Arm Holdings (NASDAQ:ARM | ARM Price Prediction) and Advanced Micro Devices (NASDAQ:AMD) both reported earnings within 24 hours of each other in early May. Arm sells the blueprints. AMD ships the silicon.

With agentic AI workloads pulling every hyperscaler toward custom CPUs and GPU racks, the two are quietly fighting over the same data center socket, just from opposite ends of the supply chain.

Licensing Royalties Lift Arm. Instinct GPUs Carry AMD.

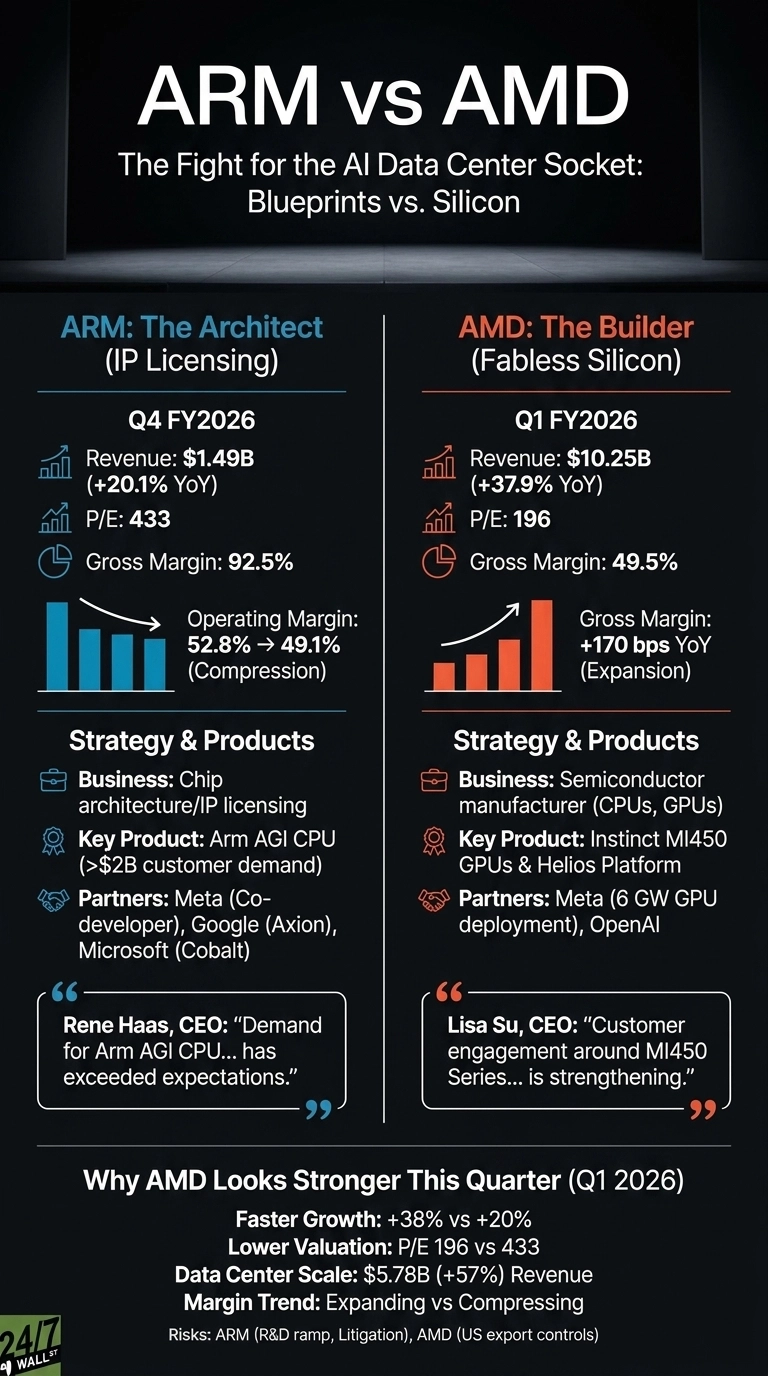

Arm’s Q4 FY2026 brought in $1.49B in revenue, up 20.1% year over year, with non-GAAP EPS of $0.60. The mix mattered more than the headline: license revenue jumped 29% to $819M while data center royalty revenue more than doubled.

CEO Rene Haas framed it bluntly, saying “demand for Arm AGI CPU, Arm’s first data center chip, has exceeded expectations.” That AGI CPU already has over $2B in customer demand pipelined through FY28, with Meta co-developing the roadmap.

AMD’s Q1 2026 was a different scale of result. Revenue hit $10.25B, up 37.9%, with non-GAAP EPS of $1.37. The Data Center segment alone produced $5.78B, up 57%. Lisa Su said “Customer engagement around MI450 Series and Helios is strengthening, with leading customer forecasts exceeding our initial expectations.”

Free cash flow more than tripled to $2.57B. That reflects Meta and OpenAI signing for gigawatts of Instinct silicon, a step beyond a normal chip cycle.

Asset-Light IP Versus Fabless Heavyweight

| Lens | Arm | AMD |

| Business model | IP licensing | Fabless silicon |

| Gross margin | 92.5% | 49.5% |

| Revenue growth (latest Q) | +20.1% | +37.9% |

| P/E | 433 | 196 |

| Lead AI customer | Meta (AGI CPU) | Meta, OpenAI (Instinct) |

Arm collects a royalty whenever a chip ships with its architecture, which is why Google’s Axion, NVIDIA’s Vera, and Microsoft’s Cobalt all feed the same income statement. The risk shows up in the cost line: full-year R&D climbed 43% to $1.91B, and non-GAAP operating margin compressed from 52.8% to 49.1%. Building actual silicon, even at the design level, is expensive.

AMD is taking the opposite bet. Rather than license cores, it is selling complete rack-scale systems through Helios and bundling EPYC plus Instinct. Q2 guidance calls for revenue near $11.2B, up 46% YoY, with gross margin expanding to roughly 56%. The vulnerability sits in geopolitics: US export controls on the MI308 cost roughly $440M across FY25.

The Next Test Is Data Center Execution

I will watch whether Arm’s AGI CPU ships on time and whether royalty rates on data center sockets actually scale faster than R&D. Reddit sentiment around Arm flipped from bullish scores near 76 on June 18 to bearish 32 by June 20, and shares fell 10.14% on June 23 alone. For AMD, the MI450 ramp and Samsung HBM4 timing are the swing factors.

Why AMD Looks Stronger This Quarter

On cleaner AI exposure today, AMD screens better. Revenue is growing nearly twice as fast at a P/E roughly half of Arm’s, and the data center segment is producing real cash.

Arm’s story is more elegant, and the 235% year-to-date run shows the market already loves it. At a 433 multiple, though, execution on the AGI CPU matters before that valuation is justified.

AMD’s 301% one-year return is no bargain either, but the margin trajectory is moving the right way. For investors researching durable royalty compounders, Arm screens as a candidate. For me, this quarter favored the company shipping chips over the one licensing the designs.

Contact [email protected] for any questions or corrections.