We’d all like to be rich.

As finance coach Dave Ramsey often says, “the rich get richer and the poor get poorer.”

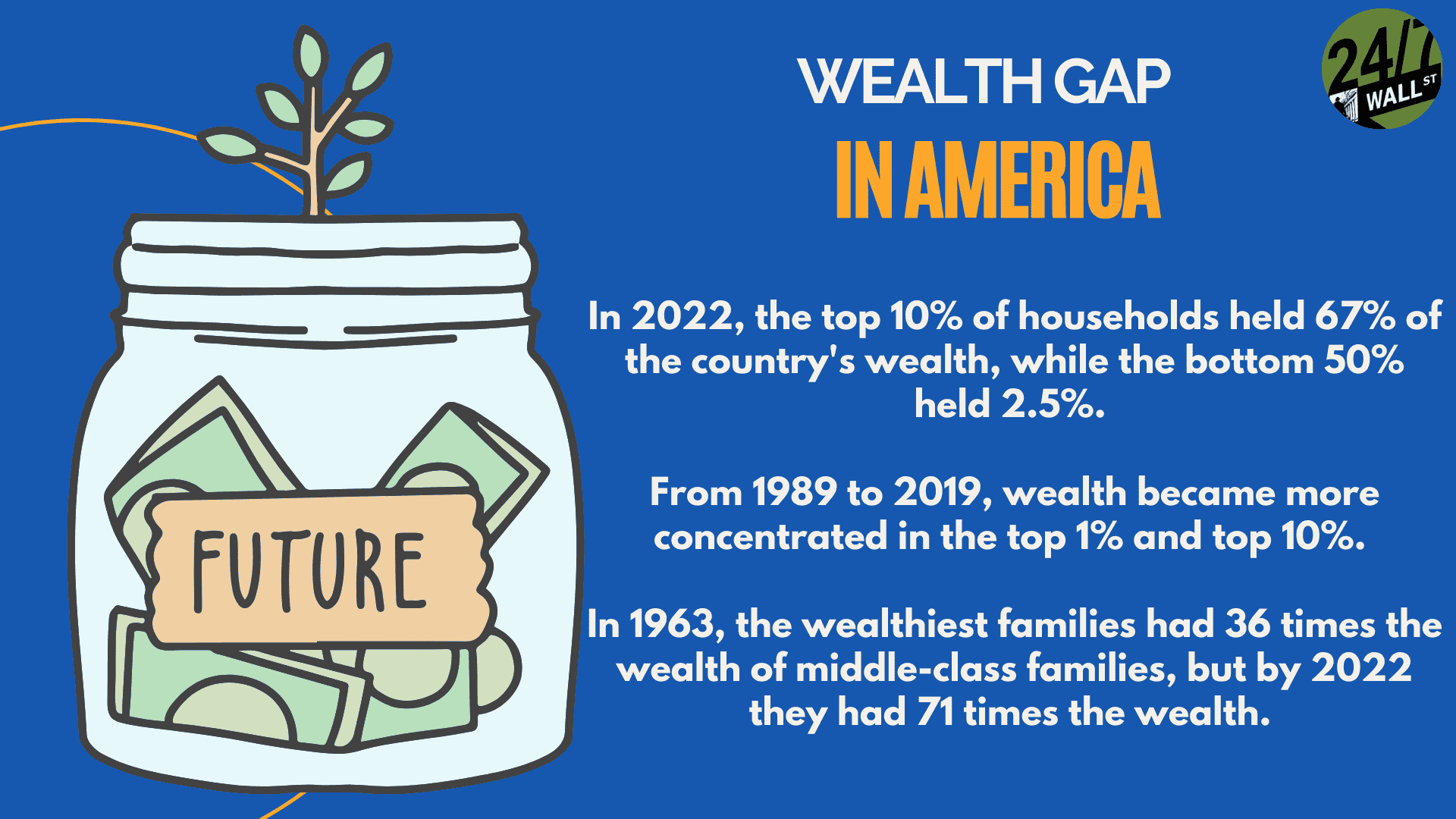

The numbers behind America’s wealth gap

The scale of the divide is hard to overstate. According to the St. Louis Federal Reserve’s Distributional Financial Accounts covering the fourth quarter of 2024, the top 10% of U.S. households by wealth held an average of $8.1 million each. As a group, they controlled 67.2% of all household wealth in the country. The bottom 50% averaged just $60,000 each and, together, held roughly 2.5% of the nation’s total household wealth. That gap between $8.1 million and $60,000 is not a fluke. According to Ramsey, it is largely the product of habit.

So, why is the wealth gap so big?

According to Dave Ramsey, the gap comes down to financial behaviors and the everyday choices that keep people in the lower, middle, or upper class. The good news, in his view: the right habits are available to anyone willing to adopt them.

