Live: Crowdstrike Holdings (CRWD) Q3 Earnings Coverage

Live Updates

Conference Call at 5 PM ET

Crowdstrike’s Conference call is scheduled for 5 pm E.T. Here are questions I will be focused on:

Key Analyst Questions:

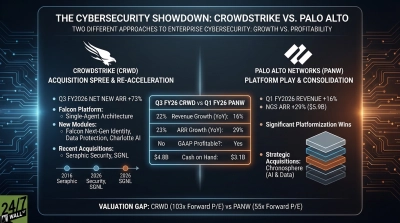

- ARR vs. Revenue Gap: Net new ARR surged 73% YoY to $265M (a record), yet revenue missed. Management must explain the timing disconnect.

- Profitability Path: $69M operating loss despite $4.92B ending ARR. When will scale drive positive operating income?

- AI Product Adoption: Charlotte AI, Falcon Next-Gen Identity, and Data Protection just launched. What’s the pipeline?

- Competitive Defense: With ServiceNow acquiring Veza for AI security today, how does CRWD defend share against Palo Alto (118x P/E)?

- FY27 Guidance: 20% net new ARR growth target represents significant deceleration from 73% in Q3. What’s driving the slowdown?

Red Flags: Vague answers on revenue timing or defensive commentary about the 50%+ operating expense ratio.

Where the numbers are guiding

Q4 FY26

| Metric | New Guidance | Prior Consensus | Trend |

|---|---|---|---|

| Revenue | $1.29B–$1.30B | ~$1.29B | Flat / Slightly Up |

| EPS (Non-GAAP) | $1.09–$1.11 | ~$1.08 | Raised |

| Op Income (Non-GAAP) | $315M–$319M | n/a | — |

Full-Year FY26

| Metric | New Guidance | Previous | Trend |

|---|---|---|---|

| Revenue | $4.796B–$4.806B | ~$4.78B implied | Raised |

| Non-GAAP EPS | $3.70–$3.72 | $3.68 consensus | Raised |

Raised ARR expectations (+50% YoY 2H target) are the biggest positive surprise. Street will treat this as evidence of sustained momentum entering FY27.

WHAT CHANGED THIS QUARTER

- ARR re-accelerated sharply — well ahead of pre-earnings “high bar.”

- Flex model adoption surpassed $1.35B ARR, confirming it is transforming deal sizes.

- Next-Gen SIEM momentum surged, supported by new AWS/EY/Kroll/KPMG partnerships.

- AI narrative strengthened — Charlotte AI FedRAMP High + agentic security rollout.

- Cash flow hit all-time highs, adding another pillar to the maturing profitability story.

- Guidance lifted, especially on ARR, which is the core driver of valuation.

Quotes From Management

“Q3 was one of our best quarters in company history… we achieved record Q3 net new ARR of $265 million, accelerating to 73% year-over-year growth… Our single platform strategy coupled with the Falcon Flex subscription model unlocks consolidation.”

CEO George Kurtz

Management is explicitly framing the quarter as a structural acceleration, not a one-off. Strength was broad, endpoint, cloud, identity, and SIEM, and Flex is positioning CRWD as the consolidation platform for enterprise security.

Earnings Are In and Crowdstrike Stock Is Up

Solid numbers coming from Crowdstrike and the stock is up 2% plus after-hours.

| Metric | Actual | Estimate | Beat/Miss |

|---|---|---|---|

| Revenue | $1.234B | $1.22B | ✅ Beat |

| EPS (Non-GAAP) | $0.96 | $0.94 | ✅ Beat |

| Net New ARR | $265M | Street ~ $240M–$255M | ✅ Beat |

| Ending ARR | $4.92B | ~ $4.90B implied | ✅ Beat |

- FY26 revenue raised to $4.796B–$4.807B

- Q4 EPS (non-GAAP) guided to $1.09–$1.11, above consensus

- Management raised 2H FY26 net new ARR growth outlook to ≥50%

This is one of CrowdStrike’s best ARR quarters ever. Net new ARR accelerated sharply, Flex ARR exploded, and cash flow set records. Guidance went up across the board, supporting why shares are steady-to-higher after hours.

