Both CrowdStrike (NASDAQ: CRWD) and Palo Alto Networks (NASDAQ: PANW) operate at the center of enterprise cybersecurity, share the same AI-driven demand tailwind, and have each pulled back sharply in 2026. Yet their strategies, growth profiles, and recent moves look strikingly different.

Falcon Flies Higher, Cortex Consolidates

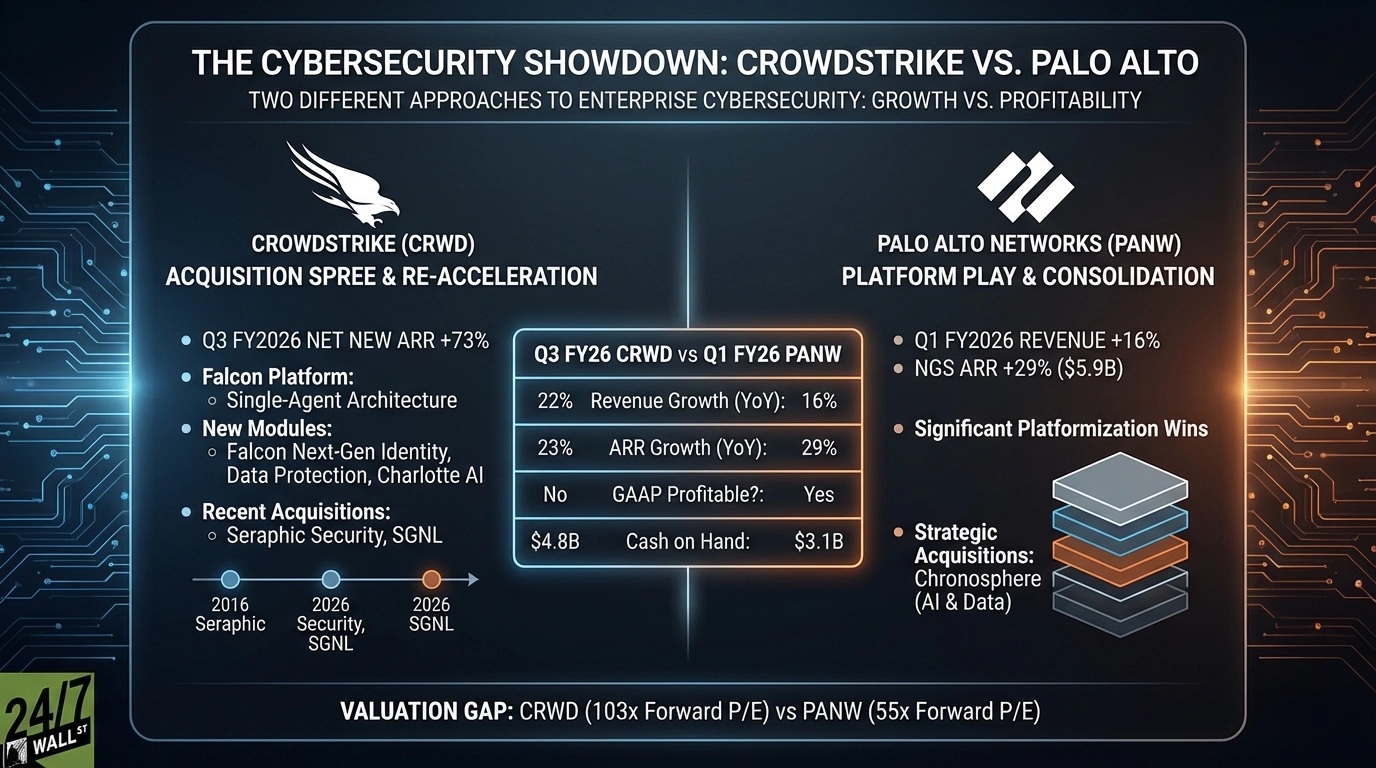

CrowdStrike’s Q3 FY2026 net new ARR of $265 million grew 73% year-over-year, a number that signals genuine re-acceleration after the July 2024 outage. CEO George Kurtz called it “one of our best quarters in company history.” The Falcon platform’s single-agent architecture, now extended through new modules like Falcon Next-Gen Identity Security, Falcon Data Protection, and Charlotte AI, keeps adding surface area without adding friction for customers.

Palo Alto reported Q1 FY2026 revenue of $2.50 billion, up 16% year-over-year, with Next-Gen Security ARR reaching $5.9 billion, up 29%. CEO Nikesh Arora emphasized “significant platformization wins” as the defining theme. The more recent Q2 FY2026 results showed revenue of approximately $2.6 billion, growing 15%, with Cortex XSIAM gaining traction as every new sale has been a seven-figure deal.

| Metric | CrowdStrike (Q3 FY26) | Palo Alto (Q1 FY26) |

|---|---|---|

| Revenue Growth (YoY) | 22% | 16% |

| ARR Growth (YoY) | 23% (ending ARR) | 29% (NGS ARR) |

| GAAP Profitable? | No | Yes |

| Cash on Hand | $4.8B | $3.1B |

Organic Builder vs. Serial Acquirer

CrowdStrike’s recent acquisitions of Seraphic Security (browser security) and SGNL (identity security) extend the Falcon platform into high-growth adjacent categories without abandoning the unified architecture thesis. Palo Alto has pursued a platformization strategy anchored by large acquisitions, including the $3.35 billion Chronosphere deal, adding AI and data capabilities to its Strata, Prisma, and Cortex stack.

Valuation Gap Tells Its Own Story

CrowdStrike trades at a forward P/E near 103x with analysts carrying a consensus price target of $543, well above the current $350 price. Palo Alto’s forward P/E sits near 55x with an average analyst target of $210 against a current price of $143. Both stocks are trading well below their 52-week highs and below their 200-day moving averages.

Two Different Approaches to Enterprise Cybersecurity

CrowdStrike’s ARR re-acceleration stands out as a pure growth signal, though GAAP losses and a premium valuation near 103x forward earnings reflect that growth expectation. Palo Alto’s platformization strategy is maturing, and its GAAP profitability has become an increasingly relevant factor for institutional holders in an elevated rate environment. The two companies represent different points on the growth-versus-profitability spectrum within enterprise cybersecurity. Both carry execution risk heading into a year where cybersecurity budgets are growing but integration costs and competitive pressure are rising simultaneously.