The rich, Ramsey says, skip the question “How much per month?” and ask instead: “How much?” Paying for things outright lets them sidestep the interest charges that quietly drain everyone else. That discipline, compounded over decades, is a core reason they stay wealthy. Ramsey Solutions’ National Study of Millionaires reinforces the point: eight out of ten millionaires built their wealth by investing in their company’s 401(k) plan, and 79% received no inheritance at all.

The middle class, by contrast, operates on installment plans. Monthly car payments, home improvement loans, and credit cards held for the airline miles are common patterns. Each individual payment may seem manageable, but financing everything collectively creates a significant drag on wealth-building that compounds over years just as surely as interest income compounds for the wealthy.

Ramsey reserves his sharpest observations for the habits that trap people at the bottom. He points to payday lenders, pawn shops, title loans, and rent-to-own services as tools that extract wealth from those who can least afford it. He also singles out the lottery: his documented view is that 78% of lottery tickets are sold in poor zip codes, and that lottery spending represents false hope rather than a genuine path out. Independent research backs the underlying disparity. According to data published by The Economist, residents of the poorest 1% of American zip codes spend about $600 a year on tickets on average, compared to $150 for those in the wealthiest 1%.

None of this, however, is permanent. Financial habits can change, and Ramsey’s broader message is that anyone can rewrite their trajectory.

Steps to build wealth

One: increase your income. Dividend stocks offer one avenue for passive cash flow. A part-time job is another. The core objective is simply to widen the gap between what comes in and what goes out.

Two: build a budget and actually use it. Without one, money disappears into a fog of small, untracked expenses. A budget makes spending visible, and visible spending is spending you can control. The most common answer people give when asked where their money went is “I don’t know,” and that uncertainty is financially destructive.

Three: create an emergency fund. Traditional advice sets the starter target at $1,000. Given current cost-of-living levels, a figure closer to $2,500 is more realistic for covering a major car repair or home expense. Setting aside roughly $210 a month reaches that goal within a year. The key is keeping this money in a dedicated, separate account with automatic contributions, and funneling any windfalls (bonuses, tax refunds, gifts) directly into it rather than spending them immediately.

Four: pay off your debt. Ramsey recommends the debt snowball method: list every debt from smallest to largest balance, then attack the smallest first while making minimum payments on the rest. Once the smallest balance is cleared, roll that freed-up payment toward the next. The momentum this builds, both mathematical and psychological, is substantial. The list should include student loans, car payments, credit cards, and eventually the mortgage.

2027 COLA outlook and what it means for retirement planning

For anyone building a retirement income plan, the Social Security cost-of-living adjustment (COLA) is worth watching closely. The 2026 COLA came in at 2.8%, a modest raise for the roughly 75 million Americans who receive benefits. The average monthly retirement benefit for retired workers currently stands at about $2,026. The outlook for 2027 has shifted sharply upward since that adjustment took effect.

The Senior Citizens League, a nonpartisan advocacy group, projects a 3.8% COLA for 2027 based on May 2026 CPI data. That would add about $79 a month to the average retiree’s check. Independent analyst Mary Johnson forecasts a higher 4.7%, driven by surging energy prices. Gasoline tracked by the CPI-W index jumped more than 40% year over year through May, while fuel oil rose nearly 59%. The official measurement window, covering July through September, just opened, so all current projections remain preliminary until the Social Security Administration makes its announcement in October 2026.

Wealthier retirees often treat COLA announcements as a prompt to revisit withdrawal strategies rather than defaulting to a fixed spending rule. When inflation accelerates, revisiting those guardrails can make a meaningful difference to how long a portfolio lasts.

Investing in your future

Five: live below your means. Personal finance voices from Dave Ramsey to Suze Orman converge on the same principle: distinguish between needs and wants, cut spending on wants, automate savings, and set a concrete savings target. The mechanics are straightforward. Following through is the hard part.

Six: invest in retirement accounts. An Individual Retirement Account (IRA) lets you grow money either tax-free or on a tax-deferred basis, depending on the type you choose. A traditional IRA often allows you to deduct contributions from your taxable income now. A Roth IRA uses after-tax dollars, but qualified withdrawals in retirement are entirely tax-free, making it a powerful long-term vehicle. For the self-employed, a Solo 401(k) offers the same basic structure as a workplace plan. Consult a financial advisor before choosing, since the right account depends on your income, tax situation, and timeline.

Editor’s note: This article has been updated to reflect Q4 2024 St. Louis Fed Distributional Financial Accounts data (top 10% average of $8.1 million, holding 67.2% of household wealth; bottom 50% average of $60,000, holding 2.5%) and current 2027 Social Security COLA projections: 3.8% from the Senior Citizens League and 4.7% from analyst Mary Johnson, both based on May 2026 CPI-W data, with the average monthly retired-worker benefit now at $2,026. Ramsey’s lottery statistic was aligned with his documented 78% figure, and Ramsey Solutions’ National Study of Millionaires data on 401(k) wealth-building was added.

Contact [email protected] for any questions or corrections.