AI hyperscaler CapEx spending is now the single biggest variable in the U.S. power equation. Microsoft (NASDAQ:MSFT | MSFT Price Prediction), Meta (NASDAQ:META), Amazon (NASDAQ:AMZN) and Alphabet (NASDAQ:GOOGL) are collectively guiding to $710B+ in combined 2026 CapEx, and the EIA’s Annual Energy Outlook 2026 now models data center server electricity use growing to 818 billion kilowatthours in 2050, more than 16 times the 2020 level. Nuclear is the only carbon-free, 24/7 baseload generation source that can scale into that demand curve.

The recent selloff in nuclear names has reset entry points across the trade. The three picks below are down sharply from their May highs, even as the long-term thesis (locked-in hyperscaler contracts and government-backed growth) has gotten stronger. Here are three nuclear-linked names worth researching this month.

Constellation Energy (CEG)

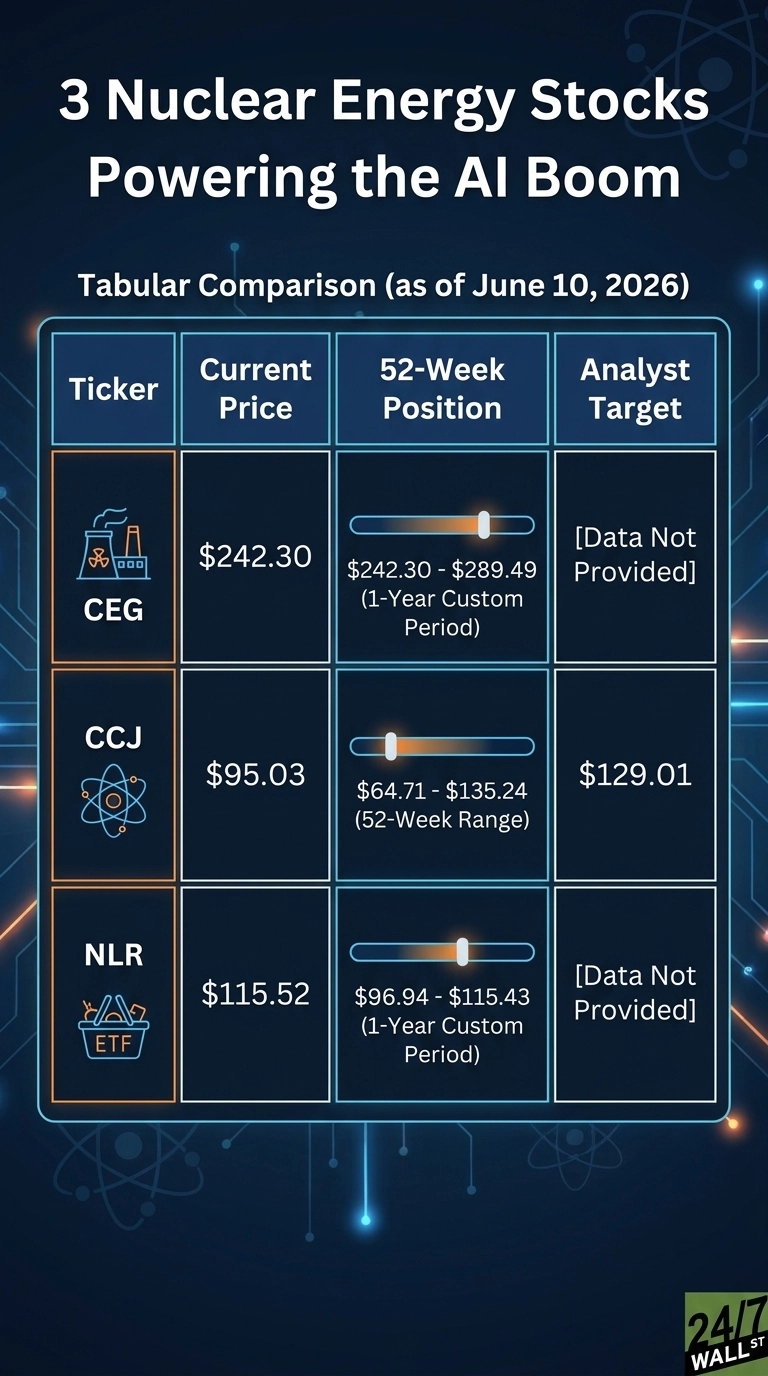

Constellation Energy (NASDAQ:CEG) is the largest nuclear operator in the US and, following its January 2026 Calpine acquisition, the largest private power producer in the world with approximately 55 gigawatts of generating capacity. Q1 FY2026 results delivered adjusted EPS of $2.74 against a $2.60 estimate, with revenue of $11.122 billion, beating consensus by 28% and growing 64% year over year.

