NVIDIA (NASDAQ:NVDA | NVDA Price Prediction) just posted the largest quarter in semiconductor history. Q1 FY27 revenue came in at $81.61 billion, up 85.2% YoY, with Data Center alone doing $75.25 billion (+92% YoY). Net income hit $58.32 billion.

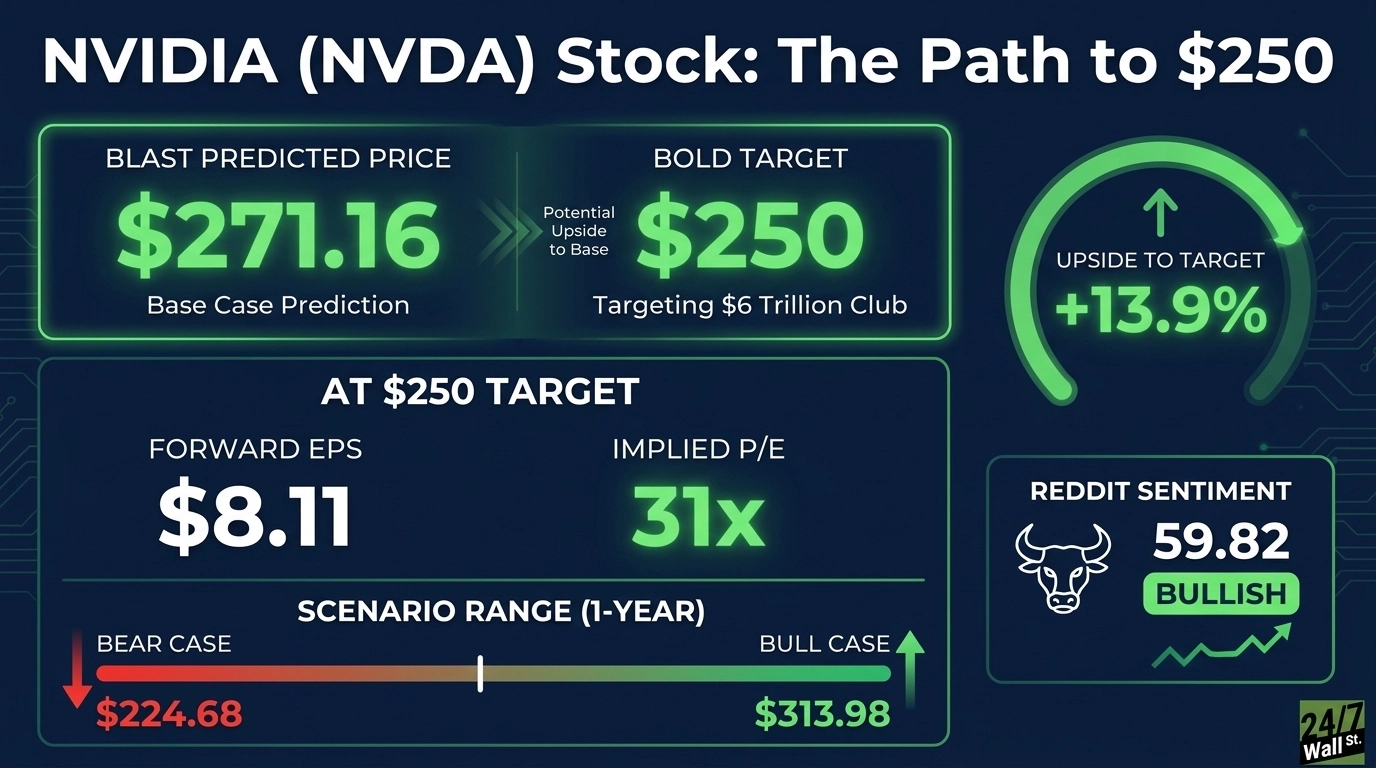

Yet shares sit at $219.51, well below the analyst average. The market cap is roughly $5.41 trillion. To join the $6 trillion club, NVIDIA needs to reach $250 per share. I think that happens by November 18, 2026, the week of the next earnings report.

Why NVIDIA Shares Are Stuck Despite a Monster Quarter

The disconnect is real. NVIDIA is up 17.71% YTD and 66.59% over the past year, but shares are down 6.88% in five sessions this past week, even after a clean beat.

Part of that is positioning. Beta sits at 2.244, so NVIDIA moves twice as hard as the market in both directions. Part is the China overhang. NVIDIA shipped zero H20 units to China this quarter, and the lost TAM there has weighed on the multiple. Prediction markets price caution. Polymarket gives only an 11% probability of $240 in May. Traders want consolidation, not a melt-up.

Wall Street Sees 27% Upside. I Think They’re Underestimating It

The consensus is loud. 10 Strong Buy, 48 Buy, 2 Hold, 1 Sell, with an average target of $278.03. Our internal model lands at $271.16 with 90% confidence, implying 23.53% upside. The scenario range runs from $224.68 bear to $313.98 bull.

Only a handful have moved targets above $300, yet 95% of analysts are bullish. With Q2 FY27 guidance of $91 billion in revenue and supply commitments of $119 billion, the bull case looks underwritten. Analysts are anchored. The forward earnings power is not.

The Path to $250 Per Share

Reaching $250 from today’s price of $219.51 requires a gain of 13.9%. With forward EPS of $8.11, $250 implies a forward P/E of 31x. The base case of $271.16 already prices in 38x, so $250 actually demands less multiple expansion than consensus. That makes this a credible 2026 milestone rather than a stretch.

Catalysts are stacked. CEO Jensen Huang told investors “the buildout of AI factories, the largest infrastructure expansion in human history, is accelerating at extraordinary speed.”

Partnerships now include OpenAI at 10 GW, Anthropic at 1 GW, and CoreWeave at 5+ GW by 2030. Data Center Networking alone grew 199% YoY to $14.8 billion. The risk is a regulatory shock on China, which has already cost NVIDIA a quarter and could compress sentiment further.

Where NVIDIA Trades Today vs Its Earnings Power

The current forward P/E is 27x. For a company growing revenue 85% YoY with 75% non-GAAP gross margins and $48.55 billion in quarterly free cash flow, that multiple is not demanding. Shares sit between a 52-week low of $129.13 and a high of $236.54. The 10-year return is 20,092.97%. The problem is sentiment positioning, not valuation.

Can NVIDIA Really Join the $6 Trillion Club? My Verdict

Reaching $250 per share, a 13.9% gain, would put market cap at roughly $6.05 trillion. I think it is realistic.

Three things need to break right. Q2 FY27 has to land at or above the $91 billion guide, Blackwell 300 has to ramp without yield issues, and the China narrative cannot worsen. A fresh export-control escalation derails it. We’ve outlined the blueprint for how NVIDIA could reach $250 in 2026.

Contact [email protected] for any questions or corrections.