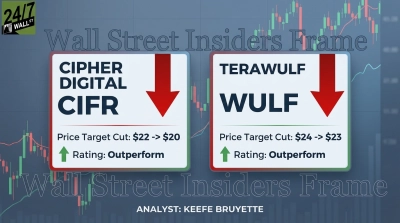

TeraWulf (NASDAQ:WULF) has pulled back sharply from its recent highs, sliding -10% over the past month and currently trading at $14.22. Despite a remarkable 340% one-year run, the stock sits 22% off its 52-week high of $18.51. Most Wall Street analysts carry more measured outlooks, but Keefe Bruyette is holding firm with an Outperform rating and a $23 price target. The broader analyst consensus sits at $25.33, with 13 analysts rated 100% bullish. Keefe Bruyette maintains its Outperform rating with a $23 price target, citing the contracted revenue foundation and HPC build-out schedule as key factors in its outlook.

Keefe Bruyette’s $23 WULF Prediction

Keefe Bruyette trimmed its target modestly from $24 to $23 but maintained its Outperform rating, maintaining its Outperform rating despite the recent pullback. The firm points to TeraWulf’s contracted revenue foundation as the anchor: approximately $12.8 billion in long-term contracted revenue backed by Google credit-enhanced leases provides a level of cash flow visibility rare among bitcoin-adjacent names. With $3.27 billion in cash on the balance sheet following major financing rounds, the company has the capital to execute its build-out through 2026 and beyond.

Key Drivers of WULF Stock Performance

- The pullback itself. A 22% decline from the February 52-week high represents a significant decline from recent highs as contracted HPC capacity comes online through 2026.

- HPC revenue acceleration. HPC lease revenue grew 35% quarter-over-quarter to $9.70 million in Q4 2025, and multiple construction milestones are scheduled for delivery across 2026, including CB-3 in mid-May, CB-4 in Q3, and CB-5 in Q4. Each delivery converts contracted capacity into recurring cash flow.

- Scale of the contracted platform. 522 critical IT MW of contracted HPC capacity and a 2.9 GW gross multi-regional platform underpin an estimated $815 million in average annualized NOI from the contracted platform, reflecting the scale of TeraWulf’s long-term NOI potential.

Keefe Bruyette’s $23 Price Target: Key Factors

Keefe Bruyette’s price target reflects the firm’s Outperform rating, with analysts citing on-time delivery of the 2026 construction milestones, continued growth in HPC lease revenue as a share of total revenue, and stability in bitcoin prices as key factors in its outlook. Bitcoin prices remain a swing factor given BTC’s 20% year-to-date decline to around $70,000.

The primary risk is TeraWulf’s approximately $2.0 billion net debt position, which leaves limited margin for construction delays or tenant setbacks. Even so, with 2026 fixed operating cost guidance of $100 to $125 million and a fully contracted growth pipeline, Keefe Bruyette’s $23 target reflects the firm’s Outperform rating on the stock.