Microsoft (NASDAQ:MSFT | MSFT Price Prediction) is down -20% year-to-date and news today that OpenAI flagged its dependence on Microsoft as a key business risk in a document resembling an IPO prospectus. OpenAI stated that Microsoft provides a substantial portion of its financing and computing resources, and warned that any alteration or termination of the partnership could negatively impact its business.

The Tension That Actually Matters

Companies filing IPO-style documents are required to disclose concentration risks, and OpenAI’s reliance on Microsoft fits that bill. What it does not change is the structural reality, OpenAI is Microsoft’s largest Azure customer, contracted to purchase an incremental $250 billion of Azure services. That commitment is already on Microsoft’s books. Commercial remaining performance obligations surged 110% YoY to $625 billion in Q2 FY2026, a figure reflecting the depth of long-term contracted revenue Microsoft has locked in.

The more substantive risk was disclosed by Microsoft itself, back in Q1 FY2026: OpenAI is no longer exclusively tied to Azure for non-API products. That structural loosening, combined with OpenAI investment losses that ballooned from $523 million to $3.1 billion YoY in Q1, is the real tension investors should track. Q2 swung the other direction, with $7.6 billion in net gains from OpenAI investments boosting GAAP net income to $38.46 billion, up 59.52% YoY. That volatility in a single line item deserves attention.

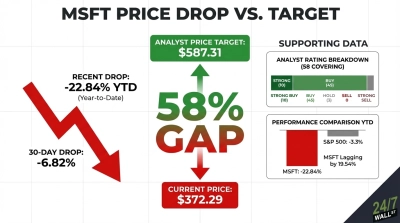

Why BofA’s $500 Target Still Holds Up

Bank of America reinstated Microsoft at Buy this morning with a $500 price target, citing Azure and AI embedding across the enterprise as dual growth engines. The underlying numbers support that framing. Azure grew 39% YoY in Q2 FY2026, with forward guidance of 37%-38% growth next quarter. Intelligent Cloud revenue reached $32.91 billion, up 29% YoY. Capital expenditures nearly doubled to $29.88 billion in Q2, signaling Microsoft is building infrastructure ahead of demand rather than reacting to it.

The broader analyst community remains firmly constructive. 54 of 57 analysts carry Buy or Strong Buy ratings, with a consensus price target of $594.62. The stock’s trailing P/E sits at 24x, with a forward P/E of 20x on forward EPS of $18.52. At current prices, that is a notably compressed multiple for a business generating $51.5 billion in cloud revenue per quarter.

The OpenAI IPO disclosure reflects a legal obligation, not a deteriorating partnership. What investors should actually watch: whether OpenAI’s non-API workloads begin migrating off Azure, whether investment gains or losses dominate Microsoft’s GAAP income in coming quarters, and whether Azure’s guided 37%-38% growth holds as the single most important data point in the next earnings cycle.

Contact [email protected] for any questions or corrections.