The bull case sits on contracted demand. Constellation already has long-term PPAs with Microsoft, Meta, and CyrusOne, including a 380 MW signed at Freestone in February with exclusivity for an additional 380 MW. Management reaffirmed FY2026 adjusted operating EPS of $11.00 to $12.00 and is guiding base EPS growth of 20%+ through 2029, with the PJM Reliability Backstop Procurement framework set to enable bilateral data center contracting starting March 2027. CEO Joe Dominguez framed it directly: “America needs reliable, clean power and Constellation is built to meet this demand.”

Shares now trade at $242.30, down 19% over the past month and 31% year to date. Reddit sentiment in r/stocks has flipped from neutral post-earnings to bullish (sentiment score 66-68) as the valuation debate intensifies.

Risk: The nuclear fleet capacity factor slipped to 92% from 94% year over year, long-term debt jumped to $17.5 billion after Calpine, and integration execution is a real overhang.

Cameco (CCJ)

Cameco (NYSE:CCJ) is the world’s largest publicly traded uranium miner and owns 49% of Westinghouse, the AP1000 reactor OEM. Q1 2026 EPS came in at $0.33 versus the $0.34 estimate, missing expectations by a hair, while revenue of $606.30 million missed consensus by 26%. Below the headline, adjusted net earnings nearly tripled to $145.59 million and Westinghouse adjusted EBITDA jumped 33% to $122 million.

The demand backdrop is unusually clean. 38 countries have pledged to triple nuclear capacity by 2050, the long-term uranium price has climbed to US$91.50/lb, and Meta has announced agreements for up to 6.6 GWe of nuclear capacity. The US DOE has flagged up to US$26.5B in loan guarantees for nuclear infrastructure, and the Brookfield-Westinghouse strategic partnership is targeting global AP1000 deployment. CEO Tim Gitzel called nuclear “uniquely positioned to meet these needs, providing long-term energy security.”

The stock trades at $95.03, off 21% over the past month but still up 49% over the trailing year. The Alpha Vantage analyst target sits at $129.01, with 9 Strong Buy and 10 Buy ratings.

Risk: The valuation is rich at a forward P/E near 91, the Key Lake mill has an extended Q3 2026 maintenance shutdown, and there is an unresolved $559M CRA transfer pricing dispute plus US tariff uncertainty.

VanEck Uranium and Nuclear ETF (NLR)

For investors who want the theme without single-name concentration, the VanEck Uranium and Nuclear ETF (NYSEARCA:NLR) is the diversified vehicle. The fund holds a mix of nuclear utilities, uranium miners, and nuclear services companies, giving it exposure to both the power-generation side (similar to CEG) and the fuel-cycle side (similar to CCJ) in one basket.

NLR trades at $115.52, down 21% over the past month alongside the broader nuclear pullback, but still up 19% year over year and 133% over the trailing five years. The fund’s recent drawdown roughly mirrors the moves in its largest single-name constituents, which is exactly the trade-off baskets create.

Risk: Diversification cuts both ways. The basket structure caps upside relative to a high-conviction single-name pick, top-holding concentration means CEG and CCJ weakness will weigh on the fund, and expense ratio drag erodes long-term returns. Current expense ratio and yield figures were unavailable from the fund snapshot at the time of writing, so investors should consult the VanEck prospectus directly before sizing a position.

What to Watch Next

The next catalysts are policy-driven. Cameco’s Q2 2026 results are scheduled for July 31, the PJM Reliability Backstop Procurement framework activates in March 2027, and the EIA’s High Electricity Demand case projects average annual electricity consumption growth of 2% through 2050. If hyperscaler CapEx holds, the contracted-demand thesis behind each of these names gets stronger, not weaker.

Contact [email protected] for any questions or corrections.