Uber’s (NYSE:UBER | UBER Price Prediction) business is firing on every cylinder: 3.6 billion trips, 199 million monthly active platform consumers, and 50 million Uber One members now driving half of Gross Bookings. Yet the stock is down.

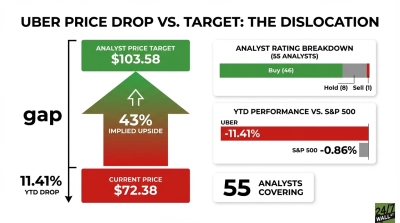

Uber trades at $68.85, off 15.74% year to date, while non-GAAP earnings power compounds. Can shares reclaim $100 before 2027? That is the question I want to answer with real numbers.

The Real Reason Uber Is Down 15.7% This Year

The headline problem is optics. Q1 2026 GAAP net income collapsed to $263 million from $1.78 billion a year earlier, an 85.19% drop driven by a $1.50 billion equity investment revaluation headwind. Revenue also missed by 0.45%, and business model changes shaved roughly nine percentage points off reported revenue growth.

Autonomous vehicle competition fears (Waymo, Tesla robotaxi chatter) add to the pressure, with the stock down 7.83% in the past month and 19.59% over the past year. With a beta of 1.12, Uber moves with the broader market, and sentiment has not been kind. This is sentiment-driven, and sentiment can flip fast.

Wall Street Sees 51.7% Upside. Our Model Says Even More

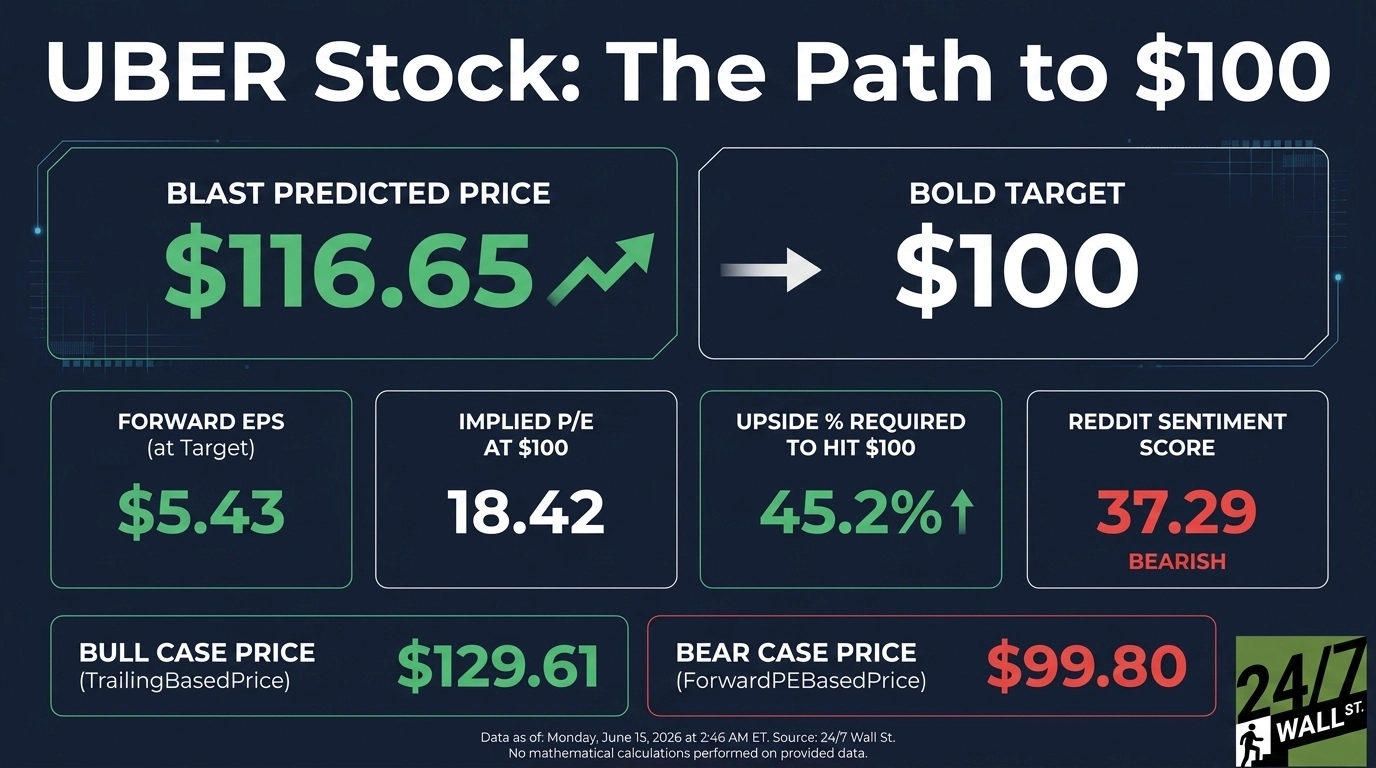

Sell-side consensus targets $104.43, with 9 Strong Buys, 36 Buys, 5 Holds, and just 1 Sell. That is 88% bullish. Our internal model pegs a 12-month base case at $116.65, implying 69.43% upside, with a bull case of $129.61 and a bear case of $99.80.

Confidence is 90%, the highest this framework gets. Analysts are anchored to recent multiple compression and underweighting the platform flywheel. The base case at $88.47 by year-end 2026 already concedes that $100 is the stretch.

The Path to $100 Per Share

Reaching $100 from today’s price of $68.85 requires a gain of 45.2%. With forward EPS of $5.43, a price of $100 implies a forward P/E of 18x. Our base case of $116.65 already implies 13x, meaning the $100 target requires roughly 5.1x additional multiple expansion versus base-case math.

Why is that re-rating reachable? The 247Factor adjustment of 1.157 is powered by an 88% bullish analyst consensus and a 15% sector momentum multiplier from technology innovation tailwinds.

Q2 2026 guidance calls for non-GAAP EPS of $0.78 to $0.82, growth of 31% to 38% YoY, with Gross Bookings of $56.25B to $57.75B. CEO Dara Khosrowshahi said the company enters “2026 with a rapidly growing topline, significant cash flow, and a clear path to becoming the largest facilitator of AV trips in the world.”

Delivery revenue jumped 34% YoY, and Uber repurchased $3.011 billion of stock in Q1 alone. The primary risk is that AV partners turn into AV competitors faster than the platform can monetize them.

Where Uber Trades Today vs Its Earnings Power

At $68.85 against $5.43 forward EPS, Uber trades at roughly 13x forward earnings. That is cheap for a business growing non-GAAP EPS 44% YoY with free cash flow of $2.29 billion in a single quarter.

Shares sit near the 52-week low of $67.19, well below the $101.99 high. The 10-year return of just 65.62% shows how patient long-term holders have had to be. Today’s setup looks like a coiled spring rather than a broken story.

Is $100 Realistic?

Reclaiming $100 by year-end requires a 45.2% gain, putting forward P/E at 18x. It is a stretch, but not a long shot.

Three things need to go right: Q2 results land at the high end of guidance, the AV narrative flips from threat to platform optionality, and buybacks keep shrinking the share count at the current pace. A recession that crimps Mobility growth back into single digits derails it. We’ve outlined the blueprint for how Uber could reach $100 in 2026.