinforces why so many Americans feel their budgets are tightening. Core PCE, the Federal Reserve’s preferred gauge, has spent this period near the 90.9th percentile of its historical range, a reminder that underlying price pressures have not eased in a meaningful way. Wage growth has continued to advance, with average hourly earnings rising from 34.76 dollars in April 2024 to 37.41 dollars in April 2026, yet the personal savings rate has moved in the opposite direction, falling from 6.2% in the first quarter of 2024 to 4.0% in the first quarter of 2026.

The pattern is straightforward, as households are earning more, saving less, and feeling the squeeze at the same time. The numbers point to an economy where income growth has not been enough to offset the rising cost of living, and where the margin for error in a family’s monthly budget keeps getting thinner.

The Social Security Trust Problem

Confidence in Social Security’s longevity has been slipping faster than almost any other sentiment in the Allianz study. The share of Americans who worry the program will not last through their full retirement rose to 67% in 2025, up from 57% in 2024, a shift the report highlights directly. The system itself continues to operate at full scale, with Social Security paying roughly $ 1.63 trillion in benefits in the first quarter of 2026, a total that continues to rise as the retired population grows. Concern is climbing even as the checks continue to go out, which points to a trust problem rather than an immediate solvency issue.

The Planning Gap

Confidence also reflects a knowledge deficit. 59% of Americans say they do not know what else to do to prepare for retirement beyond basic contributions, 47% lack a written financial plan, and only 45% know how to turn savings into retirement income. Even among active 401(k) and IRA contributors, Millennials (42%), Gen X (55%), and Boomers (54%) struggle with clarity in their plans. Saving is happening without a matching strategy.

The Behavior-Confidence Gap

One detail complicates the framing of the confidence recession. Retail sales hit $752.1 billion in March 2026, the highest in the 12-month period. The unemployment rate held at 4.3% in April 2026, and initial jobless claims were 200,000 for the week of May 2, 2026, within the healthy range. Americans report feeling worse even as they continue to spend, and the labor market beneath them has softened modestly. The Allianz figures capture how people feel about their futures. The spending and jobs data capture how they are currently behaving. Both can be true at once.

What the Data Documents

The Allianz study documents a measurable loss of faith, concentrated in the generation furthest from retirement and most exposed to the housing and inflation environment of the last six years. The macro indicators explain the finding. Confidence is responding to lived costs and to a Social Security debate that has grown louder, even as incomes rise and employment remains. Whether spending behavior eventually follows sentiment downward is the open question. The confidence number, for now, has already moved.

Contact [email protected] for any questions or corrections.