Thoughts on Valuation Before Earnings Drop

CRWD enters earnings priced for continued leadership in AI-native security, platform consolidation, and ARR reacceleration. The central debate is whether the company can sustain back-half momentum while also navigating tougher compares, a volatile macro backdrop, and intensifying platform competition from Palo Alto, Zscaler, Microsoft, and Wiz.

If ARR growth, Flex burn rates, or SIEM/cloud momentum exceed expectations, the stock could justify further multiple expansion.

CrowdStrike (Nasdaq: CRWD | CRWD Price Prediction) reports after the close with expectations high following a second quarter marked by renewed acceleration and broad-based platform strength. Management emphasized that Q2 FY26 represented a turning point, net new ARR accelerated a full quarter earlier than anticipated, Charlotte AI adoption surged, and the company continued to gain share across cloud runtime, identity, and Next-Gen SIEM. Crowdstrike is up 48% in 2025 and up 2.4% today, heading into earnings at 4:05 PM ET.

What to Expect When CrowdStrike Reports

| Metric | Estimate | Year-Ago |

|---|---|---|

| Revenue (Current Qtr., Oct 2025) | $1.22 billion | $1.01 billion |

| EPS (Normalized, Current Qtr.) | $0.94 | $0.93 |

| Next Qtr. Revenue (Jan 2026) | $1.29 billion | $1.06 billion |

| Next Qtr. EPS (Normalized) | $1.08 | $1.03 |

| Full-Year 2026 Revenue | $4.78 billion | $3.95 billion |

| Full-Year 2026 EPS | $3.68 | $3.93 |

| Full-Year 2027 Revenue | $5.84 billion | $4.78 billion |

| Full-Year 2027 EPS | $4.80 | $3.68 |

Key Areas to Watch When CrowdStrike Reports

1. Net New ARR Momentum and Falcon Flex Burn Rates- Management said Q2 marked “reacceleration… a return to year-over-year net new ARR growth a quarter early” and guided to at least 40% YoY net new ARR growth in the back half. Flex utilization sits above 75%, re-Flex activity doubled, and re-Flex deals deliver ~50% ARR uplift — a central bull catalyst heading into Q3.

2. AI-Driven Demand and Charlotte AI Adoption- Charlotte AI posted 85% sequential growth last quarter and is now deeply embedded across Falcon modules. The call detailed dramatic productivity gains, with tasks that once took days now handled in under an hour. CRWD’s positioning as the security layer for agentic AI is becoming a key narrative for investors.

3. Next-Gen SIEM + Onum Integration- Next-Gen SIEM ARR grew 95% YoY to $430M, and CRWD announced its intent to acquire Onum, a real-time data pipeline platform delivering 5x faster throughput and 50% lower storage costs. This is one of the most important strategic expansions in the product portfolio since LogScale, and investors will look for early customer traction and integration roadmap detail.

4. Cloud Security and Runtime Protection Growth- Cloud ending ARR surpassed $700M, growing 35% YoY. CRWD emphasized that runtime protection — not posture tools alone — is increasingly the core of enterprise cloud security. Management cited large competitive wins and consolidation across CNAPP, CSPM, ASPM, CDR, and container security. More Fortune-500 cloud migrations could become a meaningful catalyst.

5. Identity Security and the Expansion into PAM- Identity remains one of the most important vectors for growth. Next-Gen Identity Protection ARR exceeded $435M, and CRWD highlighted rising interest in its new PAM offering, which consolidates password rotation, identity insights, MFA controls, and privilege risk detection into the Falcon platform.

Contact [email protected] for any questions or corrections.

Joel South covers large-cap stocks, dividend investing, and major market trends, with a focus on earnings analysis, valuation, and turning complex data into actionable insights for investors.

He brings more than 15 years of experience as an investor and financial journalist, including 12 years at The Motley Fool, where he served as an investment analyst, Bureau Chief, and later led the Fool.com investing news desk. He has also co-hosted an investing podcast and appeared across TV and radio discussing market trends.

© 247 Wall Street